AUTOMOTIVE RENAISSANCETOM PARRYYEAR 5 @unit14_ucl UNIT Y5 TP

THE

All work produced by Unit 14

Cover design by Charlie Harris

www.bartlett.ucl.ac.uk/architecture

Copyright 2021

The Bartlett School of Architecture, UCL All rights reserved.

No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage and retrieval system without permission in writing from the publisher.

-

@unit14_ucl

-

twjparry.archi@gmail.com

@archi_parry

THE AUTOMOTIVE RENAISSANCE

BRITISH LEYLAND REBUILT

Birmingham, England, UK

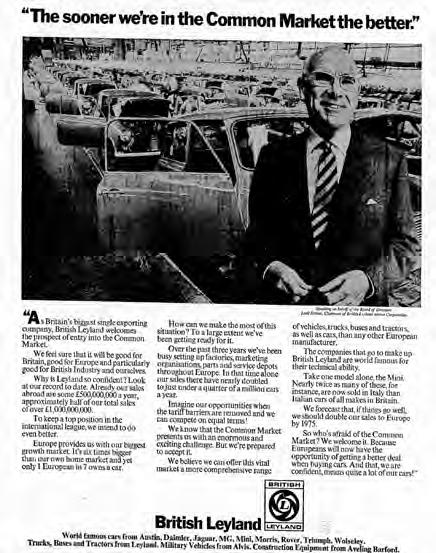

TThe project follows the narrative of the UK’s need to reclaim its lost manufacturing sector, as it adapts to changing trade dependencies and the need for economic specialisation. In response, the former national conglomerate, British Leyland, is revived to fill the void that once was the British automotive industry, as a strategy to spark a manufacturing renaissance. As the UK’s historic centre of the automotive industry, Birmingham is the natural home to locate the new British Leyland headquarters.

The project itself seeks to embody the automotive renaissance brought about by a revived British Leyland through its Birmingham headquarters. In partnership with HS2 and Formula E racing, would become a multifaceted hub of automotive activity in the centre of Birmingham. As the destination gateway into Birmingham via HS2, the project links directly to the rest of the UK with ease, while the spectacle and competitive nature of Formula E drives automotive innovation, demonstrated on an international stage.

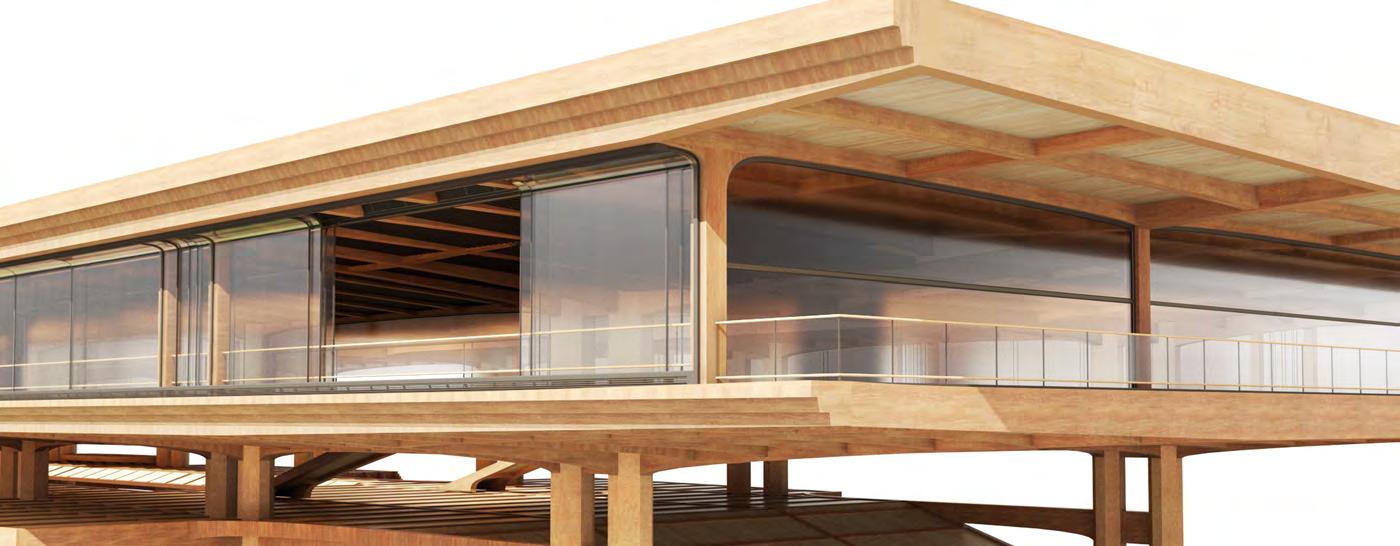

While embodying the symbolic headquarters of British Leyland, as it is compartmentally diversified throughout the city, the building itself is a figurehead of new technologies and practices of the industry. The public journey of the building enables visitors to customise and create their own cars as they become integrated in the manufacturing process, while exploring British Leyland’s heritage and contemporary collections. Constructed from mass timber glulam and CLT, the structure reflects both the contrast of nature and machinery, while also demonstrating the shift towards an environmentally conscious industry. The building form’s transparencies intend to merge with the site and showcase the industry, as the building becomes an all-encompassing shelter for its multifaceted programmes.

