UK investment opportunities in the Floating Wind sector

May 2023 (webinar)

3rd

Agenda

• Julien Danne – Head of DBT France’s Clean Growth cluster, British Embassy Paris Welcome

Policy update

• Aidan Campbell – DESNZ’s Head of Floating Wind, London

Wales

• Helen Donovan – Welsh government’s Industrial Transformation & Foundational Economy Division

Scotland

• Ian MacDonald, Scottish Enterprise Offshore Wind Specialist

• Julien Rapenne – Scottish Development International Trade Adviser

Q&A

Offshore Wind in the UK: Policy update

3 May 2023

The status of Offshore Wind in the UK

The UK has the highest offshore wind deployment (13.9 GW) in Europe, the world’s largest wind farm (Hornsea Two), and both the world’s first (Hywind Scotland) and largest (Kincardine) floating offshore wind farms.

We have a world-leading ambition to deploy up to 50 GW by 2030, including up to 5 GW of floating offshore wind.

Hornsea Two. Source: Ørsted

The pipeline of offshore wind farm projects

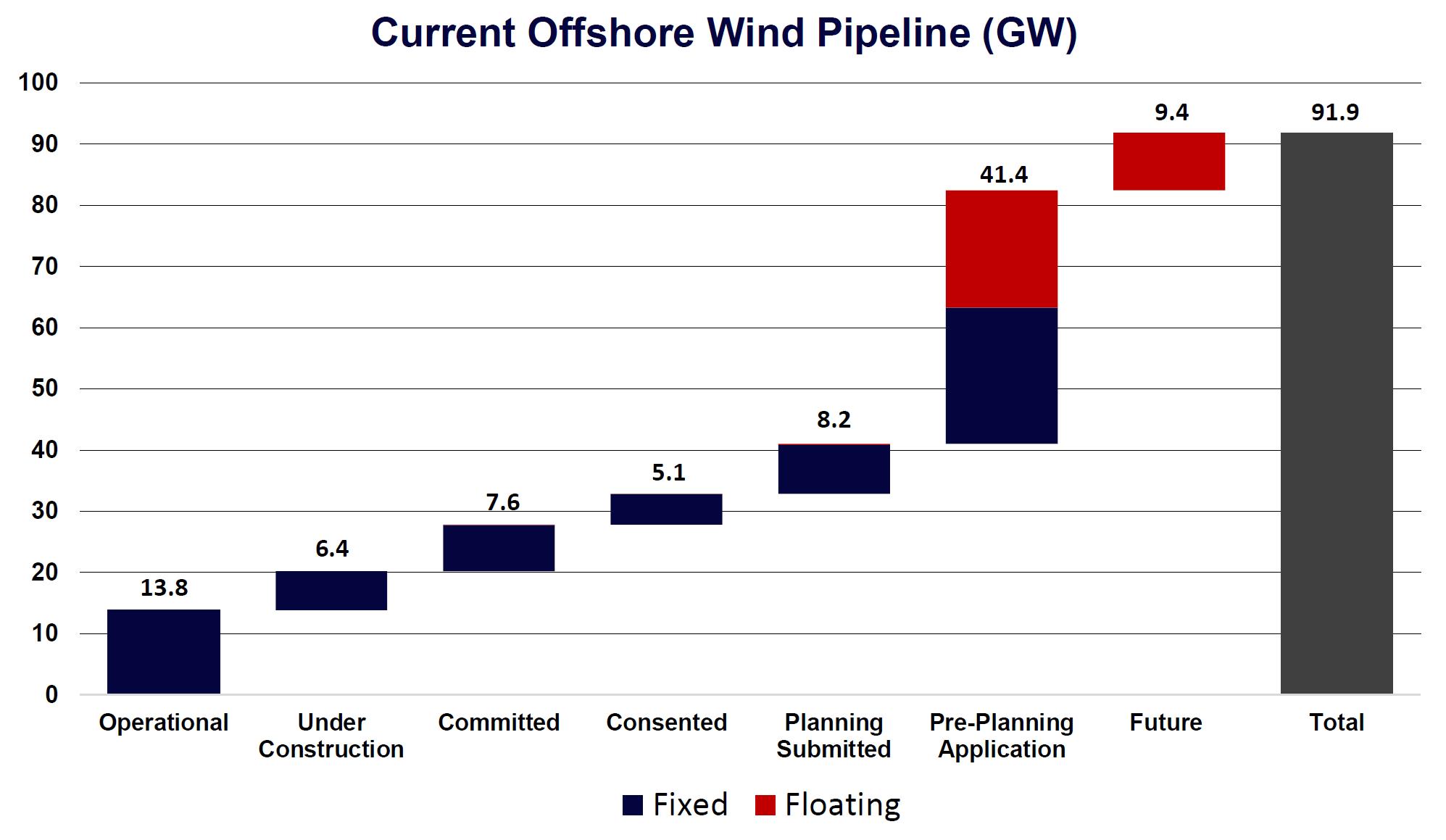

• There is around 78 GW of offshore wind capacity in the UK pipeline.

• Around 60% is fixed-bottom, and 40% is floating.

• Crown Estate Scotland awarded rights for 27.6 GW of new capacity through the Scot Wind leasing round.

• A further 5 GW of seabed exclusivity agreements were announced through the Innovation and Targeted Oil and Gas process.

• A further 4 GW is expected through the Celtic Sea floating wind leasing round.

British Energy Security Strategy

• The BESS created the Offshore Wind Acceleration Taskforce, a group of industry experts brought together to work with Government, Ofgem and National Grid on further cutting the timeline.

• When it ended in April 2023, Offshore Wind Champion, Tim Pick, who co-chaired the Taskforce, published a report, outlining seven areas of opportunity for industry, government, and the Crown Estates to accelerate the deployment of UK offshore wind farms.

