ECORA RESOURCES Energy, renewables and resources

and, as such, are written by the companies in question and reproduced in good faith.

and, as such, are written by the companies in question and reproduced in good faith.

Welcome to Spotlight, a bonus report which is distributed eight times a year alongside your digital copy of Shares.

It provides small caps with a platform to tell their stories in their own words.

This edition is dedicated to businesses powering the global economy, whether that be in mining, oil and gas, the renewables space, infrastructure or energy provision.

The company profiles are written by the businesses themselves rather than by Shares journalists.

They pay a fee to get their message across to both

existing shareholders and prospective investors.

These profiles are paidfor promotions and are not independent comment. As such, they cannot be considered unbiased. Equally, you are getting the inside track from the people who should best know the company and its strategy.

Some of the firms profiled in Spotlight will appear at our webinars and in-person events where you get to hear from management first hand.

Click here for details of upcoming events and how to register for free tickets.

Previous issues of Spotlight are available on our website.

Members of staff may hold shares in some of the securities written about in this publication. This could create a conflict of interest. Where such a conflict exists, it will be disclosed. This publication contains information and ideas which are of interest to investors. It does not provide advice in relation to investments or any other financial matters. Comments in this publication must not be relied upon by readers when they make their investment decisions. Investors who require advice should consult a properly qualified independent adviser. This publication, its staff and AJ Bell Media do not, under any circumstances, accept liability for losses suffered by readers as a result of their investment decisions.

In this article we discuss the best performing AIM-listed mining stocks so far this year. The data shows that small cap miners producing tin, tungsten, helium, and gold exploration companies have offered impressive returns to investors.

UK-based helium exploration and production company

Helium One Global (HE1:AIM) has seen shares gain an impressive 274%. These gains, albeit from a low base, are primarily due to the progress the company has made with its flagship project in Tanzania.

The company holds exploration licenses covering 4,512 square kilometres in the Rukwa Rift basin in Tanzania which may in the

future become a new helium province.

As an early-stage explorer in this field it is well-positioned to benefit from rising longterm helium demand and pricing.

Although Plymouth-based tungsten and tin miner Tungsten West (TUN) has seen share price gains of 120%, there have been a few wobbles this year including the abrupt departure of CEO Neil Gawthorpe in June.

In mid-August, the company appointed a new CEO Jeffery Court who has 30 years’ experience of the mineral resource sector.

Shares in lithium miner

Savanna Resources (SAV:AIM) jumped 15% on 20 June after it received a £16 million investment from AMG Critical Materials group – an Amsterdam-listed specialty metals group.

Over the past year shares have gained 92.9% as the company continues to grow and develop Europe’s first European lithium mine north of Portugal.

Gold, copper, silver, and precious metal company Anglo Asian mining (AAZ:AIM) has seen shares gain 50%.

On the 5 August, the company’s Azerbaijan subsidiary, Azerbaijan International Mining Company Limited (AIMC) was given the green light from the Azerbaijan government for the final phase of its tailings dam.

‘Confirmation was also received that the construction work will comply with all health and safety requirements,’ said the company.

Anglo Asian mining continues to prioritise the progression of its development portfolio, with the new Gilar mine expected to enter production in the fourth quarter of 2024.

Other gainers this year are specialist metal supplier Uru Metals (URU) and an early-stage gold exploration company Oriole Resources (ORR:AIM). Uru Metals shares have gained 107% and Oriole Resources shares have gained 100%.

In January this year, Oriole Resources signed two agreements with BCM International in respect of the group’s Bibemi and Mbe projects.

On the 5 September, the company reported a pretax profit for the six months to 30 June of £1.15 million compared to a loss of £860,000 last year. Oriole has also been a beneficiary of a rising gold price.

Company Year-to-date performance

With a portfolio focused on future facing commodities and the business model of providing funding to the mining sector, Ecora Resources (ECOR:LSE/TSX.

ECRAF:OTCQX) is truly a company at the heart of the energy transition.