TOM PARRY YEAR 5

Y5 TP

ArtefactStudies+DesignFragments InitialConceptResearch

01

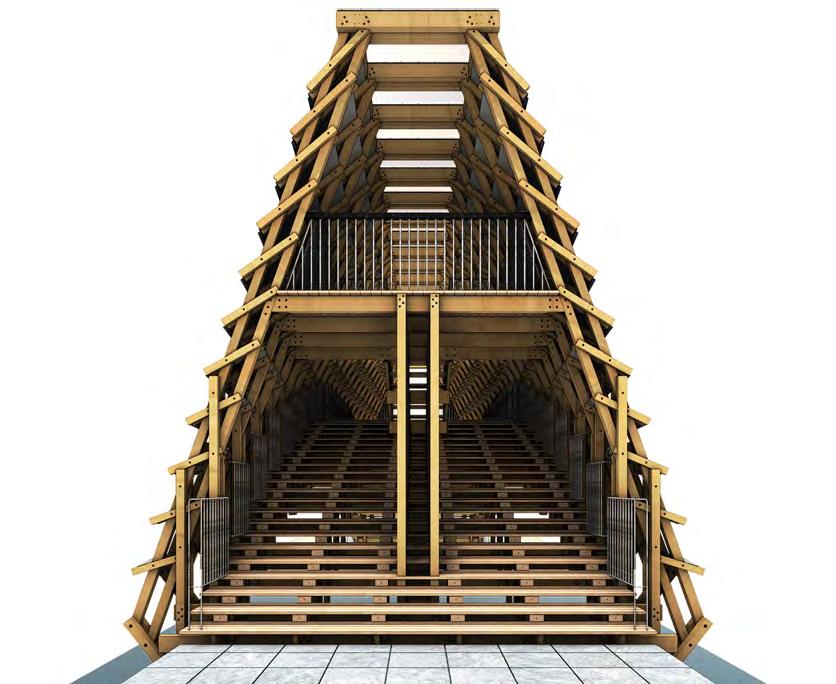

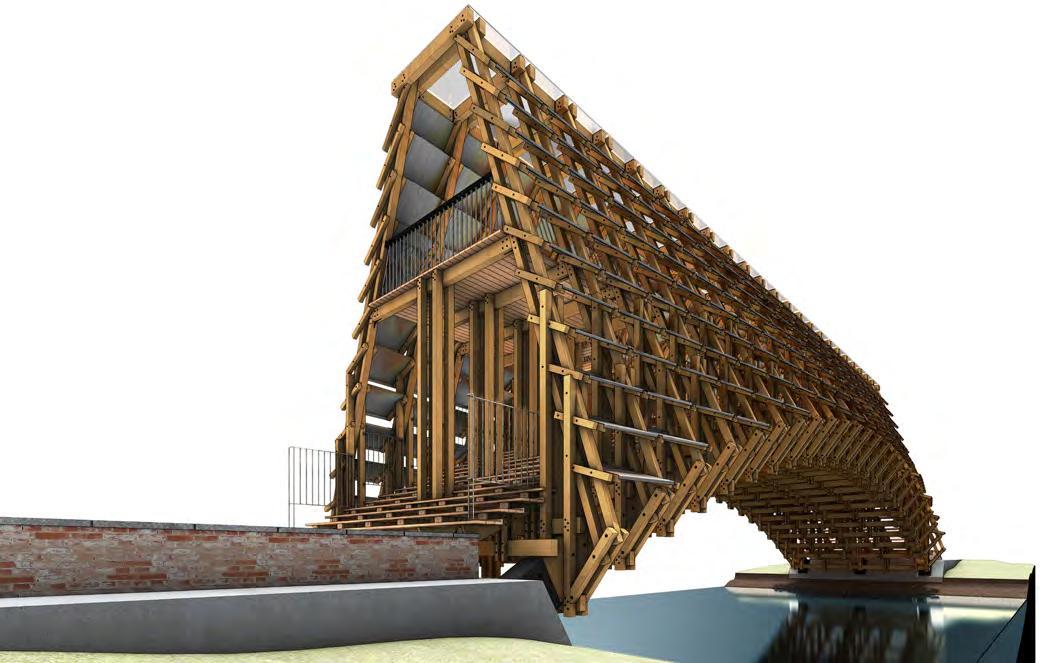

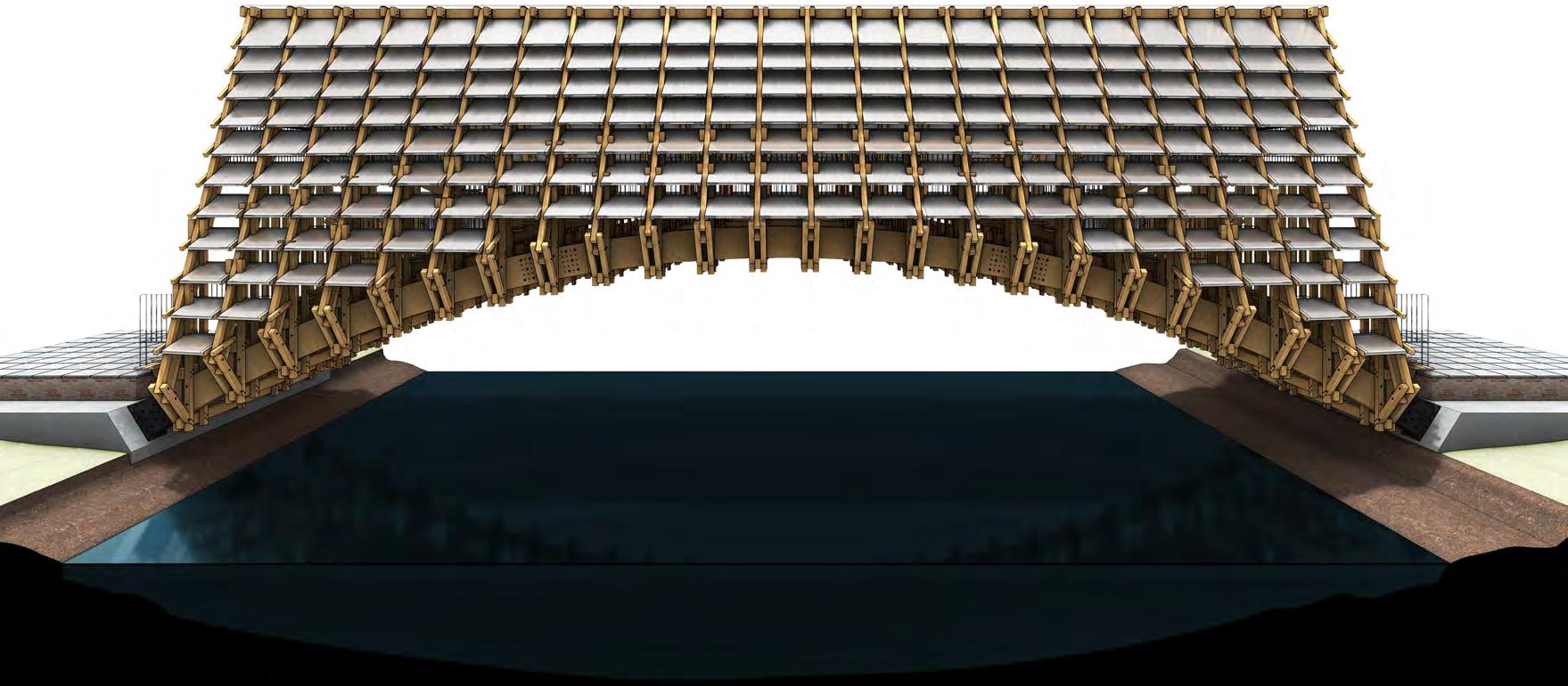

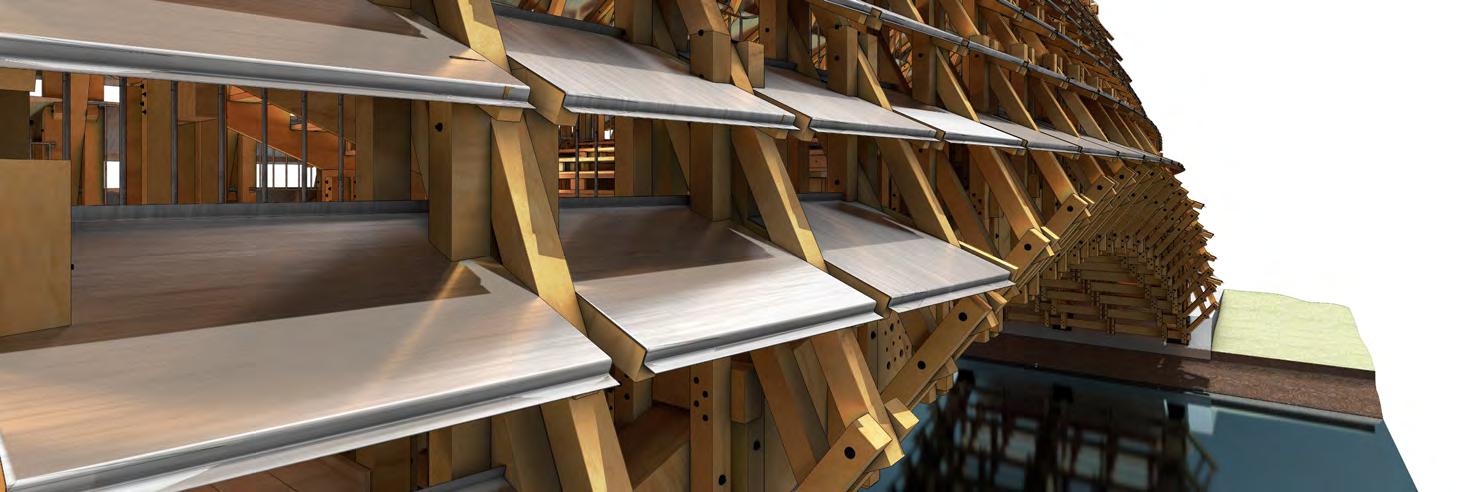

KnownsimplyasTimberBridgeinGulou Waterfront,thisstructurebyLUOStudiosisa primeexampleofcontemporarymasstimber architecturethatevokestraditionaldesign. Builtin2022,thepedestrianbridgeemploysa kitofpartssystemassembledatoptraditional archedspanningbeamstoenablepassageof boatsbeneath,whilealsoenhancingstructure.

Intendedtodifferentiatefromlocalurban constructionsthroughitsuseoftradtional timbermaterialandstructuralelements, thebridgegivesconsiderationtoits contextinbothdesignandnon-invasive construction,assembledwithsteelbolts.

TimberBridgeinGulouWaterfront,LUO TIMBER BRIDGE

TimberBridgeinGulouWaterfront,LUO INTERLOCKING TIMBER SYSTEM

The4marchingstructure,formedbythree parallelbeamsspanning25.2m,enableslevel changesthroughoutthebridge,creatinga centralplatformalongwithplatformsateach end.Theshelteredinteriorspacegivesgreater opportunitytoinhabitthebridge,givinga senseofceremonywhencrossing.

TimberBridgeinGulouWaterfront,LUO STRUCTURAL FRAGMENT

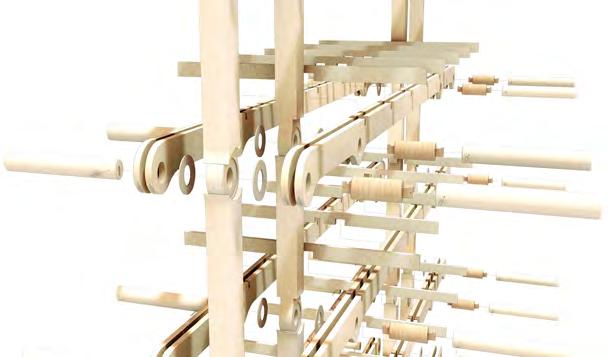

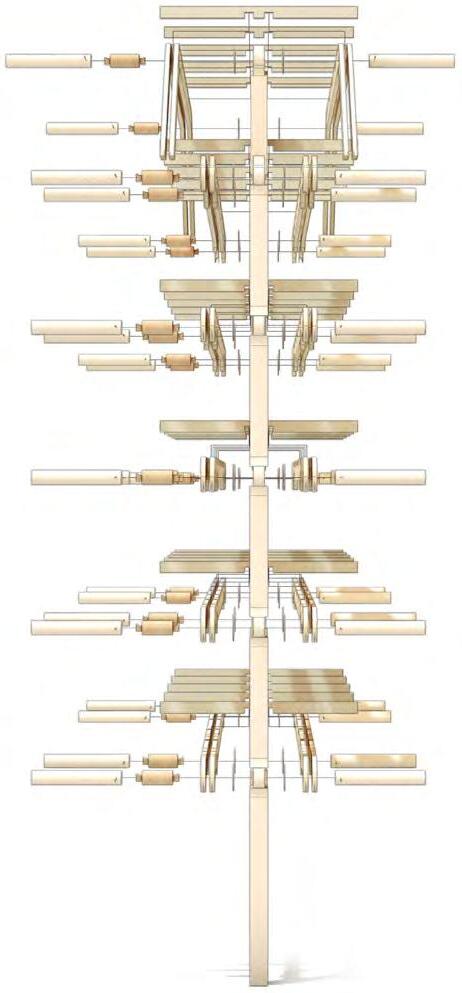

ExplodedanalysisoftheTimberBridge’skitofpartsassembly.Examining themodularprefabricationoftimbercomponentsbeingassmbledin repeatingformationtocreateacomplexyetsimplestructuralexpression.

TimberBridgeinGulouWaterfront,LUO COMPONENT ASSEMBLY

Anexperimentalfragmentinextractingthe TimberBridge’skitofpartsstructure,seeing howprefabricatedsmallerpartsmightbe assembledtoformlargerstructuralelements.

DesignFragmentOne EXTRACTED STRUCTURE STUDY

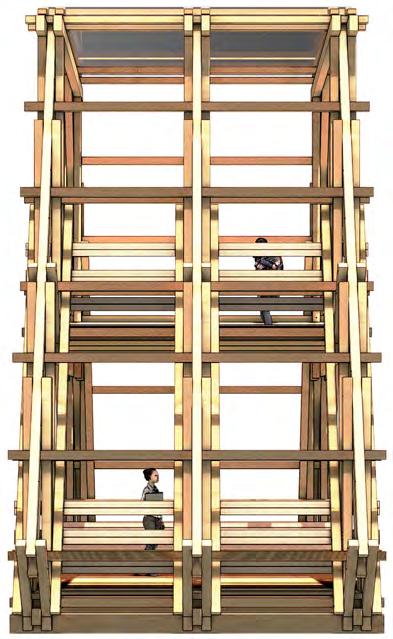

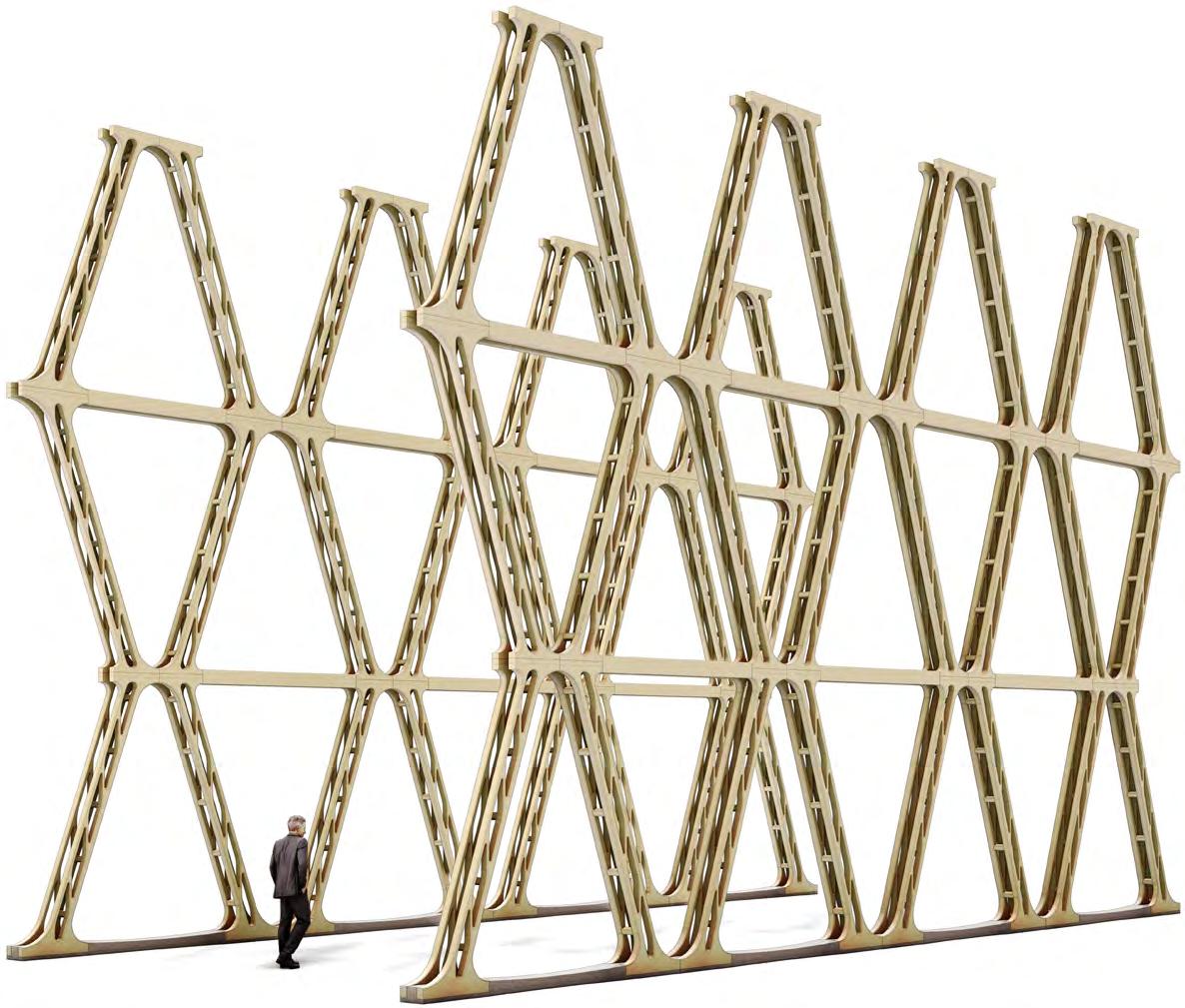

ReinterpretingthestructureofTimberBridge again,ontoalargerscalewheretheexpression ofrepetitionissimplifiedandcondensedto formalargeA-framestructure.

DesignFragmentTwo SCALED STRUCTURAL FRAGMENT

RefiningthetimberA-frameexplored previously,creatingmodularstructural elementsfromprefabricatedsmallertimber compnonents,combinedtoformatruss systemwhenassembledinalinearformtion.