• The BESS also set out that we will reduce the time it takes to get planning consent by:

• strengthening the Energy National Policy Statements, which Government are consulting on;

• reviewing the way in which the Habitats Regulations Assessments are carried out;

• implementing a new Offshore Wind Environmental Improvement Package;

• establishing a fast-track consenting route for priority cases where quality standards are met.

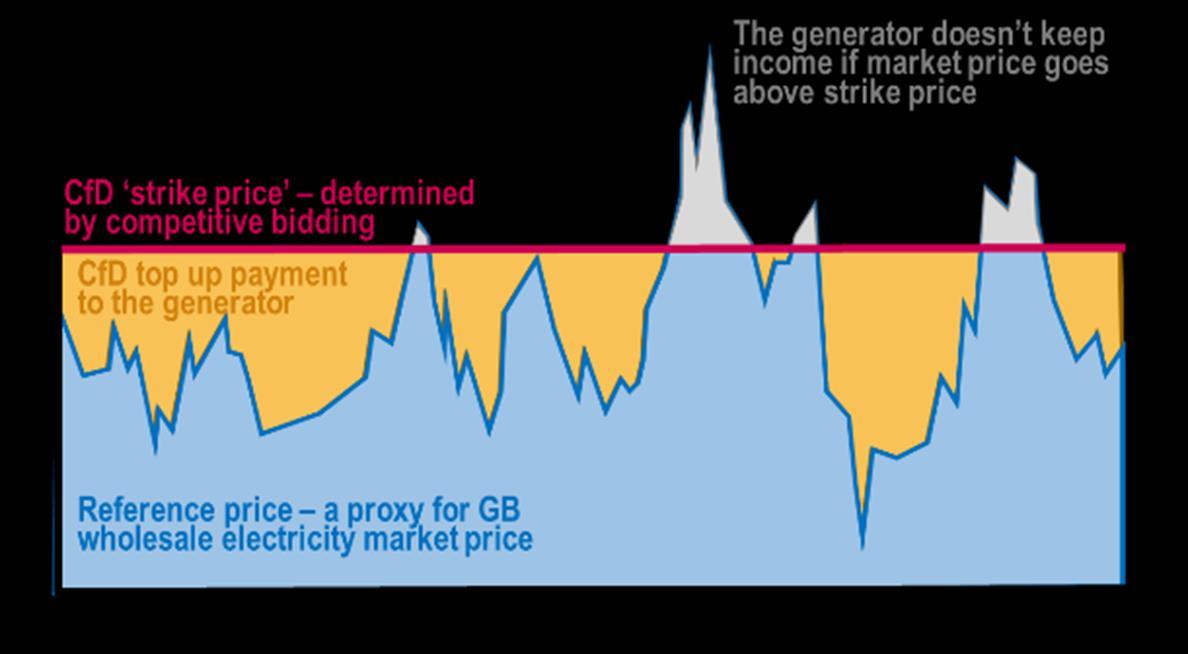

Contracts for Difference scheme

• The Contracts for Difference (CfD) scheme is the government’s main mechanism for supporting new lowcarbon electricity generation projects in Great Britain. It guarantees a set price per MWh of electricity for 15 years, indexed to inflation.

Contracts for Difference scheme

• Approximately 7 GW of offshore wind projects won a CfD in 2022’s Allocation Round 4, which was the largest CfD round ever, including the first ever floating wind project (TwinHub).

• Allocation Round 5 (AR5) opened in March 2023 and is the first CfD round to run on an annual basis in line with the government’s commitment to increase the frequency of auctions to further support the of the rollout of new renewable energy projects in Great Britain.

• AR5 closed to applicants on 24 April. Results will be announced in the summer.

• On 17 April, we published a Call for Evidence on the potential introduction of non-price factors into the CfD auction in future allocation rounds.

Offshore Transmission Network Review

• The Offshore Transmission Network Review (OTNR) was set up in 2020 to improve the delivery of transmission connections for offshore wind. It seeks to coordinate this transformation, ensuring impacts on communities, the environment and network efficiency are considered as well as minimised whilst building a cheaper, greener, and more secure energy system for Britain.

• The Holistic Network Design (HND) provides an upfront plan for both wider network reinforcements and the connections for offshore wind. It recommends how to connect 23 GW of energy to where it is needed, enabling the delivery of 50 GW by 2030.

• The HND Follow Up Exercise will provide recommended connections for an additional 24 GW of offshore wind from ScotWind and Celtic Sea wind. We expect this to be published in summer 2023.

• The forthcoming publication of the OTNR’s Future Framework outlines recommendations and actions for a more strategic approach for the deployment of offshore wind, interconnectors and multi-purpose interconnectors. This covers new offshore wind from conception to project delivery, shaping the future of offshore wind delivery.

Floating Offshore Wind Manufacturing Investment Scheme

• We have now launched the Floating Offshore Wind Manufacturing Investment Scheme (FLOWMIS), which will provide up to £160 million to kick start investment in port infrastructure projects needed to deliver our floating offshore wind ambitions.

• We are committed to placing the UK at the forefront of the development of the sector, underlined by the announcement in the British Energy Security Strategy of our ambition to deploy up to 5 GW of floating offshore wind by 2030 – more than 60 times current installed capacity.

• To achieve this ambition, we are supporting the investment needed in port infrastructure to deploy the large-scale components of floating offshore wind turbines.

Floating Offshore Wind Manufacturing Investment Scheme

• Floating foundations require port facilities that combine a substantial depth of water with heavy-lift capacity and extensive quayside space, meaning ports are likely to require upgrades to their existing facilities.

• The scheme is open to ports across the UK and we welcome applications from any port that believes it can meet the strategic objectives of the scheme and offer value for money.