With many of the world‘s royalty companies focused on the precious metals space, Ecora has long been concentrating on the mining sector‘s primary thematic, positioning itself as the world’s leading royalty company focused on the critical minerals essential to renewable and low carbon electricity generation, as well as electricity’s subsequent transmission, storage, and consumption.

By focusing on building a diversified portfolio of royalties over low-cost projects backed by strong operators such as Vale (VALE:NSE), Capstone Copper (CS:TSE), BHP (BHP) amongst others, Ecora has built a strong platform for further growth and diversification.

Looking ahead, volume growth in 2024 and 2025 is expected from the operations

underpinning Ecora’s royalty portfolio, and its portfolio of royalties over a pipeline of high-quality development projects provides strong revenue growth potential thereafter.

However, this outlook was not always so clear-cut. Back in 2014, the business was entirely dependent on a single royalty over a steel making coal mine, Kestrel, and mining activities were not expected within the royalty area after 2030.

Cognizant of that overdependence, as well as the

energy transition’s potential to drive critical mineral demand growth over multiple decades, the company embarked on a journey to rebuild its portfolio and provide investors with a royalty company fully aligned with this trend.

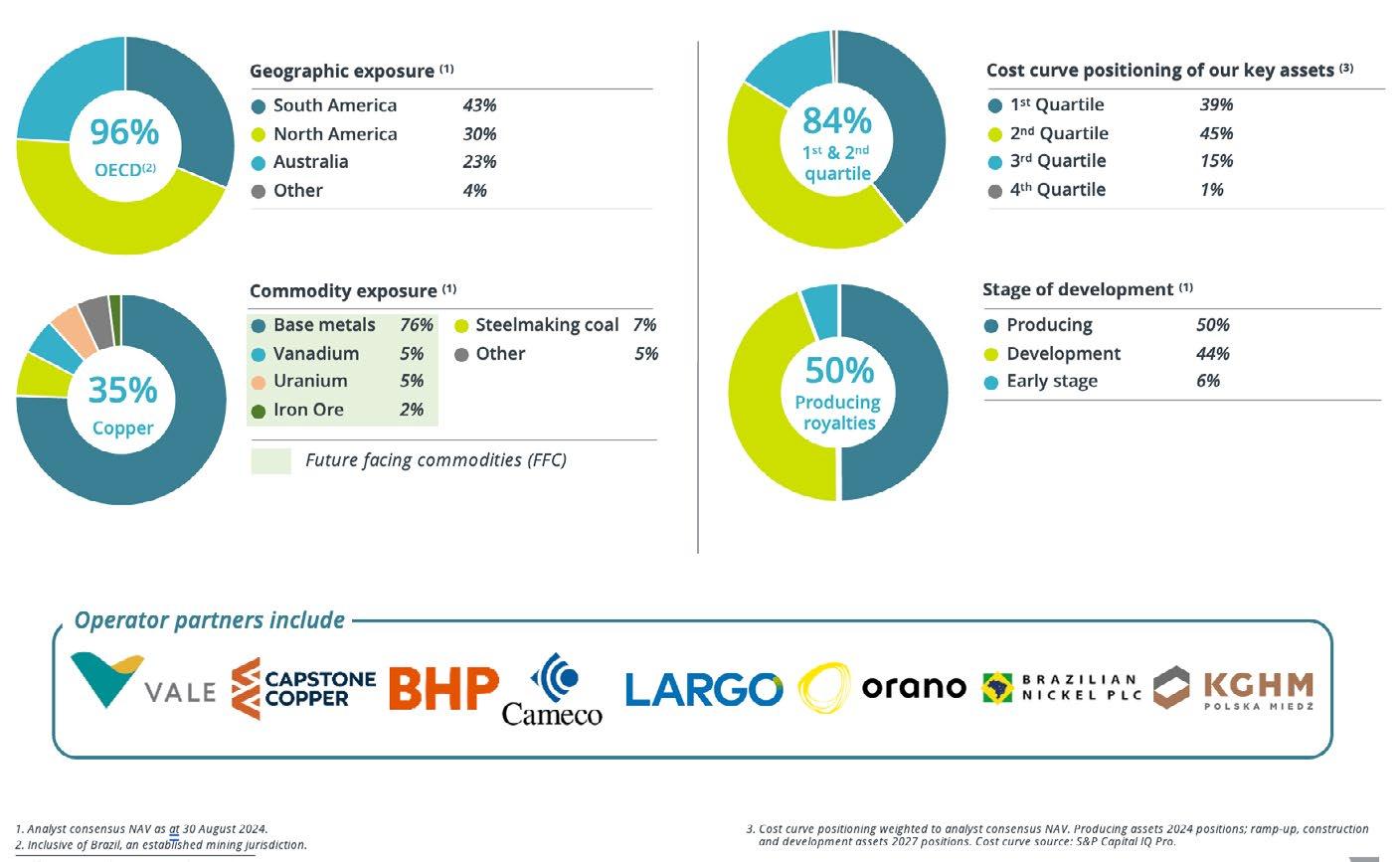

In the brief time since, Ecora’s portfolio has evolved such that 85% of its NAV (net asset value) now comes from future-facing commodities including copper, nickel, cobalt, uranium, and rare earths, amongst others. Most of these assets are in OECD (organisation for economic co-operation and development) jurisdictions, over operations that can, or are expected to, generate strong cash flows throughout the highs and lows of commodity price cycles and operated by recognized, high quality partners.

For investors, Ecora’s royalty portfolio provides a relatively de-risked way to invest in the metals and mining space given royalties are a function of the revenue generated by a mine operation, and not impacted directly by operating costs, with few royalty companies purely focused on investing in commodities driving the energy transition.

In the medium term, the portfolio has the potential to generate more than $100 million annually, primarily underpinned by a sector leading portfolio of royalties

over copper operations and high-quality development projects.