DesignFragmentThree TIMBER A-FRAME COLUMNS

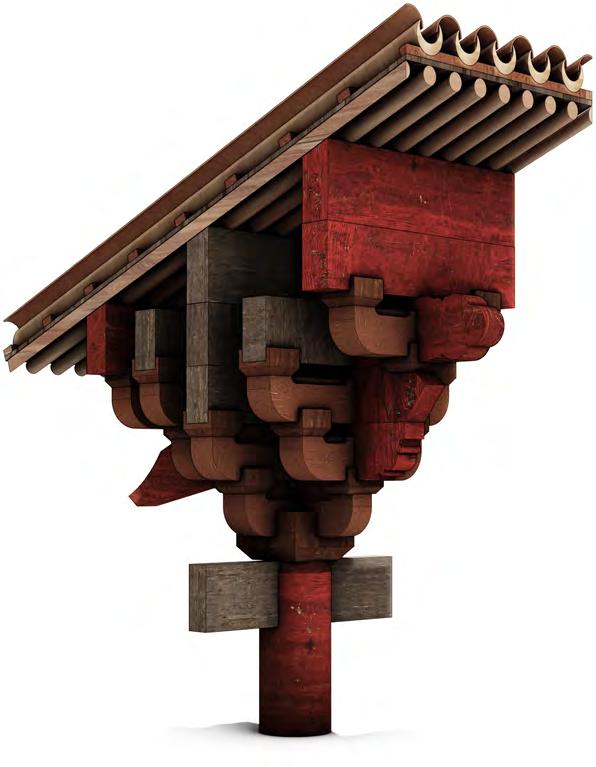

Thetraditionalmethodofinterlockingtimberstructuralcomponentsonwhich TimberBridgeisbased,DougongistheancientChinesesystemofinterlocking timberbracketstoenhancestructuralcapacities.Recognisedalsoforits culturalimplicationsandtraditions,dougongstructuresavoidanyadditional fixingdevices,relyingonprecisecarpentry.

Theincreasingsurfaceareaandstructuraljunctionsprovidedbythedougong atopacolumnenablesgreaterloadbearingcapacityfromthesinglecolumn, creatingamorestablebaseonwhichtosupportroofandfloorbeams.

DougongStructuralSystem DOUGONG COLUMN STUDY

DougongStructuralSystem INTERLOCKING MODULAR BRACKETS

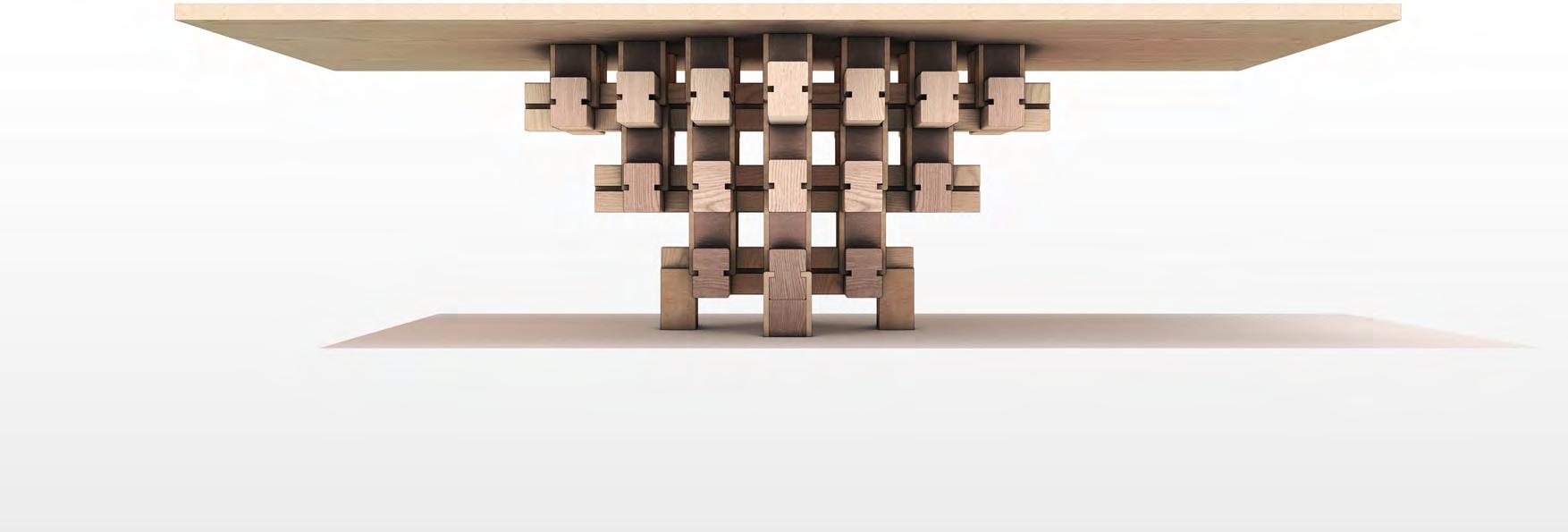

Acontemporaryinterpretationofdougong,simplifingthe bracketelementsintotwotypes,eachofwhichfollowinga simplicityofformtoassembleintoacomplexgeometry. Whileappliedtoatable,theextractionofkeyprinciples fromdougonginthisformcanbeenhancethroughease ofprefabricationandmodulardesign.

TheDougongTable,MianWei SIMPLIFIED CONTEMPORARY INTERPRETATION

Aninterpretationofthedougongsystemwherebythesurfacearea increasesexponentiallywithheight,utilisingdowelassembleyto enhancestructuralcapability.Alsoenablingfloorbeamstoextrude atvariouslevelswherenecessary,creatingacomplexformfroma kitofpartsthatmightbeadaptedwherenecessary.

DesignFragmentFive DOWEL + BRACKET COLUMN

DesignFragmentFive DOWEL ASSEMBLY DETAILS

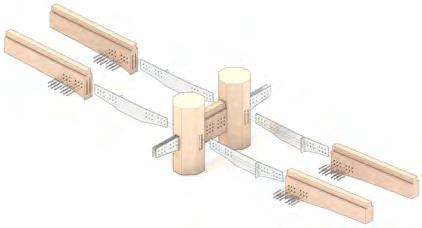

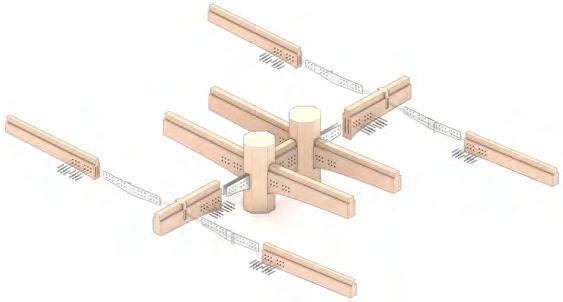

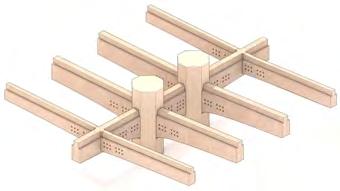

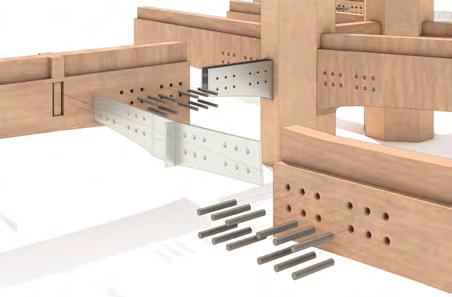

Auniquestructuralsystemcomprisedentirelyof timber,withoutsteeljointsorbraces,eachcolumnis adjoinedtotwoparallelbeamsoneitherside,joined byanovalbeamthatslotsthroughtheseelementsto formarigidjoint.

InitialConceptResearch | TamediaNewOfficeBuilding,ShigeruBan

FULLY TIMBER STRUCTURE + JOINTS

Thebuilding’sstructuralsystemperformssimilarlytothatof anenlargedkitofparts,utilisingrigidjointstoavoidexcess components.Thelargespanningwidthofthebeamsisenabled throughthesmallerendscectionsoftheloadbearingbeams beingsupportedbytwosetsofcolumns,alsoformingasan intermediatespaceforthebuilding.

InitialConceptResearch | TamediaNewOfficeBuilding,ShigeruBan PREFABRICATED TIMBER

MASS TIMBER MaterialResearch Panellised Mass Timber Volumetric Modular Post and Beam Facade Panels Internal Walls Columns External Walls Suspended Floors Facade Panels Volumetric Modules Floors Beams Internal Walls Typical Structural Systems Timber Flooring Glulam Column Glulam Beam Engineered Bolts 7-Ply CLT Steel Plate Joint Steel Bracket Exploded Fragment Assembled Fragment Black and White Building Fragment LaminatedVeneerLumber - LVL Application Beam / Column / Cord Interior Usage MassPlywoodPanel - MPP Application Roof / Wall / Floor Interior / Exterior Usage ParallelStrandLumber - PSL Application Beam / Column Interior Usage LaminatedStrandLumber - LSL Application Beam / Wall Interior Usage NailLaminatedTimber - NLT Application Roof / Wall / Floor Interior / Exterior Usage GlueLaminatedTimber - Glulam Application Beam (long span) / High Loading Interior / Exterior Usage CrossLaminatedTimber - CLT Application Roof / Wall / Floor Interior / Exterior Usage DowelLaminatedTimber - DLT Application Roof / Wall / Floor Interior / Exterior Usage Mass

Timber Types

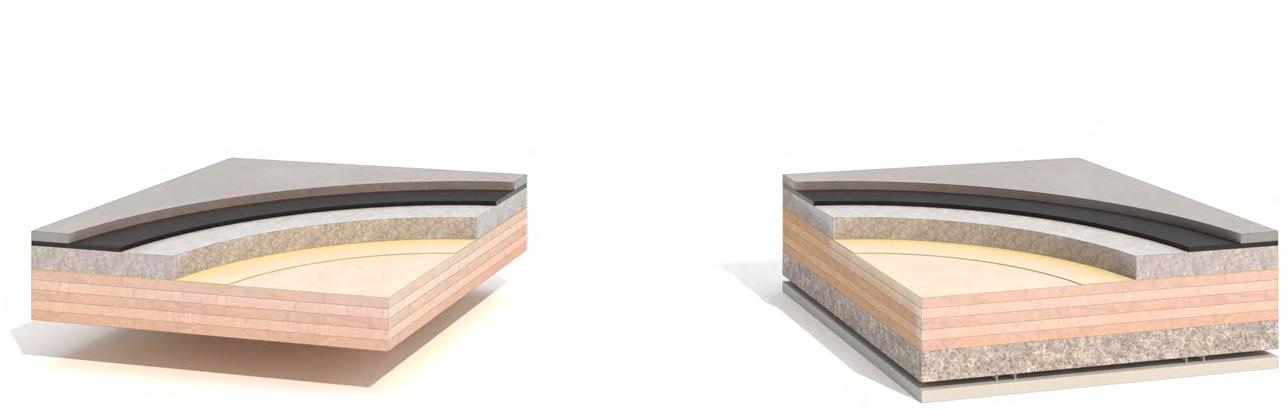

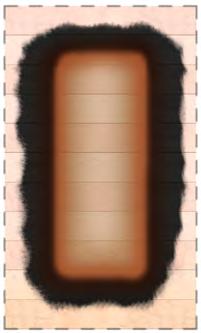

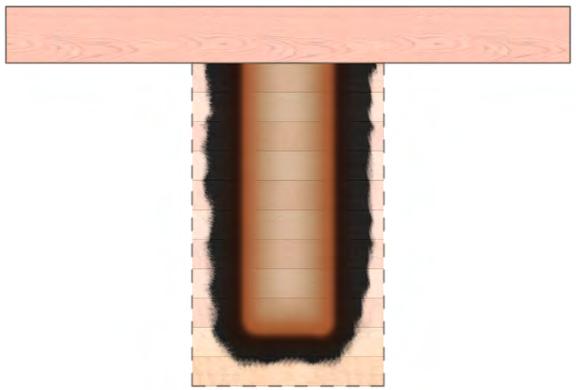

PASSIVE FIRE DESIGN MaterialResearch 25mm dry screed 12mm recycled rubber sound absorption layer 60mm flooring grade rigid wood fibre insulation Breathable floor protection membrane 30mm fire protection boarding 75mm sheepwool insulation within 95mm cavity 130mm (5 ply) CLT