Thank you

Floating Offshore Wind in Wales

3 rd May 2023

CONTENTS

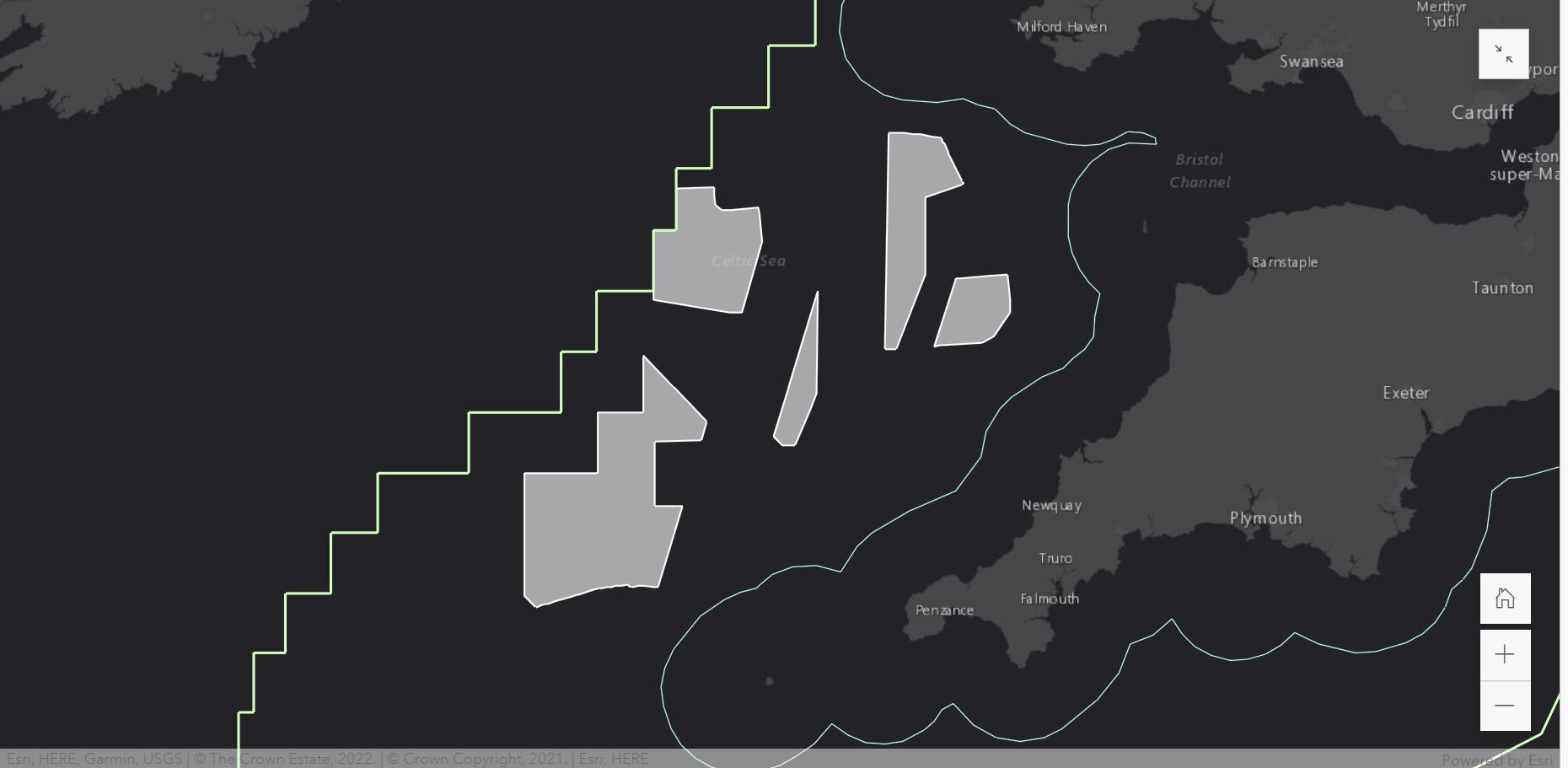

Celtic Sea - What’s there now & Scale of Opportunity

Celtic Sea - Crown Estate seabed leasing

Investment Opportunities

CELTIC SEA – WHAT’S THERE NOW

CELTIC SEA - PROJECT DEVELOPERS

Test and demo, up to 100MW

Early stage commercial, up to 300MW:

Blue Gem Wind 96MW Erebus project – has seabed licence and marine licence

ERM 300MW – hydrogen production

Hexicon 40MW – has seabed licence & CfD

Awaiting outcome of TCE HRA

process:

Whitecross 100MW

Blue Gem Wind 300MW Valorus project

Floventis – 2 x 100MW

CELTIC SEA CLUSTER

Founding members include:

Welsh Government

Offshore Renewable Energy

Catapult

Marine Energy Wales

Cornwall & Isle of Scilly LEP

Celtic Sea Power

CSC – Celtic Sea Supply Chain Cluster (celticseacluster.com)