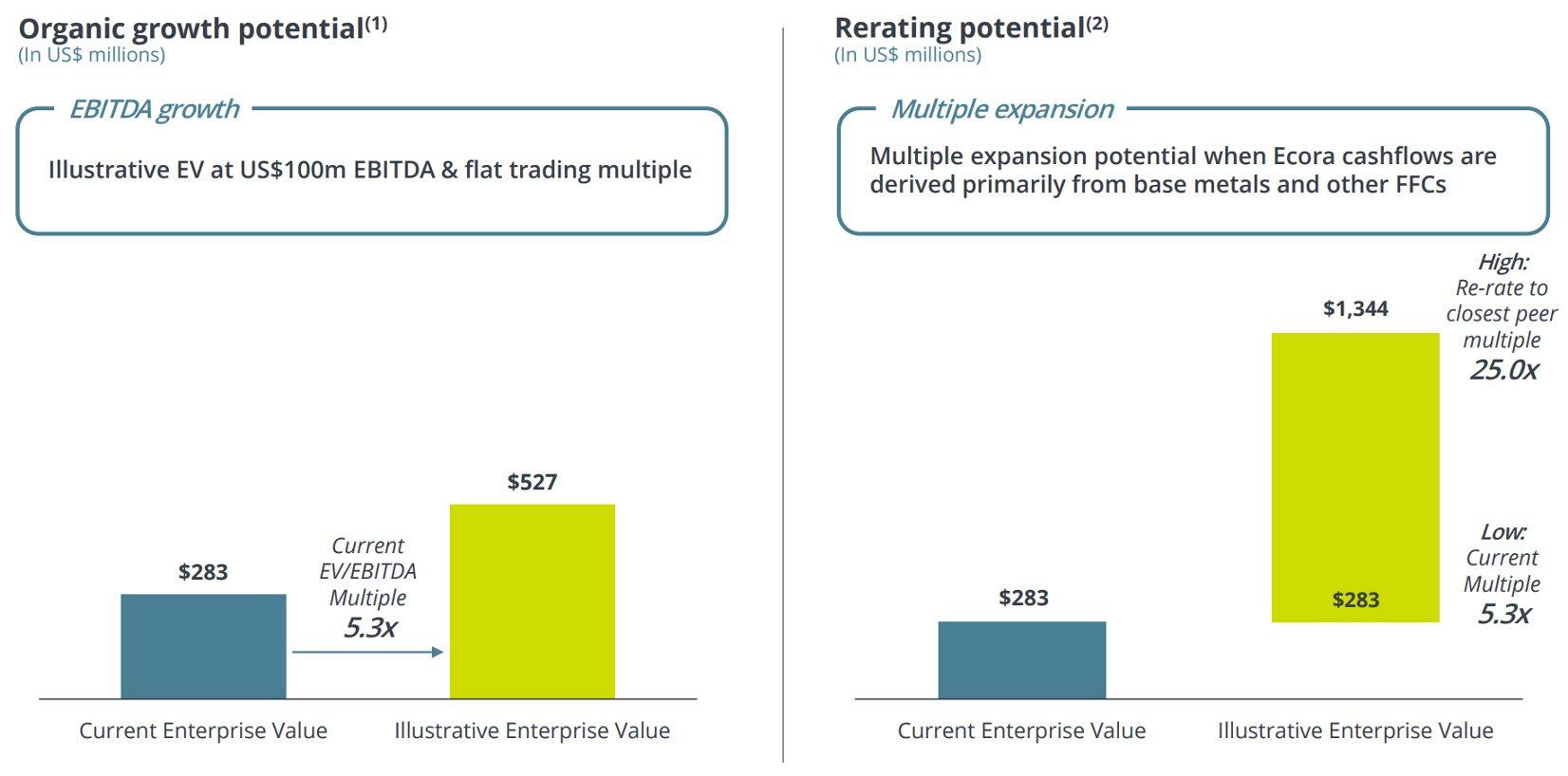

In addition to its current dividend yield of approximately 5%, Ecora shares offer substantial value, with the share price today less than the value of the producing portfolio, meaning that its portfolio of royalties over high quality development projects are not currently priced in, and provide pure upside for investors.

The capital that Ecora’s management has deployed

DID YOU KNOW?

• Ecora has the leading copper growth pipeline in the royalty sector.

• One tonne of copper brings functionality to 40 cars, powers 100,000 mobile phones, enables operations in 400 computers and provides electricity to 30 homes.

• Demand could nearly double by 2035 and there will be a 20% shortfall from the supply level required for the netzero emissions by 2050 target.

has yielded a portfolio of royalties generating cashflow, as well as high quality projects that once in production, will become the cornerstones of the business for many decades to come. It is a strong platform to continue to grow Ecora’s royalty portfolio, which would benefit further from continued diversification.

Capital market conditions for the mining sector have been challenging of late, highlighting the merits of the royalty partnership as a source of capital, with royalty financing now a mainstream source of funding. Coupling the mining sector’s need for capital, and expectations of strong critical mineral demand growth trends, Ecora’s near and midterm growth prospects appear attractive.

Marc Bishop Lafleche, CEO

Ecora’s strategy is to acquire royalties and streams over low-cost operations and projects with strong management teams, in well-established mining jurisdictions. Our portfolio has been reweighted to provide material exposure to this commodity basket and we have successfully transitioned from a coal orientated royalty business in 2014 to one that by 2026 will be materially coal free and comprised of over 90% exposure to commodities that support a sustainable future.

Shaun Bunn, Managing Director

Empire Metals (LON:EEE) is an exploration and resource development company focused on the Pitfield Project in Western Australia, a globally significant titanium project contained within a giant, sediment-hosted, hydrothermal mineral system.

Paul Barrett, CEO

Pathfinder Minerals Plc (PFP) is a natural resources company is being admitted to AIM following the acquisition of Rome Resources Limited in a reverse takeover. Rome Resources holds tin assets in the DRCongo with encouraging initial drilling results, situated only 8km from the highest grade tin mine in the world.

Source: Refinitiv. *Data to 23 September.