90minsFR 60minsFR Typical Floor Buildup

CLTFloorwithExposedSoffit CLTFloorwithSuspendedCeiling

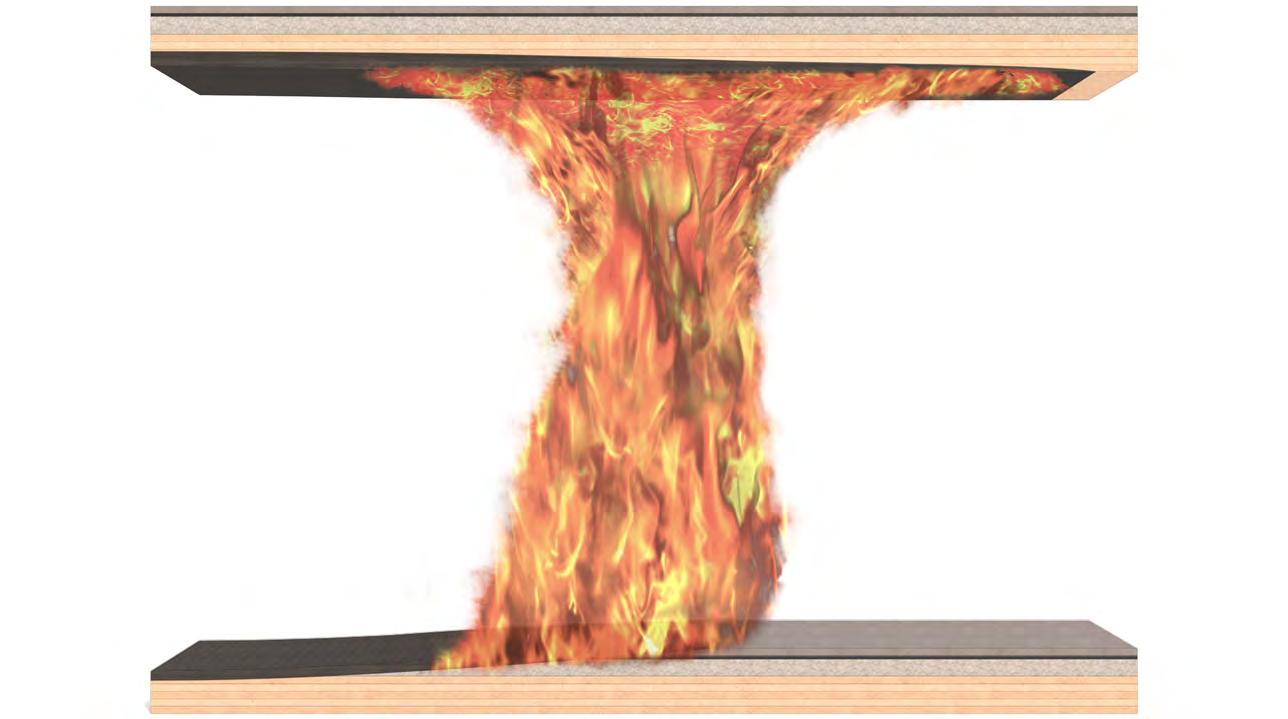

Pyrolysis gases

Leading edge

at ceiling Thin initial char layer

Unburnt fuel on the floor

Leading edge

Burnt

Trailing edge at ceiling Flaming region Growingcharlayer Flaming CLT Aheadoffire Smouldering char Well-developedthickercharlayer Heat radiation FIRE SPREAD Fire Spread Dynamics

Cold wood Consumed wood Heated zone Char layer b b B B d D d D Charring Barrier

Trailing edge

out fuel on the floor

ExposedGlulamBeamSupportingFloorSlab FullyExposedGlulamBeam

c.3,200 BCE CHARIOTS Ancient Greeks repurpose potter’s wheels.

1884 PETROL ENGINE The first internal combustion engine invented by Edward Butler.

Invented

SELF-DRIVING Google begins its self-driving car project.

TESLA AUTOPILOT

Bothcarsandarchitecturehave undergonehistoriesofevolution andrefinement,influencedbut culturalandtechnologicalchanges.

BRICK c.9,000 BCE

Sun baked clay bricks first appearing in the Middle East.

TIMBER c.8,500 BCE

Earliest recorded wooden hut unearthed in England.

GRANITE, LIMESTONE c.3,100 BCE

Ancient Egyptians the first to use stone structures.

MARBLE c.650 BCE

Ancient Greeks begin building their temples from granit.

Evolutionofbothcarsand architecturehasbeendriven bybothvisualaestheticsand technologicalperformance.

Thecontemporaryfocusofcars beingintergrationofdigital technologiesandsoftwaretomeet usercomfortandsafety,where architectutrealsostrivestoimprove environmentalcomfortand imrpovedfunctionalityofbuildings.

CONCRETE c.20

Developed by the Romans and decribed in recipe by Vitruvius.

GLASS c.100

First appearing in Roman-era Egypt as flattened brown glass.

IRON c.700

Used as a primary structural material by the Tang Dynasty.

IRON (REINVENTED) 1775

Rediscovered as a construction material in England.

Sustainabilityineachindustry hasbecomeasignificantfactor; wherecarsareincreasingly electricpoweredandlightweight toimprovefuelefficiency,biomaterialssuchasmasstimberare growinginusefortheirrecognised sustainabilityandstructural performance.

ENGINEERED TIMBER 1852

First used in England but later poplised by Otto Hetzer.

ASBESTOS 1866

First use as an insulative and fire resistance material in building.

STEEL 1890

Modernised for construction and replacing iron.

PVC 1926

Part of the 20th Century discovery and research into plastics.

REINFORCED CONCRETE 1950

Tensile strength added to concrete with iron/steel.

FLOAT GLASS 1959

Enabling mass production of high quality large glass panes.

TENSILE PLASTIC 1967

PVC tensile membranes displayed at the 1967 Expo in Canada.

ETFE 1982

First used as a building material by Stefan Lehnert.

MASS TIMBER 1998

Cross laminated timber developed by Gerhard Schickhofer

AUTOMOTIVE + ARCHITECTURE EVOLUTION Automotive+Architecture TechnologyinAutomobiles 19 TH CENTURY EARLY 20 TH CENTURY 21 ST CENTURY MID TO LATE 20 TH CENTURY PREHISTORIC

1911

1886 MOTOR CAR Karl Benz patents an automobile powered by a petrol engine. 1891 ELECTRIC VEHICLES Viable electric vehicles introduced but forgotten by the 1930s.

ELECTRIC IGNITION

by Charles Kettering and first used in 1912 Cadilacs. 1908 FORD MODEL T A mass production car developed by Henry Ford. 1926 POWER STEERING

Invented by Francis W. Davis but not used until 25 years later. 1953 AIR CONDITIONING Installed by Chrysler, set to low, medium or high. 1959 SEAT BELTS

1971

safety

1973

toxic emissions from exhaust fumes. 1988

Originally

drivers only. 1994

2000s

hybrid

industry

2010s

Driver safety

such

traffic alerts

2014

Autopilot steering technology is released commercially. 1890 s 1930 s 1960 s 1990 s 2010 s 2020 s MaterialinArchitecture ANCIENT CIVILISATION 19 TH CENTURY 20 TH CENTURY INDUSTRIAL REVOLUTION PREHISTORIC

Invented by Volvo and given to other car makers for free.

ANTI-LOCK BREAKS Developed as a standard

feature.

CATALYTIC CONVERTER Reducing

AIRBAGS

introduced for

ON-BOARD DIAGNOSTICS On board computers to diagnose repair issues.

ELECTRIC + HYBRID REVIVAL The electric and

vehicle

is revived internationally. 2009

DRIVER ASSIT FEATURES

features

as

and 360 sensors.

CONTEMPORRY MODERNISM BAROQUE RENAISSANCE GOTHIC CLASSICAL

LightWeight MassProduction MassCustomisation

StageOne RawMaterialSourcing

StageTwo

ManufacturingProcesses

StageThree

Transportation+Logistics

StageFour

Construction+Installation

StageFive

EndofLifeScenarios

Laminated Veneer Lumber - LVL Mass Plywood Panel - MPP Parallel Strand Lumber - PSL

Strand Lumber - LSL

Laminated Timber - CLT

Laminated Timber - DLT

Laminated Timber - NLT

Laminated Timber - Glulam Peeling ~1.1m

wood

mass timber ~1.8m

2m 3 of wood per 1m

of mass timber Sawing Wood Products Wood Chips + Sawdust 60% 40% CLT Panel Material Efficiency -7% Veneers Timber Drying,

Drying, Planing + Grading

Drying

Bioenergy Production ~2.8m

-

of wood per

of mass timber Logs Sustainable Forestry Reforestation Afforestation Imports Bioenergy Production Non-Timber Forest Products Carbon Sequestering Recreation + Ecotourism Pulp + Paper 15%

Laminated

Cross

Dowel

Nail

Glue

31.4m 3 of

per 1m 3 of

3

3

Cutting + Sorting

Stranding Strands

+ Sorting

3

2.9m 3

1m 3

Imports Construction Prefabrication End of Life Reuse Material Recycling End of Life Disposal Bioenergy Production

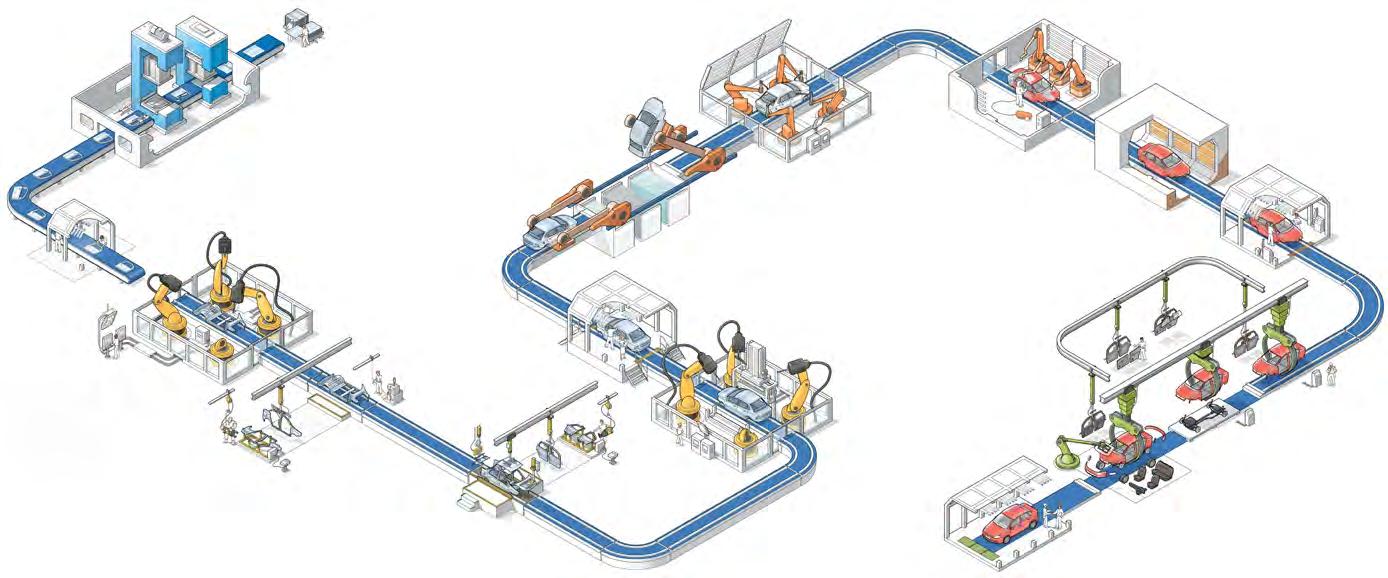

MODULAR MASS TIMBER PRODUCTION Automotive+Architecture

PressShops

BodyShops

a. On-Site BodyFabrication+Assembly

1a. Press Shops Smallermetalworkproduction ofcarbodycomponents.

2a. Body Shops Assemblyofcomponentsto createcarbodyskeleton.

3a. E-Coat + Wash

4a. Paint + Coatings Dippingofassembledmetal bodyinprotectivecoatings. Spraypaintingandheatdrying ofbody+additionaltouches.

5. Final Assembly Assemblyofbody,chassisand othercomponents.

6. Inspection + Testing

7. Shipping + Sales Finalqualitycontrolinspections andperformancetesting. Logisticalorganisationand transportofcarstodistribution andsalescentres.

E-Coat+Wash Paint+Coatings

b. Off-Site PowertrainAssembly+Testing

1b. Metalworking Fabricationofmetalworkengine andchassiscomponents.

2b. Parts Wash Industrialcleaningof componentstoensurethey functionandfit.

3b. Powertrain Assembly Finishedassemblyofcarengine andchassis.

4b. Testing Qualitycontroltestingof electricalandmechanical components.

Raw Materials

Comparisonofthesupplychainsandproduction processesofmasstimberandcars,whereboth followstandardisedlinesofproductiontocreatea modularfinalproduct.Thedevelopmentofspecialised manufacturing,suchasCNCmachining,usedinboth allowingforgreaterprecisionandmaterialefficiency.