CELTIC SEA – FLOATING OFFSHORE WIND

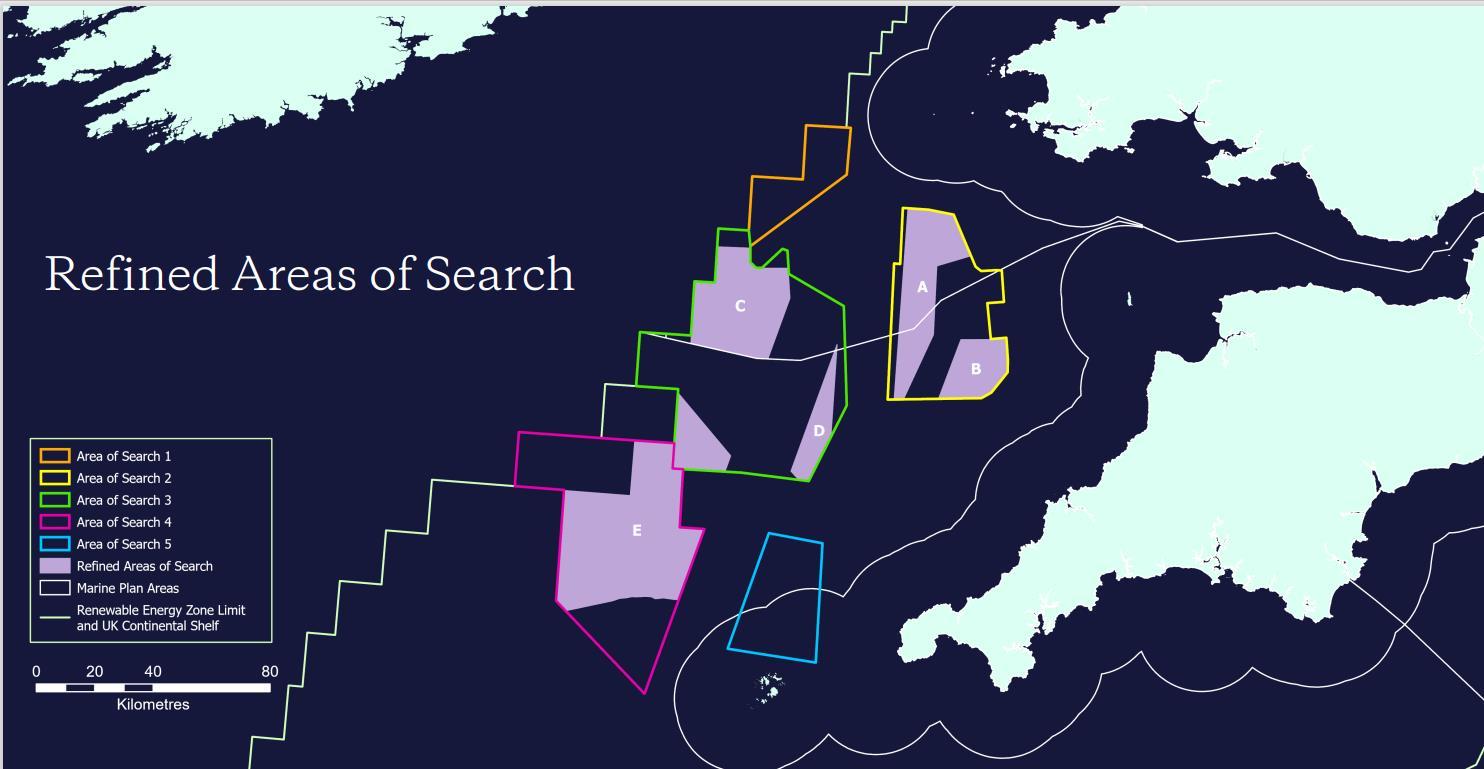

CELTIC SEA - REFINED AREAS OF SEARCH

INVESTMENT OPPORTUNITIES

Investment

Supply Chain Opportunities Port

Opportunities

INVESTMENT OPPORTUNITIES

Turbine Components

FLOW sub-structures (steel or concrete)

Substation manufacture

Turbine and Foundation

Foundations

Mooring systems

Installation

Installation – Other

Anchors

Decommissioning

Cables

CELTIC SEA – MAIN WELSH PORTS

Port Talbot

Pembroke Dock

Cardiff

Port Talbot

Pembroke Dock

Cardiff

ABP – PORT TALBOT

Image courtesy of Associated British Ports

Image courtesy of Associated British Ports

MILFORD HAVEN PORT AUTHORITY – PEMBROKE DOCK

Image courtesy of Milford Haven Port Authority

Image courtesy of Milford Haven Port Authority

PORT – SUPPLY CHAIN OPPORTUNITIES

Port Talbot

Pembroke Dock

High value manufacturing

Engineering Services

–

Foundations

Wind Turbine Integration

–

Subsea cables

Engineering Services

Operations & Maintenance

Wind Turbine Integration

Also opportunity for port to service bottom-fixed wind projects between Wales and Ireland

CONTACT DETAILS

Helen Donovan

Department of Economy, Treasury & Constitution

Helen.donovan@gov.wales

Senior Industrial Transformation Manager

OFFSHORE WIND IN THE UK

Opportunities in Scotland

SCOTTISH DEVELOPMENT INTERNATIONAL

Scottish Development International (SDI) is the specialist trade and investment arm of:

• Scottish Government

• Scottish Enterprise

• Highlands & Islands Enterprise

• South of Scotland Enterprise

SDI is Scotland’s single point of contact for all international business development needs. We work in close partnership with:

• Local Authorities and Business Gateway

• Chambers of Commerce

• Business organisations

• UK Department for Business & Trade

SCOTTISH OFFSHORE WIND PIPELINE

• The past 18 months have seen a seismic shift in Scotland’s offshore wind sector, with two new leasing rounds – ScotWind and INTOG – dramatically increasing the Scottish offshore wind project pipeline to 45.5GW (inc 24.9GW floating wind).

• The ScotWind leasing process awarded development rights to 20 projects (17 in January and 3 in August) with proposed capacity of 30 gigawatts (GW).

• The Innovation and Targeted Oil & Gas (INTOG) leasing round offered rights to a further 13 projects with proposed capacity of 5.4GW.

• The construction of these projects could not only transform Scotland’s energy system, but also reshape Scotland’s renewable energy industry.

• Scotland must, however, build capacity and capabilities in several key areas – including our supply chain and port infrastructure – to leverage the full economic value of offshore wind.

SCOTTISH OFFSHORE WIND PIPELINE

Scotland needs to move from industry that has built less than 2GW of offshore wind in the past 15 years, to one that can build 20GW+ over the next 15 years.

35,432MW Lease Offer

NO PROJECT DEVELOPER CAPACITY 1 Robin Rigg RWE Renewables 174MW 2 Beatrice SSE / Red Rock Power 588MW 3 Hywind Scotland (Floating) Equinor 30MW 4 Aberdeen Offshore Wind Farm Vattenfall 96.8MW 5 Kincardine (Floating) Grupo Cobra 50MW 6 Levenmouth Turbine ORE Catapult 7MW 7 Moray East Ocean Winds 950MW 8 Seagreen SSE / TotalEnergies 1,075MW 9 Neart na Gaoithe EDF / ESB 448MW 10 Moray West Ocean Winds 882MW 11 Seagreen 1a SSE / Total 500MW 12 Inch Cape Red Rock Power / ESB 1,080MW 13 Forthwind Cierco 20MW 14 Pentland Floating Wind Farm CIP 100MW 15 Berwick Bank SSE 4,100MW 1635 ScotWind 30,016MW 3648 INTOG 5,416MW 1,896MW Operational 1,523MW Construction

2,482MW Consented 4,200MW In Planning

SCOTWIND PIPELINE

NO PROJECT DEVELOPER TECH CAPACITY 16 MachairWind ScottishPower Renewables Fixed 2,000MW 17 Spiorad na Mara Northland Power Fixed 840MW 18 Talisk Magnora ASA / TechnipFMC Float 495MW 19 Havbredey Northland Power Float 1,500MW 20 West of Orkney Windfarm RIDG / TotalEnergies / GIG Fixed 2,000MW 21 Ayre DEME / Qair / Aspiravi Float 1,008MW 22 Stromar BlueFloat Energy / Renantis / Orsted Float 1,000MW 23 Caledonia Offshore Wind Farm Ocean Winds Fixed 2,000MW 24 Broadshore BlueFloat Energy / Renantis Float 900MW 25 Buchan Offshore Wind BayWa / BW Ideol / Elicio Float 960MW 26 MarramWind ScottishPower Renewables / Shell Float 3,000MW 27 Muir Mhor Fred Olsen / Vattenfall Float 798MW 28 CampionWind ScottishPower Renewables / Shell Float 2,000MW 29 Bowdun DEME / Qair / Aspiravi Fixed 1,008MW 30 Morven BP / EnBW Fixed 2,907MW 31 Ossian SSE / CIP / Marubeni Float 3,600MW 32 Bellrock BlueFloat Energy / Renantis Float 1,200MW 33 Sealtainn ESB Float 500MW 34 Arven Ocean Winds / Mainstream Float 1,800MW 35 Ocean Winds NE1 Ocean Winds Float 500MW Total Fixed Wind 10,755MW Total Floating Wind 19,261MW Total ScotWind 30,016MW

INTOG PIPELINE

The Innovation and Targeted Oil & Gas (INTOG) has made development rights available for projects that will directly reduce emissions from oil & gas production (TOG) and project that will boost offshore wind innovation (IN).

NO PROJECT DEVELOPER TYPE CAPACITY 36 Sinclair BlueFloat Energy / Renantis IN 99.5MW 37 Scaraben BlueFloat Energy / Renantis IN 99.5MW 38 Salamander Simply Blue Energy / Orsted / Subsea 7 IN 100MW 39 BP IN4 BP IN 50MW 40 Malin Sea Wind ESB IN 100MW 41 Green Volt Flotation Energy / Vårgrønn TOG 560MW 42 Cerulean Winds TOG7 Cerulean Winds TOG 1,008MW 43 Harbour Energy TOG8 Harbour Energy TOG 15MW 44 Cerulean Winds TOG9 Cerulean Winds TOG 1,008MW 45 Cerulean Winds TOG10 Cerulean Winds TOG 1,008MW 46 Cenos Flotation Energy / Vårgrønn TOG 1,350MW 47 TotalEnergies TOG12 TotalEnergies TOG 3MW 48 Harbour Energy TOG13 Harbour Energy TOG 15MW Total Innovation 449MW Total Targeted Oil & Gas 4,967MW Total INTOG 5,416MW

LOCAL CONTENT COMMITMENTS AND AMBITIONS

The ScotWind Supply Chain Development Statement (SDCS) documents provide a snapshot of the supply chain Scotland will need to build to realise the value of its offshore wind project pipeline.

Commitment

As part of their bids, developers were asked to outline expenditure commitment over the development, construction, installation and operation phases of the projects. In total, the 17 projects awarded leases in January have committed to £25.5bn of Scottish supply chain expenditure. Latest figures for all 20 projects show Scottish commitments totalling £28.8bn indicating an average investment in Scotland of £1.4bn per project / £1bn per GW.

Ambition

Projects were also asked to estimate expenditure ambition over the relevant phases of the project. The 17 original ScotWind projects have outlined further ambitions of £11.1bn of offshore wind supply chain earmarked for Scotland which amounts to 49% of the total supply chain spend.

Commitment (£bn) Ambition (£bn) Scotland 25.5 36.6 UK 10.9 12.9 EU 25.0 21.4 Other 8.0 3.9 Total 69.4 74.8

KEY CHALLENGES PORT AND SUPPLY CHAIN CAPACITY

Delivering Scotland’s extensive pipeline of offshore wind farm projects will require significant investment in Scotland’s port and manufacturing infrastructure. Without this, port constraints will either delay deployment or limit Scottish content by forcing developers to use port facilities outside of Scotland.

• Timelines produced by the Scottish Offshore Wind Energy Council (SOWEC) show that there is a shared sector risk of slowed deployment due to shortage of port space for assembly and manufacturing

• If the sector waits until projects can unilaterally contract with ports, ports cannot be made ready in time for ScotWind delivery. There is a need to work ahead of time to build business cases.

• Securing Scottish content from offshore wind manufacture and assembly will also require inward investment.

Deployment based on grid and planning timelines

Deployment based on 2x planned assembly capacity

Deployment based on planned assembly capacity

KEY OPPORTUNITY FLOATING FOUNDATIONS

There is a commercial opportunity to establish a manufacturing facility in Scotland for the serial production of floating substructures to serve the growing pipeline of floating wind projects.