FinalAssembly Inspection+Testing

Stage4a

Stage1a Stage2a Stage3a

Stage5 Stage6

Raw

Outsourced Components

Materials

Outsourced Components Outsourced Components

MODULAR CAR PRODUCTION Automotive+Architecture

NarrativeContext MadeInBritain

02

WhereoncemanufacturingwasastapleoftheBritisheconomy,ithasbeeninconstantdeclinesince the1970s,primarilyduetoashiftintotertiaryserviceindustries.WhilethevalueofUKmanufacturing hasremainedsomewhatconsistentandlabourproductivityisincreasingmoresothattheUKaverage, thisisduetoafocusonspecialistmanufacturing.Employmenthasfallenby60%since1979and manufacturingcomprisesjust10%ofthewholeeceonomy.

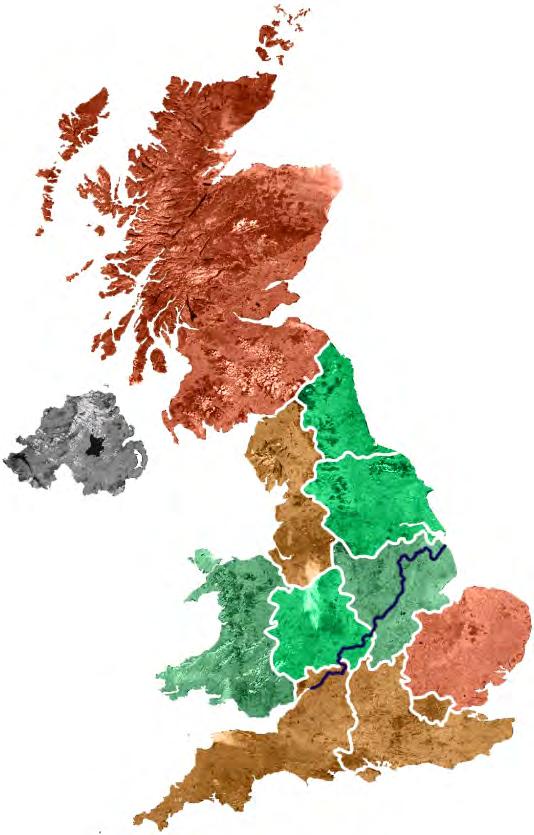

THE DECLINE OF BRITISH MANUFACTURING BritishManufacturing 14.0bn £ Scotland 180,000 6.5% 11.0% 45.6% 2020:5.6 | 2021:4.5 7.1bn £ NorthEast 115,000 9.6% 14.8% 61.7% 2020:6.0 | 2021:6.3

£ NorthernIreland 89,000 10.2% 14.3% 54.9% 2020:3.9* *averageforprevioustwoquarters 24.2bn £ NorthWest 318,000 8.8% 15.5% 46.4% 2020:6.1 | 2021:6.2 17.5bn £ WestMidlands 323,000 11.0% 14.8% 47.0% 2020:5.9 | 2021:6.4 9.4bn £ Wales 156,000 10.7% 16.8% 67.1% 2020:5.9 | 2021:6.7 12.5bn £ SouthWest 236,000 7.9% 10.5% 41.7% 2020:6.2 | 2021:6.0 15.5bn £ Yorkshire+Humber 293,000 10.6% 15.0% 55.0% 2020:5.7 | 2021:6.1 15.9bn £ EastMidlands 293,000 12.4% 17.1% 52.3% 2020:5.7 | 2021:6.6 16.7bn £ EastofEngland 217,000 6.9% 12.2% 52.6% 2020:6.1 | 2021:5.7 8.3bn £ London 127,000 2.2% 2.3% 43.4% 2020:6.3 | 2021:6.4 19.0bn £ SouthEast 279,000 5.6% 7.8% 48.8% 2020:6.3 | 2021:6.4

ManufacturingOutput £ EmploymentinManufacturing Manufacturing%ofTotalEmployment %ofRegionalOutput %ofManufacturedEUExports 2020/21:BusinessConfidenceIndicator BusinessConfidenceIndicator Comparedtooneyearago Solidcoloursonmap Positiverelativechangeinconfidence(upperquartile) Negativerelativechangeinconfidence(lowerquartile) Nodataavailable Textiles,wearingapparel Computer,electronic,opticalandelectricalproducts AllManufacturing Rubberandplasticproducts,andothernon-metallicmineralproducts Transportequipment Chemicalandpharmaceuticalproducts Coke,refinedpetroliumproductsandothermanufacturing Basicmetalsandmetalproducts Machineryandequipment Foodproducts,beveragesandtobacco Woodandpaperproducts,andprinting -100% -90% -80% -70% -60% -40% -20% -50% -30% -10% 0% Reduction in Jobs Manufacturing GVA Since 1970 1970 1980 1985 1990 1995 2000 2005 2010 1975 £60bn £140bn 20 £200bn 35 £155bn 29% 26% 23% 18% 10% +£7bn -£1bn +£26bn -£41bn £161bn £186bn £145bn £40bn £120bn 15 £180bn 30 £20bn £100bn 10 £160bn 25 0 £80bn 5 0 -3% -2% -5% -8% Manufacturing GVA % of Total GVA Labour Productivity 1948-2013 Manufacturing Services WholeEconomy 1948 1958 1963 1968 1973 1978 1983 1988 1993 1998 2003 2008 2013 1953 400 700 300 600 200 500 0 100 1948 = 100

4.8bn

ManufacturingClusters North-SouthDivide Automotive(SMMT) Food+Drink(FDF) Chemicals(CIA) Aerospace+Defence(ADS) Pharmaceutical(ABPI) RegionDataKey

UnitedStates

2023Rank: 2nd

WorldTotal: 16.6%

AnnualValue: $2.5tn

Automobiles, Chemical, Food Products,Military,Aircraft

MineralFuels,Lubricants,Food, TransportEquipment,Machinery

ShareofManufacturinginGDP

Manufacturingcomprisesunitsengagedinthe physicalorchemicaltransformationofmaterials, substancesorcomponentsintonewproducts.

2021 Solidcoloursonmap

2023Rank:

Agricultural,Machinery,Aircraft, HyrdocarbonProducts Chemicals,ManufacturedGoods, FoodProducts

2023Rank: 7th

Textiles,Vehicles,Chemical, MetalProducts

MotorVehicles,Electrical Machinery,ManufacturedMetals

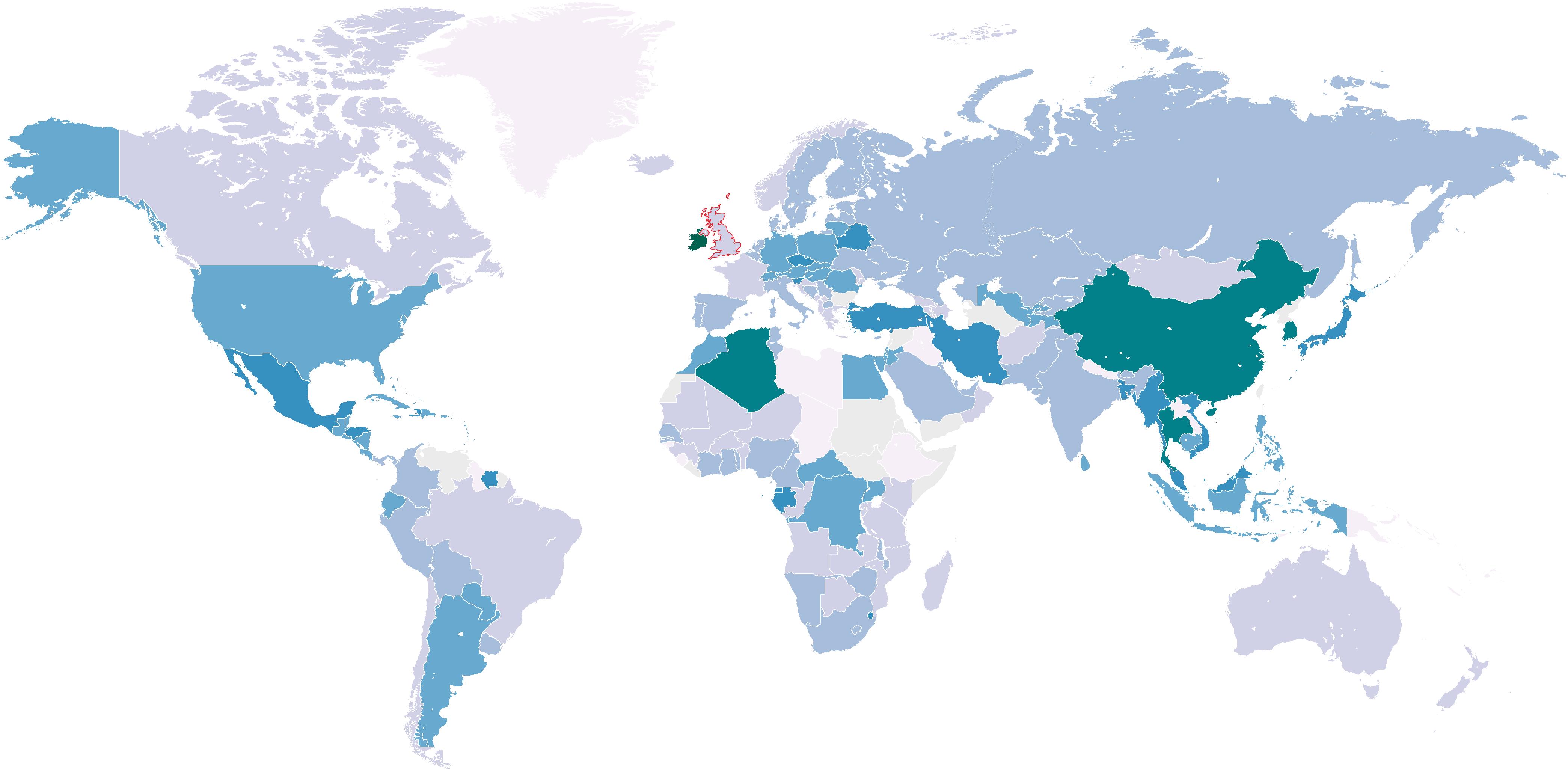

As the UK has shifted to a focus on an economy of services over goods, its specialism in manufacturing has shifted relative to the rest of the world. Vehicles (£34.9bn) and engineered goods (£32.8bn) are the UK’sprimaryexportedgoods,however,invaluetheystilllackconsiderablybehindbusiness(£176.3bn)and financial(£78.2bn)servicesexported. UK’s Position in Global Manufacturing

Agricultural,Textiles,Leather, Chemical,EngineeringGoods

Vehicles,Chemical,Electronics, ComputerParts

SouthKorea

2023Rank: 5th WorldTotal: 3.0% AnnualValue: $0.46tn

TechnologicalProducts,Machinery, Petrolium,Automobiles

WhiledomesticproductionwithintheUKhasrapidlydecreasedsincethe90s,thevalueof thosegoodsisstillsubstantialenoughtoplaceithighlyintheglobaltable,althoughthis tooisgraduallingfallinginrecentyears. UK Manufacturing Output Rankings

Manufacturing by Output (GVA)

DuetothevalueofgoodsproducedbytheUK,moresothanitphysicaloutput,ithasconsistentlyplacedwithinthetop11countries.ThreeofthetoptenbeingEUcountries,the UKisplacedinmoredirectcompetition.

as Share of

Between1970and1995,theUKandChinawerecomparableinmanufacturingoutput,but aseachfocusedmoresooneithergoodsorservices,avastdisparityhasemergedwiththe UKeversincedeclining.

BritishManufacturing

PRODUCTION 16th 12th 8th 4th 15th 11th 7th 3rd 14th 10th 6th 2nd 13th 9th 5th 1st Canada Mexico France Germany Russia Indonesia Italy Japan Taiwan Brazil India US Spain UK SouthKorea China 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

GLOBAL

Manufacturing

Total 1970 0% 5% 10% 15% 20% 25% 30% 1975 1980 1985 2000 1990 2005 1995 2010 US China UK 1 20 40 60 80 100 120 1970 2010 1975 1980 1985 1990 1995 2000 2005

World

GVA PerCaptia %NationalGVA

WorldTotal:

AnnualValue: $0.45tn

2023Rank: 6th

3.0%

WorldTotal:

AnnualValue: $0.28tn

2.3%

8th WorldTotal: 1.9% AnnualValue: $0.27tn 2023Rank: 9th WorldTotal: 1.8% AnnualValue: $0.26tn

WorldTotal: 1.5% AnnualValue: $0.26tn 2023Rank: 4th WorldTotal: 5.8% AnnualValue: $0.75tn India Italy France UnitedKingdom Mexico Germany

2023Rank: 10th

Nodataavailable 30%+ 25-30% 20-25% 15-20% 10-15% 5-10% 0-5%

2023Rank: 1st WorldTotal: 28.4% AnnualValue: $4.98tn China Commercial,Textiles,Electronics,

WorldTotal:

AnnualValue:

Japan

Garments 2023Rank: 3rd

7.2%

$1.03tn

Annual GDP per Capita

SincetheUKlefttheEUin2016,ithasexperiencedmuchslowergrowthcomparedtootherG7 economies,withinvestmentintheUKhavingplateauedthenfallenintheyearsfollowing.Trade dependancywiththeEUalsoseestheUKimportingsignificantlymorethanexportswiththevast majorityofEUmembers,hamperedbytheinabilitytocompeteinmanufacturingproduction.