With floating offshore wind, the turbine is installed on a steel, concrete, or hybrid floating substructure, which is anchored to the seabed by mooring systems consisting of flexible anchors, chains or steel cables.

Substructures to date have been largely bespoke with a wide range of designs. The four most prominent substructure types are:

Scotland is home to a number of companies capable of fabricating substructure components but, as yet, there is no single company looking at serial substructure fabrication or assembly. There is an opportunity for a company with expertise in the fabrication and assembly of large steel or concrete structures to capitalise on this lucrative gap in the supply chain.

In addition to a clear pipeline of commercial scale projects unlocking economies of scale, cost reduction will be driven by a combination of continued technology optimisation and innovation, increasing standardisation and targeted port investment.

Collaborate with Scotland’s leading innovation ecosystem to realise cost advantages from advances in fabrication and assembly facilities and processes, such as advanced manufacturing and robotic welding.

Project No Required

› › › › 10 28 222 833

credit: Boskalis

Kincardine

Principle Power substructure.

Picture

KEY OPPORTUNITY MOORING ANCHOR SYSTEMS

Mooring is the element that fixes and flexibly connects the floating substructure to the anchoring point on the seabed. The choice of mooring system depends on variables such as the depth, the type of floating platform and the meteorological conditions (waves, currents, winds). In floating wind, catenary mooring has been deployed for semi-submersible, spar and barge-type substructures.

Several components compose a mooring system: mooring lines, connectors, clump weights and anchors.

The table below shows component number projections for Scotland based on

Anchors are the elements that connect the moorings to the seabed. The anchor type used depends on the mooring system configuration, characteristics of the seabed and the environmental loads.

› Drag anchor

› Suction anchor

› Driven piles

› Drilled piles

› Gravity anchor

› Vertically loaded

Bruce Anchor is a British company specialising in drag-embedded anchors and associated equipment design. Originally the company provided anchors for the oil and gas industry, but has since successfully diversified into offshore renewables. Bruce Anchor has been involved in multiple floating offshore wind projects both in the UK and abroad. The company is developing a drag embedded anchor specifically for floating offshore wind. This anchor will be able to provide the same holding capacity as bigger units, but at a significantly reduced weight and, as the consequence of reduced weight, at a fraction of the transportation costs.

Component Per Substructure Total

› Improvements in design standards, standardisation of components,

› Use of novel materials (including synthetic rope)

› Optimisation of array layouts

A more integrated design interface between anchors, mooring system and substructure would enable further benefits and speed up installation and major repair operations.

Drag Embedment Anchor Picture credit: Bruce Anchor

KEY OPPORTUNITY DYNAMIC CABLES

FOW requires dynamic, high-capacity subsea cable systems to collect and export the power they generate. The cable needs to be ‘dynamic’, as it connects the moving substructure to a fixed element (the seabed).

In addition to the cable, a number of supporting components are required to allow limited movement and to protect the cables and the connection with the array cables on the seabed.

Substations have not been needed for demonstration floating wind projects as they generate limited levels of power that can be exported directly to shore. However, commercial scale projects, with significantly higher power outputs, will require OSS to host a step-up transformer and the equipment necessary to export power in high voltage. With commercial scale projects on the horizon, substation solutions are attracting greater attention and investment from leading industry players.

› Optimise cable connection systems to reduce the time taken to connect and disconnect cables.

› Improve cable design to withstand the different loadings dynamic cables are under in site conditions at FOW sites.

› Innovations required in both static and dynamic cable design to provide higher voltage array cables for projects using higher rated turbines.

For early commercial floating windfarms, where water depths allow, fixed-bottom structures may be preferred to limit the risks and costs associated with new technologies. A bottom-fixed OSS could be economically competitive in water depths of up to 100m, a depth not unusual for oil and gas fixed platforms.

Required for access to wind farm sites in water depths not suitable for fixed bottom foundations. The different concepts foreseen for floating OSS foundations are similar to designs utilised for wind turbines: semi-submersibles, tension leg platforms (TLP), barge, or even spars.

2 2,000 2 2,000 2 2,000 4 Component

4,000

number projections for Scotland based on 1,000 substructures.

Image credit: Jason Bauer of NREL

Per Substructure Total Component

Scotland OW Supply Chain

Scottish Development International

Scottish Development International (SDI) is Scotland’s international trade and investment agency. HQ in Glasgow + 30 offices in the world including an office in Paris

• One stop shop for French companies to connect to Scotland’s offshore wind ecosystem

• Support the internationalisation of the Scottish supply chain

Our partners in Scotland:

- Deepwind Cluster

- Forth and Tay cluster

- Aberdeen Renewable Energy Group (AREG):

- Scottish Renewables

Our partners in France:

- Local clusters: Bretagne Ocean Power (BOP), Wind’Occ, Neopolia, Normandy Maritime

- Pôle Mer Méditerranée/ Bretagne Atlantique

- Evolen

-

ORE Catapult/ Floating Wind Centre of Excellence

- France Energies Eoliennes (FEE)

- Business France

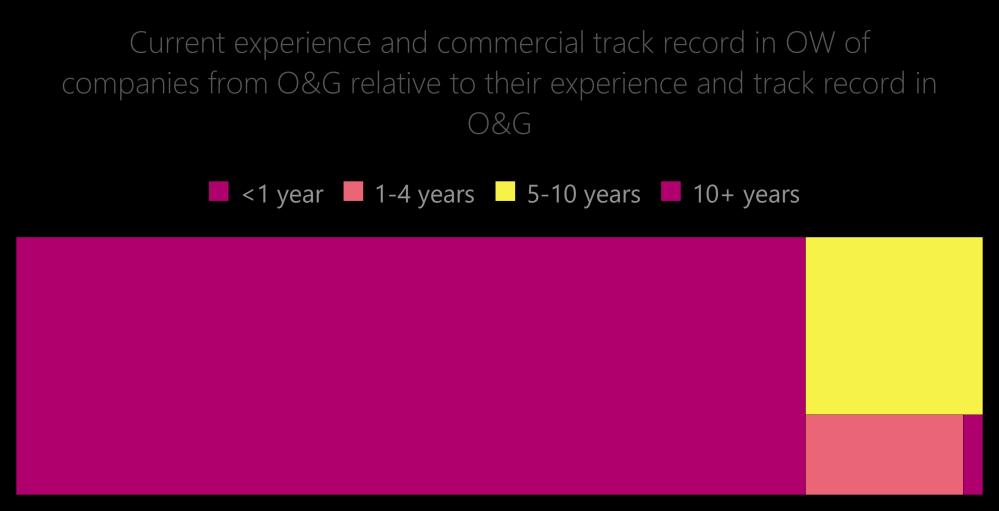

Scottish supply chain is experienced

• Scottish OW companies come from:

- Oil and Gas (most representative)

-

Marine/Maritime

-

Subsea Engineering

- Ports and Harbours

-

Civil Engineering

• Strong experience with offshore energy asset development, maintaining and decommissioning

• Most of the Scottish OW companies from the O&G sector have +10 years of experience in O&G

Marine/Maritime 25% Oil and Gas 26% Ports and Harbours 17% Subsea Engineeri ng 19% Civil Engineering 13%

Scottish supply chain is international

No, we are not exporting to offshore wind clients overseas

• 34% of our OW supply chain is currently exporting overseas

No, we are not exporting to offshore wind clients overseas, but we are exporting to other clients overseas in allied industries

• 65% of the Scottish supply chain has international trade records in the OW industry or allied industries

Yes, we are exporting to offshore wind clients overseas

• Southern Europe including France is one of the top market of interest

Current Export Markets

34% 31% 35%

OSW

Current

Export Status

0 50 100 150

- North Sea Europe - Baltic Sea Europe - South APAC - South East Asia USA Ireland APAC - Other South America China Other markets

Europe

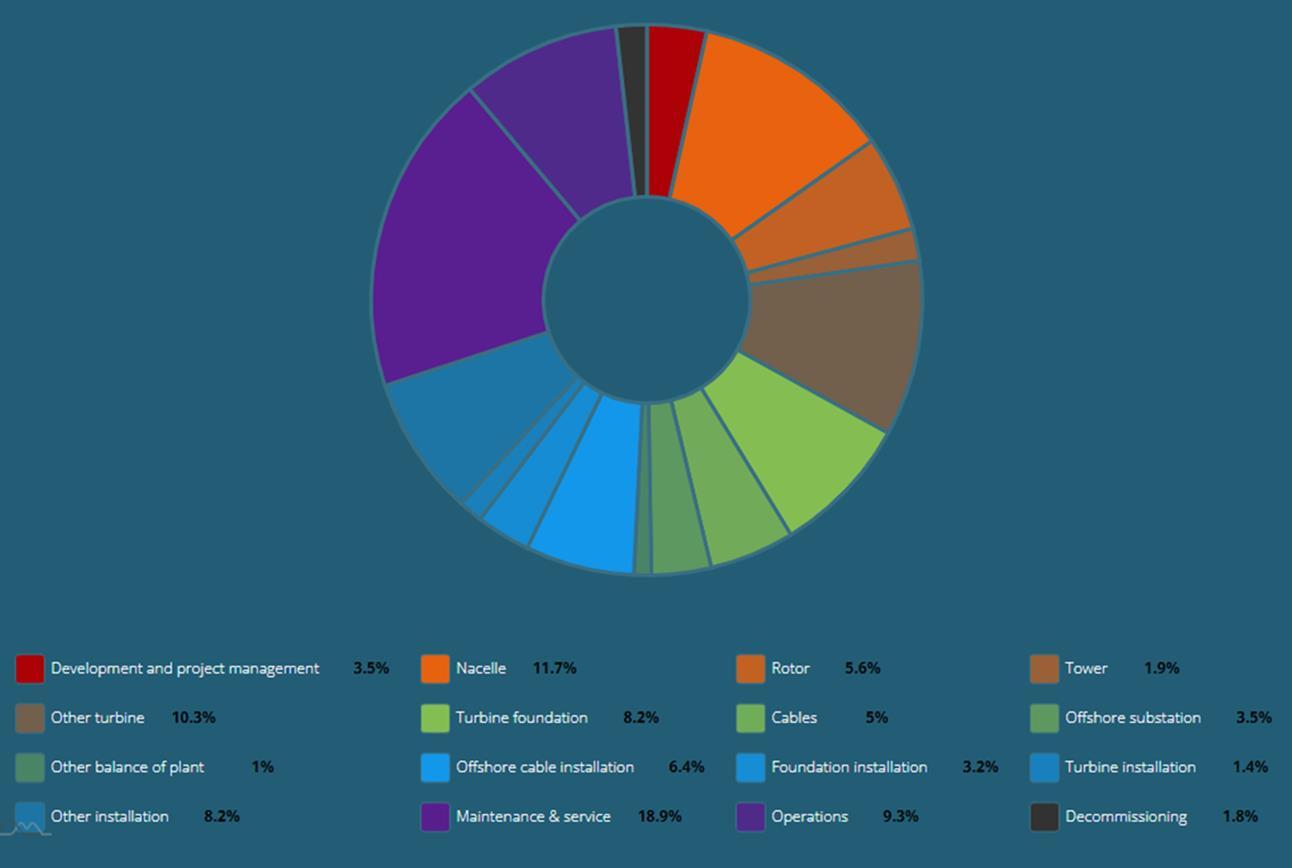

Supply chain capabilities overview

The Scottish supply chain cover all the value chain and most of the companies are working across several activities