1st Germany -£22.3bn

2nd Spain -£12.1bn

3rd Belgium -£10.7bn

4th Netherlands -£9.8bn

5th Poland -£6.9bn

6th Italy -£5.3bn

7th France -£4.9bn

8th CzechRep. -£3.6bn

9th Hungary

-£2.6bn

10th Portugal -£2.5bn

11th Austria -£2.3bn

12th Sweden -£2.2bn

13th Slovakia -£1.8bn

14th Denmark -£1.5bn

15th Romania -£1.5bn

16th Greece -£1.0bn

17th Bulgaria -£0.6bn

18th Latvia -£0.5bn

19th Lithuania -£0.5bn

20th Croatia -£0.4bn

21st Estonia

£0.0bn

22nd Slovenia

£0.0bn

23rd Finland

£0.1bn

24th Cyprus

£0.7bn

25th Malta

£1.3bn

26th Luxembourg

£1.6bn

27th Ireland

£10.0bn

UK-EUTradeBalances UnitedKingdom

EU: <-£10bn

EU: -£10bnto£0

EU: £0to£10bn Europe(Non-EU)

POST-BREXIT BRITAIN EconomicDivide

US EU27 Italy UK Japan Canada Germany France 2016 2017 2018 2019 2020 2021 2022 100 105 110 95 90 2016 = 100 Business Investment in UK and EU UKBusiness Investment EUBusiness Investment UKpre-2016 Trend Q1/2009 Q4/2012 Q3/2016 Q2/2020 Q2/2010 Q1/2014 Q4/2017 Q3/2021 Q3/2011 Q2/2015 Q1/2019 Q4/2022 100 140 120 160 170 90 130 110 150 Q1/2009 = 100

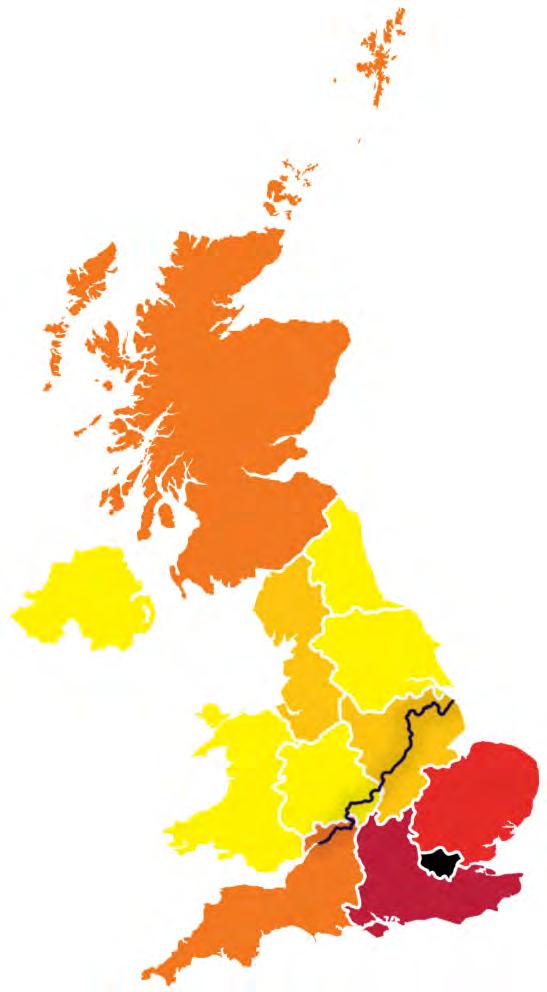

Britain’s least economically successful towns

The southern regions of the UK are generally considered the more affluent, which is reflected in average household incomes. Thenorth-southdividethatexistsbothpoliticallyandculturallyis reinforcedintheUK’sinequitabledistributionofwealth.

most economically successful

THE NORTH-SOUTH DIVIDE EconomicDivide Cambridge 79.5years Liverpool 75.7years Life Expectancy Healthcare Withlessinvestmentandlowerqualityhealthcare,lifeexpectancyand qualityofhealthisreflectedinthis,dividingthenorthandsouthregions entirely. Life expectancy Healthy life expectancy Years SouthEast SouthWest EastofEngland London EastMidlands WestMidlands YorkshireandTheHumber NorthWest NorthEast 0 10 20 30 South North 40 50 60 70 80 South North London £9,176 Yorkshire EastMidlands £7,623 £6,983 Government Spending per Person Employment Economy Growth(2008-2018) SouthWest SouthEast London EastofEngland WestMidlands EastMidlands YorkshireandTheHumber NorthWest NorthEast NorthernIreland Scotland Wales England UK(excl.London) 0 10% 20%

general government spending per region, employment andeconomicgrowthforthesouthtendstobelargerthanthenorth, contributingtothewealthdivide.

Reflecting

Economy + Employment

84.3% £12,543 North East 96.2% £14,301 Scotland -

Cambridge - Oxford - Reading - Aldershot

Hull

Britain’s

towns: - Sunderland - Blackburn - Liverpool -

%ofUKaverage 84-89.9% 90-95.9% 96-101.9% 102-107.9% 108-113.9% 120%+ North-SouthDivide 114-119.9%

UK

88.2% £13,115 Yorkshire + Humber 86.8% £12,910 Northern Ireland 90.0% £13,386 North West 89.7% £13,337 West Midlands 87.9% £13,073 Wales 98.7% £14,680 South West 91.5% £13,611 East Midlands 104.3% £15,509 East of England 128.0% £19,038 London 112.9% £16,792 South East Sunderland Cambridge Hull Reading Blackburn Oxford Liverpool Aldershot NORTH SOUTH

£14,872

Average

Pharmaceutical (ABPI)

Aerospace (ADS)

TheManufacturingFive

Automotive (SMMT)

Chemicals (CIA)

Food+Drink (FDF)

TheManufacturingFive–theAssociationoftheBritishPharmaceuticalIndustry(ABPI),ADS,theChemicalIndustriesAssociation(CIA),theFoodandDrinkFederation(FDF)and theSocietyofMotorManufacturersandTraders(SMMT)–makerecommendationsonhowGovernmentcanworkwiththemtoseizeneweconomicopportunities,sustainjobs, anddelivergrowthandprosperity

1.LevellingUptheWholeUK

“Developtheinfrastructure,skillsandincentivestodevelopnewclustersofadvancedmanufacturingacrosstheUK.”

Itiscrucialforthegovernmenttopromoteinvestmentinadvancedmanufacturingtofulfillitscommitmenttolevelingupthenation.Suchinvestmentholdsthepotentialto positiontheUKcompetitivelyamonggloballeaders.Establishedmanufacturinghubsofexcellence,liketheautomotivesectorintheWestMidlands,Clydeshipyards,andthe chemicalindustryintheNortheast,playavitalroleinsupportingextensiveregionalsupplychainsandemployment.

2.AchievingNet ZeroTogether

“ScaleupandenhancetheindustrialenergytransformationfundtodeliverprogresstowardsNetZero.”

Thecollaborativeaspirationtodecarbonizebothproductandproductionprocessesiswidelyembracedwithinadvancedmanufacturing.WhiletheUKgovernmenthasestablished ambitioustargets,realisingthesegoalsnecessitatesaclosepartnershipwiththeindustry.Giventheenergy-intensivenatureofcomplexmanufacturing,itisimperativefortheUK toremaincompetitiveandseizeemerginglow-carbonprospects.CompaniescontemplatinginvestmentsintheUKprioritizefactorssuchasenergycostsandsecurity.

3.BuildingaScienceSuperpower

“ExpandincentivestoattractsignificantR&Dinvestment.”

Aspiringtoallocate2.4%oftheGDPtoResearchandDevelopment(R&D)withthegoalofbecominga“ScienceSuperpower”necessitatesacollaborativeeffortbetweenthe governmentandtheindustry,coupledwithfocusedinitiatives.Thedecisionsmadebymanufacturersintheirinvestmentstodaywillshapethetrajectoryofthenextdecadeof financialcommitments.TofosterR&Dinvestment,thegovernmentshouldbroadenincentives,incorporatingcapitalasaqualifyingexpenditureunderR&Dtaxcredits.

4.Designing+MaintainingWorld-ClassRegulatoryFrameworks

“EstablishacoherentstrategyfortheUK’sregulatorapproachformanufacturingsectors,thatdeliversalevelplayingfield andmaintainsthehigheststandardsofqualityandsafety.”

ThegovernmentshoulddefinetransparentguidelinesforeffectiveregulationwithintheemergingregulatorylandscapeoftheUK.Theseguidelinesshouldprioritizeminimizing businesscostsandthoughtfullyaddressanypotentialinternational,regional,ordevolvedvariationsthatcouldaffectcompetitivenessorposeobstaclestotradewithcrucial partners.Domesticdivergenceshouldonlyoccurwhennecessaryorwhenadistinctadvantage,identifiedincollaborationwithindustry,isevident.

5.SupportingInternationalLeadership+GlobalBritain

“Placeadvancedmanufacturingattheforefrontofalong-termExportStrategy,developedwiththeindustry.”

Tofostermanufacturinginvestmentininfrastructure,machinery,equipment,andresearchanddevelopment(R&D),thegovernmentshouldestablishaninternationallyappealing fiscalenvironment.Specifically,maintaininggloballycompetitivebusinesstaxes,enhancingsupportforplant,machinery,andequipmentthroughcapitalallowancesandbusiness rates,andbroadeningthescopeofthepatentboxtoencompassabroaderspectrumofIntellectualPropertywouldbeinstrumentalinachievingthisgoal.

UK MANUFACTURING SECTOR POLICIES BritishManufacturing

775,014

Despiteadeclineinmanufacturingacrossgeneral UKandautomotiveindustries,knowledgeand skillsincarproductionhasbeenretainedand expandedasspecialistmanufacturersareprevalent throughouttheUK.

CarProduction2018: 449,304

CarProduction2018: 442,254

CarProduction2018: 234,138

CarProduction2018: 129,070

CarProduction2018: 160,676

CarProduction2018: 77,481 JaguarLandRover

Sunderland Nissan CastleBromwich JLR CastleSolihull JLR HamsHall BMW* Dagenham Ford* Swindon Honda Oxford Mini(BMW) Bridgend Ford* Deeside Toyota* Halewood JLR EllesmerePort Vauxhall MajorPremiumand SportsCarManufacturers 7 DesignCentres 9 BusandCoach Manufacturers 8 CommercialVehicle Manufacturers 4 Engine Manufacturers 10 MainstreamCar Manufacturers 4 R&DCentres 22 SpecialistCar Manufacturers 60+ SpecialistCar Manufacturers 2,500+

UK Car Production Plants

Mini(BMW) Honda Nissan Toyota Vauxhall Halewood | Castle Bromwich | Solihull Oxford Swindon

Sunderland Burnaston, Deeside Ellesmere

2021

(closed in 2021)

Port British Automotive at a Glance £67billion Turnover

2022

1,614,063 New Cars Registered

Cars built in 2022 130+ Countries Exported To 101,600 Commercial Vehicles Built 2022

2022

Built 2022

THE BRITISH AUTOMOTIVE INDUSTRY AutomotiveBritain Ferry

606,838 Cars Exported

1,614,063 Engines

780,000 Employment Across UK Auto

MainRoad Motorway Railway(moretracks) Railway(fewertracks) TransportKey *Engine manufacture only

Top10CarExportMarkets

ShareofUKCarExportstoEachMarket,2019

UK’s Automotive Exports

TradedependancywiththeEUisexhibitedfullyintheautomotiveindustry,withmorethanhalfofUKcar exportsbeingtotheEU.ThisalsoposesthechallengeofcompetitionwithEuropeanbrands,wherefarmore carproductionplantsexistintheEU,albeitthattheUKdoescontainmoreplantsthantheaverageEUcountry. ThisdemonstratestheUK’sstrengthofpositionwhenapproachingaregenerationofcarmanufacturingand theleverageithasovertheEUmarket.

THE EU AUTOMOTIVE INDUSTRY AutomotiveBritain

19% 55% EU US 2.2% Canada 5.3% China 1.9% Australia 3.2% Japan 1.2% South Korea 1% Russia 1.2% Ukraine 1.2% Israel 11.2% of UK manufactured cars sold domestically

UK-Made Cars Exported 900 800 700 600 500 400 300 200 100 0 2009 2013 2011 2015 2017 2010 2014 2012 2016 2018 RestofWorld EU UKCarExports(000units)2018 Japan Canada Russia L.America S.Korea US Others Asia-Pacific EU China Turkey -2% -3% -8% -10% -11% -19% -39% +42% +42% +42% +42% 2017-18Change 1.8% 1.5% 1.8% 1.8% 2.0% 2.0% 3.4% 3.4% 6.3% 17% 59% EU US China %ofTotalExports UK-EU Vehicle Trade Revenue Renault-Nissan PSA BMW Group Daimler Ford Toyota Hyundai-Kia Ceely Honda FCA Suzuki Aston Martin Ferrari McLaren Iveco McLaren Morgan Isuzu VW Group JLR 16.2bn 13.5bn 12.8bn 11.3bn 10.2bn 7.9bn 6.0bn 4.2bn 2.1bn 2.0bn 2.0bn 1.1bn 355m 325m 205m 181m 106m 45m 15m 113k EU Car Production Plants Stellantis 25 Europe Plants 2 UK Plants BMW(incl.Mini+RollsRoyce) 7 Europe Plants 3 UK Plants Volkswagen(incl.Bentley) 22 Europe Plants 1 UK Plant Ford 6 Europe Plants 1 UK Plant Renault-Nissan-Mitsubishi 12 Europe Plants 1 UK Plant Geely(incl.Volvo,Lotus+LEVC) 4 Europe Plants 2 UK Plants Paccar(incl.DAF+LeylandTrucks) 3 Europe Plants 1 UK Plant Toyota 5 Europe Plants 2 UK Plants JaguarLandRover 5 Europe Plants 4 UK Plants Honda 1 Europe Plants 0 UK Plants

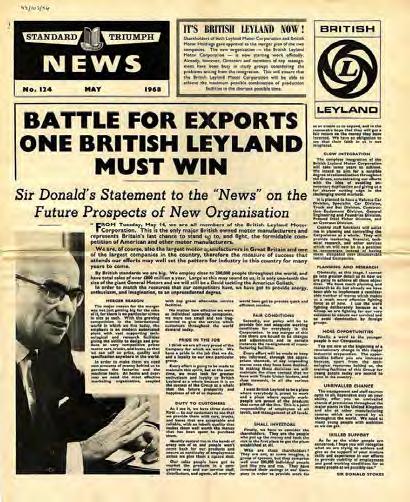

RevivingBritishLeyland

Narrative+Brief

03

TriumphvAustin vMorrisvMG

RovervJaguar

Internally CompetingMarques

Unsuitable PipelineofDesigns

Outdated Marques

National CompetitionUptake

Competitive Weaknesses

InheritedIssues

Unrealised EconomiesofScale

Internal Managment FalteringSales Damaged Reputation

International CompetitionUptake

UnabletoFollow DesignTrends

Investment Control

Approaching CriticalFailure

1968-74

Persistent UnionAction StrainedInter-Factory Relations

Manufacturing

SinglePointof FailureProduction

Confusing MarketingStrategies

InitialSuccessWithFailedLongevity

MorrisMarina+Austin AllegroModelLaunches

PlantClosures

MarquesRetired

Restructuring Nationalisation

Divestments

TheRyder Report

Waltonvs BritishLeyland

Collapse

1975-86

MarqueSales 7Divisions Reducedto4

AlthoughithadthepotentialtobringtheUKinto anewautomotiveera,speculatedtodominate theglobalmarket,thecreationofBritishLeyland wasdestinedtofailunderaseriesofinternal mismanagementissuesandexternalfactors.

ShiftingFocuson IndividualMarques

Reversingand ContradictingPolicies

Constant Rebranding

ShiftingFocuson BritishLeylandBrand

RISE + FALL OF BRITISH LEYLAND HistoricContext

Division: Austin-Morris

Class: CityCar(A)

BodyStyle: 2-doorsaloon/convertable/estate /van/coupeutility Production: 5+millioncars

UKAssembly: LongbridgePlant,Birmingham Accolades: SecondMostInfluentialCarofthe 20thCentury

Division: SpecialistDivision

Class: SportsCar

BodyStyle: 2-seatsportsconvertible/roadster Production: 314,332cars

UKAssembly: Canley,Coventry Accolades: Numerousstreetandrallyracingwins

Division: SpecialistDivision/Austin-Morris

Class: ExecutiveCar(E)

BodyStyle: 5-doorhatchback/fastback Production: 303,345cars

UKAssembly: CastleBromwich;Cowley,Oxford; Solihull Accolades: EuropeanCaroftheYear,1977

Division: Austin-Morris

Class: SportsCar

BodyStyle: Varying Production: 514,852cars

UKAssembly: LongbridgePlant,Birmingham; Abingdon

Division: Austin-Morris

Class: SmallFamilyCar

BodyStyle: 2-door/4-doorsaloon/3-doorestate Production: 642,350cars

UKAssembly: LongbridgePlant,Birmingham Accolades: Fifth-bestsellingnewcarinBritain,1979

TIMELINE OF MARQUES HistoricContext Although officially formed in 1968, British Leyland was a conglomerate created from a history of mergers, takeovers and buyouts of many car brands and marques since the start of the British automotive industry; a portfoliothatultimatelyleadtoitsdownfall. StarleyandSutton 1877 Leyland 1896 RoverGroup Rover MG LandRover BritishLeyland 1968 Standard 1903 Triumph 1923 Morris 1912 BMH 1966 BMC 1966 Nuffield Wolseley 1896 Riley 1898 Austin 1905 VandenPlas 1913 1944 1927 1938 1931 1955 1960 1952 1946 1961 1987 1984 1963 1967 Land Rover 1948 Rover 1904 MG 1923 Austin-Healey Daimler 1896 Lanchester 1896 Jaguar 1931 1984 1975 1969 1971 1987 1980 1984 Merged Discontinued Sold RoverGroup Key

ClassicMini TriumphSpitfire RoverSD1 MGMGB AustinAllegro Morris 1959-2000 Triumph 1962-1980 Rover 1976-1986 MG 1963-1980 Austin 1973-1982

BRITISH LEYLAND

1. Political Intervention

Throughgovernmentintervention,BritishLeylandisrebuilttofill themanufacturingvoidoftheUKinanattempttorevitalisethe economyofthecountryandparticularlythenorth.

5. Intelligent, Electric + Autonomous Cars

Afocusondevelopingaffordableeverymancarsthatincorporate theforefrontoftechnologies,emphasisingstustainabilityascars looktobecomewhollyelectricwithautonomouscapabilities.

2. Consolidating Marques

Former iconic marques must be consolidated under the single bannerofBritishLeyland,beingrevivedoracquiredasnecessary torebuildthestrengthandinfluenceofthebrand.

3. At Home in the Midlands

As the spiritual home of automotive manufacturing, the headquartersofBritishLeylandistoreturntothemidlandsand Birmingham,astheepicentreofamanufacturingrevival.

6. Education + Training

Ensuring that skills and education excel in design and manufacturing in the revived automotive industry through intergrationthroughoutallstagesofthesupplychain.

ExemplifyingthecompetitiveexcellenceofBritishLeylandagainst internationalcompetingbrandsthroughspecicalentertainment andpromotionnofFormulaEracing.

4. British Leyland Design Hub

Learningpaststagnationleadingtocollapse,designinnovation shall be at the centre of the new British Layland, wit hits headquartersservingasaDesignHubtoensureprosperity.

PartneringwithHS2asthegatewaytothemidlandsandthenorth fromLondonintoBirmingham,combiningtheHS2stationwith BritishLeyland’sHQtoformthesymbolicunityofthenation.

REVIVAL STRATEGIES Strategy

7. Formula E Team

8. HS2 Partnership

ROVER

The British Icon Is REBORN BRITISH LEYLAND Affordable. Electric. Iconic. Classic

BRITISH LEYLAND

Seen An Affordable Luxury Sports Car? SPITFIRE

Have Now

Never

You

Which Allegro Will You Choose?

BRITISH LEYLAND BRITISH LEYLAND BRITISH LEYLAND Allegro Allegro Allegro This One? This One???

Tested On The Track. Applied To YOUR Car.

BRITISH LEYLAND PRECISION ENGINEERING.

“LeadershipandInnovation”

Reinforcingourleadership,brandreputationandcredibilitythoughtheadoptionofthe bestinternationallyrecognisedstandardsforsustainableeventmanagementandenvironmentalexcellenceinsportingevents.

“EnvironmentalExcellence”

ImplementingUnitedNationsSustainableDevelopmentGoalswithinourenvironmental strategyandalignourcarbonemissionsontoclimatescience.

“SocialProgess”

Buildingmoreinclusive,resilientanddiversecommunitieswithinourhostcitiesthrough theimplementationofourstrategicengagementplan.

“CreatingValueThroughValues”

EnhancingourTeamsandPartnersbrandvisibilityandreputationbydevelopingbespokesustainabilitycampaignsandactivations.

FIA Sponsorship

SponsorshipwithFormulaE’srulingbody,theFIA,asanopportunitytoaccessthecompetitive spectical of racing to both demonstrate and promote British Leyland’s engineering superiority againstitsdirectEuropeancompetitorsinapublicsportssetting.

FormulaE,Established2014

10thSeasonofRacingin2023-24

17RacesAcross11VenuesperSeason

MixofTemporaryCity-CentreStreetCircuits+ TraditionalRacingCircuits

RacingSessionsTakePlaceOver1or2Days

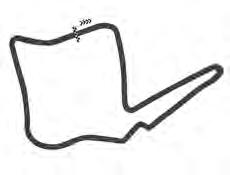

PreviousBritishCircuits:

BatterseaParkStreetCircuit

Active 2015to2016

Length 2.925km

NumberofCorners 15

Direction Anticlockwise LapRecord 1:24.150

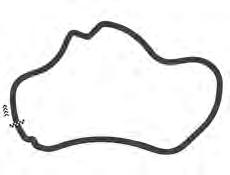

DoningtonParkCircuit

Active 1977topresent Length 4.023km

NumberofCorners 11

Direction Anticlockwise LapRecord 1:17.707

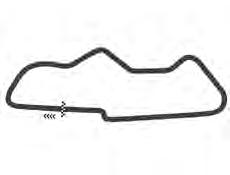

LondonExCelTrack

Active 2019topresent Length 2.090km

NumberofCorners 20

Direction Anticlockwise

LapRecord 1:21.554

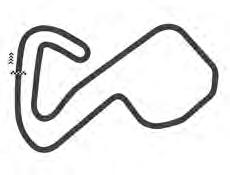

Establishment of a new Formula E circuit in the heart of Birmingham, starting at British Leyland’s DesignHub,bringingthespecticalofracingdirectlytopublicengagementtofostergreaterinterest andinvolvementintherevitalisedautomotiveindustry.

CreationofaBritishLeylandFormulaEracingteamasawayofbothdemonstratingitsengineering capabilities,whilealsoactingasavesselthroughwhichtotestandenhancenewtechnologiesand methodswhichmaythenbebroughtintotheproductionofconsumervehicles.

FORMULA E PARTNERSHIP

British

Leyland Racing Team

New

Formula E Circuit

Wins14 Podiums47 | Races 100 ABTCupra Wins3 | Podiums13 | Races 117 DSPenske Wins2 Podiums6 | Races 117 ERT Wins5 | Podiums24 | Races 116 Mahindra Wins7 Podiums24 | Races 72 McLaren Wins6 Podiums14 | Races 59 TG Porche Wins10 | Podiums32 | Races 117 Andretti Wins16 | Podiums49 | Races 117 Envision Wins12 Podiums33 | Races 96 Jaguar TCS Wins9 | Podiums25 | Races 117 MaseratiMSG Wins17 | Podiums40 | Races 117 Nissan Wins? | Podiums? Races ? BritishLeyland 12Teams,24Drivers AllElectricGen3RacingCar TopSpeed322kph Race Power 300kW 0-100km/h2.8sec Race Power 300kW MinimumWeight850kg BatteryCapacity54kWh BatteryVoltage900volts World’sfirstnet-zero carbonracecar.