Most of the Scottish companies are Tiers 2/3 and could be subcontractors for the manufacturing of small components

Project Development and O&M are the most represented activities with 205 and 218 companies

Specific experience and innovative capabilities for the French market:

• Project development: Site surveys & assessments, UXO, engineering services

• Subsea Engineering: mooring systems, offshore cable

• Assembly of substructures

• Offshore services: Installation, equipment provider

• Assets maintenance and digitalisation: CTV,

Source: Xodus survey OW Supply Chain in Scotland

The portal for Scottish Industry Directories

preventive maintenance, sensors No. of Companies Development and consenting services 71 Site surveys 67 Resource and met-ocean assessment 76 Engineering services 143 Turbine manufacturing 46 Turbine foundation manufacturing 125 Array and/or export cables manufacturing 62 Offshore substation manufacturing 76 Onshore substation manufacturing 59 Turbine T&I 29 Turbine Foundation T&I 64 Offshore electrical infrastructure T&I 74 Onshore electrical infrastructure T&I 19 Port and logistics (T&I) 119 Access and transfer operations 63 Port and logistics (O&M) 58 Maintenance and service activities 131 Health and safety 45 Hardware, software and digital services 97 Decommissioning activities 66 Repowering activities 14 Port and logistics (EoL) 105 Sector Support Sector support services 179 Sector Coupling Sector coupling solutions to offshore windfarm developments 63 Project Development Manufacturing Transport and Installation (T&I) Operations and Maintenance (O&M) End of Life (EoL)

Supply chain and collaboration opportunities

Scotland identified several areas of the supply chain that offer immediate opportunities for manufacturing companies:

• Export cable manufacture

• Array cable manufacture

• Large castings and forgings (wind turbine rotor hubs, bedplates and drive shafts)

• Offshore wind turbine blades (blade lengths greater than 100m)

• Offshore electrical substation topsides

• Large gauge mooring chain for floating wind

• Substructures (floating)

Scotland and France collaboration on key challenges:

• Cost reduction especially on subsea engineering and O&M

• Support the development of a regional supply chain

• Reducing project risk by partnering with experienced and innovative companies

• Ports and infrastructures for commercial projects

Meet with the delegation at FOWT

15 Scottish companies

Covering the entire supply chain

Catalogue with their capabilities available

•

•

•

Meet with the delegation at FOWT

Wednesday 10th May

DAY 1 from 4:30 pm–

Exhibition area

Thursday 11th May

DAY 2 from 8:30– 4th Floor Meeting room KL

Breakfast Session: Scotland and the UK

Floating Wind Opportunities

Meet with the delegation at FOWT

Julien Rapenne

Senior International Trade Specialist

julien.rapenne@scotent.co.uk

+33 (0) 6 85 78 00 88

Nindy Bhari

Senior International Trade Specialist

nindy.bhari@scotent.co.uk

+44 (0) 782 798 1425

Many benefits to choosing the UK

▪ Top European/3rd global best location for scale-up investments

▪ Lowest corporate tax rate in the G20

▪ Flexible employment law that supports growth

▪ Easiest place to obtain credit in Europe

▪ Home to 4 of the top 10 universities in the world

▪ Strong policy to support a green industrial revolution

Policy

Powering Up Britain is the Government’s blueprint for the country’s energy future. It brings together our Energy Security Plan, and Net Zero Growth Plan to explain how to diversify, decarbonise and domesticate energy production. It presents the opportunities in Carbon Capture, Usage and Storage, Floating Offshore Wind Manufacturing, and Hydrogen.

The 10 Point Plan is designed to stimulate private sector investment and manufacturing to deliver audacious net zero goals, creating unique opportunities for investors of all kinds.

Opportunities from Land's End to John O'Groats

The Investment Service Team (IST) delivers an end-to-end investment service on behalf of DBT

▪ DBT’s delivery partner providing an end-to-end service for foreign companies seeking to invest and expand in the UK ▪ Connects investors into a large network of policy and business support

▪ Works across all sectors and markets in conjunction with DBT ▪ Approx 110 FDI professionals UK wide.

Official – Sensitive

Energy Transition & Infrastructure sector propositions

▪ Sector overviews

▪ UK strengths in the sector

▪ Key opportunities for investors

▪ Industry support

▪ Research capability

▪ Key companies and FDI case studies

▪ Key UK locations and clusters for the sector

Propositions available on Internal InvestmentAtlas https://dbis.sharepoint.com/sites/InternalInvestme ntAtlas 7

Here to help you find expertise for your projects in the UK and abroad

INVITATION - Offshore Wind deep-water port manufacturing: Investment

Opportunities in Teesside and the Humber

Tap into an exceptional opportunity to become part of Teesside and the Humber's established and thriving offshore wind supercluster. Companies looking at UK expansion can benefit from large, upgraded quayside to test, develop and manufacture components and subcomponents to deploy offshore wind farms in the North Sea and further afield. You will also be able to enjoy the benefits associated with the Freeport status of Teesside and Humber.

The Department for Business and Trade will host two webinars on:

• 17th of May from 08:00 to 09:00 (BST)

• 25th of May from 16:00 to 17:00 (BST)

We will be joined by Siemens Gamesa, SeAH, SSE, and Orsted. It will be a great opportunity for your business to hear from them and the opportunities in offshore wind that they see in the region.

To register and find more information about the webinars, please follow this link: https://www.events.great.gov.uk/hpo-offshorewind-teessideandhumber

Contact us

Julien Danne

• Head of the Clean Growth Team, British Embassy Paris

• Tel: 0033 688 391 132

Mia Barclay

• Renewable Energies and Environment, Senior Trade and Investment Adviser, British Consulate Bordeaux

• Tel: 0033 608 963 798

Catherine Cestari

• Hydrogen Trade and Investment Adviser, British Consulate Bordeaux

• Tel: 0033 603 856 638

• firstname.surname@fcdo.gov.uk