Brief

Glasgow Motherwell

MaintainedDestinations

HS2Phase1

ScrappedDestinations

HS2Phase2a-Scrapped

HS2Phase2b-Scrapped

HS2East-Scrapped

PotentialHS2serviceson existingnetwork-Scrapped

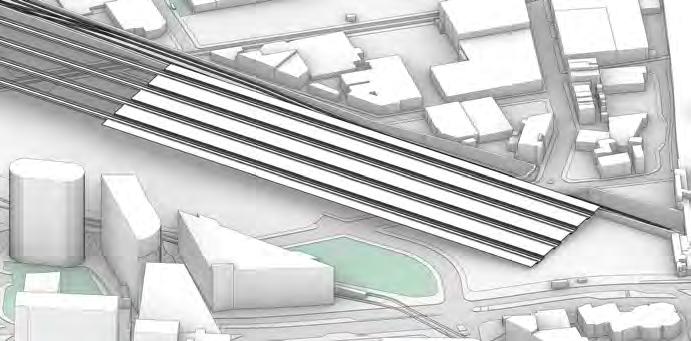

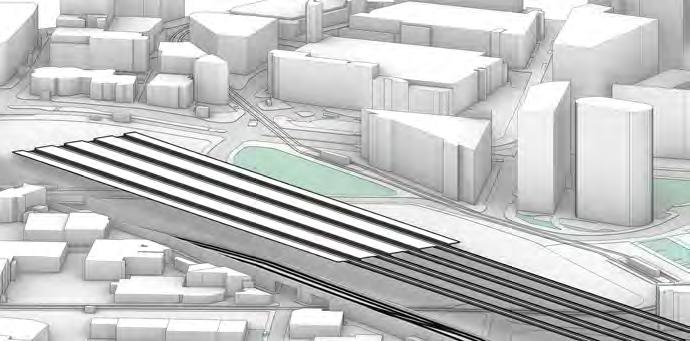

HS2 PARTNERS WITH THE NEW BRITISH LEYLAND TO DELIVER BIRMINGHAM STATION

• HS2 annouces its partnership with the newly revived British Leyland car manufacturing conglomerate

• British Leyland to integrate its new HQ with the Birmingham Curzon Street station to alleviate costs and aid future development

• Partnership hopes to restore faith to the Northern leg of HS2

Scrapped Northern Lines

UnderfinancialandpoliticalturmoilaroundHS2,thenorthernlinesbeyondHS2haverecentlybeen cancelled, effectively ending the train line at Birmingham Curzon Street. As such this London to BirminghamlinksetsthestageforthestationtobecomethedestinationgatewayofHS2.

Financial + Political Partnership

Under pressure of the cancelled northern destinations and unfulilled political promises, in the hypothtical scenario of this brief, HS2 partners with the newly revived British Leyland to provide financialaidandactasanexemplarpartnershipmodeltobereplicatedalongthescrappedroutes.

WhilefundedinpartbyBritishLeyland,theproposedBirminghamCurzonStreetstationistobe reducedinsizetoaccommodatefinancialredistributionalongtheline,reducingtheplatformsand scaleofthebuildingasappropriate.

HS2 PARTNERSHIP

Downsizing Proposed Curzon Street Station Interchange London Euston Old Oak Common Birmingham Curzon Street Edinburgh Lockerbie Carlisle Penrith

Leeds Manchester Piccadilly Derby Stoke Macclesfield Manchester Airport Sheffield Chesterfield Nottingham East Midlands Lancaster Preston Wigan Warrington Lancaster Stafford Runcorn Crewe

Oxenholme

Parkway

Key

Brief

BritishLeylandDesignHub

EmanatingTheBritishMotorIndustry

Theprojectmustexpresstheheritageandfuture oftheBritishmotorindustry,expandingonthe existingspecialismtorevitalisemanufacturing.

SustainabilityDrivenDesign+Operation

Reflectingtheneedforsustainabledesigninboth automotiveandarchitecture,theprojectistobe exemplaryasabeacontotheUK.

Efficient+EffectiveConstruction

Utilisingmasstimberprefabricationandmodular systems,constructionefficiencycanbeenhanced todelivertheprojectatashortertimescale.

SnowHillStation

Project Objectives

DesignHub+HS2Station

ContributingtoLocalCulturalIdentity

Birminghamhasahertitageofmanufacturingthat willbeemboldenedandcelebratedthroughthe project,whilstrefelctingthecontemporaryculture.

LocalCommercial+EconomicGrowth

InpartneringHS2withBritishLeylandtocreatea gatewayintoBirmingham,thiswillincreaseinterest andinvestmentintotheareatostimultaegrowth.

CommunityDrivenCollaboration

Closecommunitytieswithlocaluniversities, businessesandresidentswilldrivecollaborative initiativestostrengthenthesharedcommunity.

PublicParks+TestTrack

NewStreetStation

MoorStreetStation

Birmingham City Centre

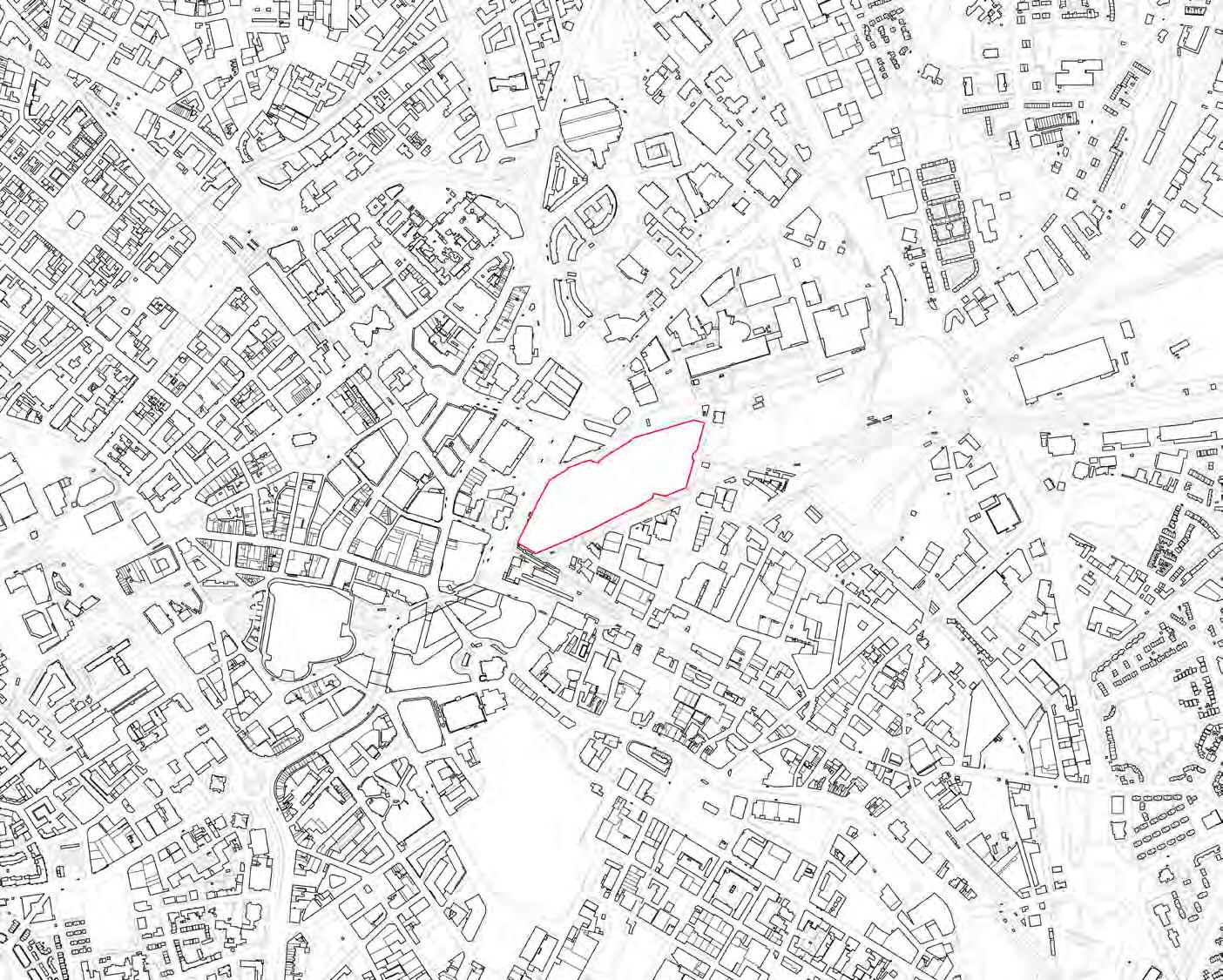

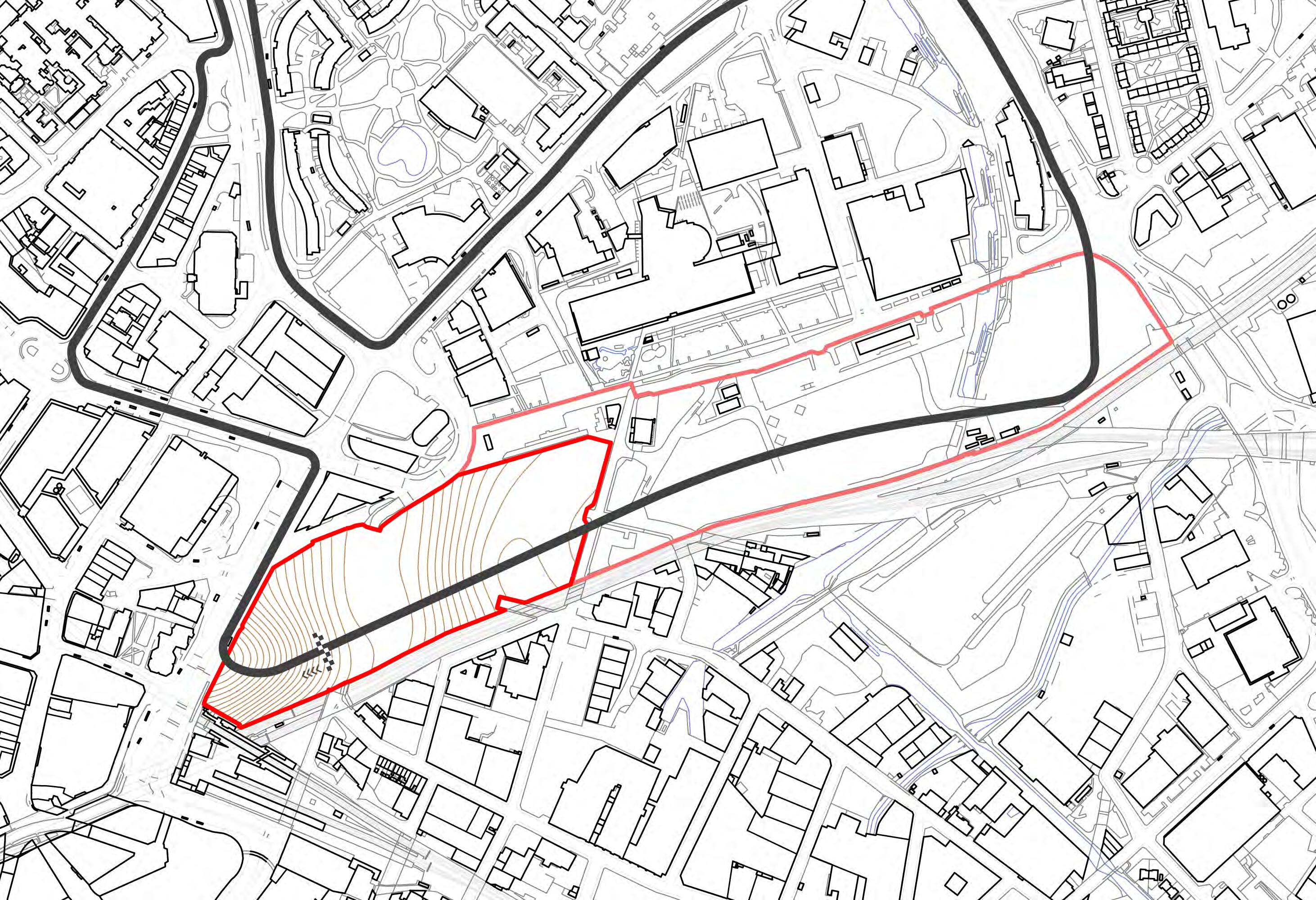

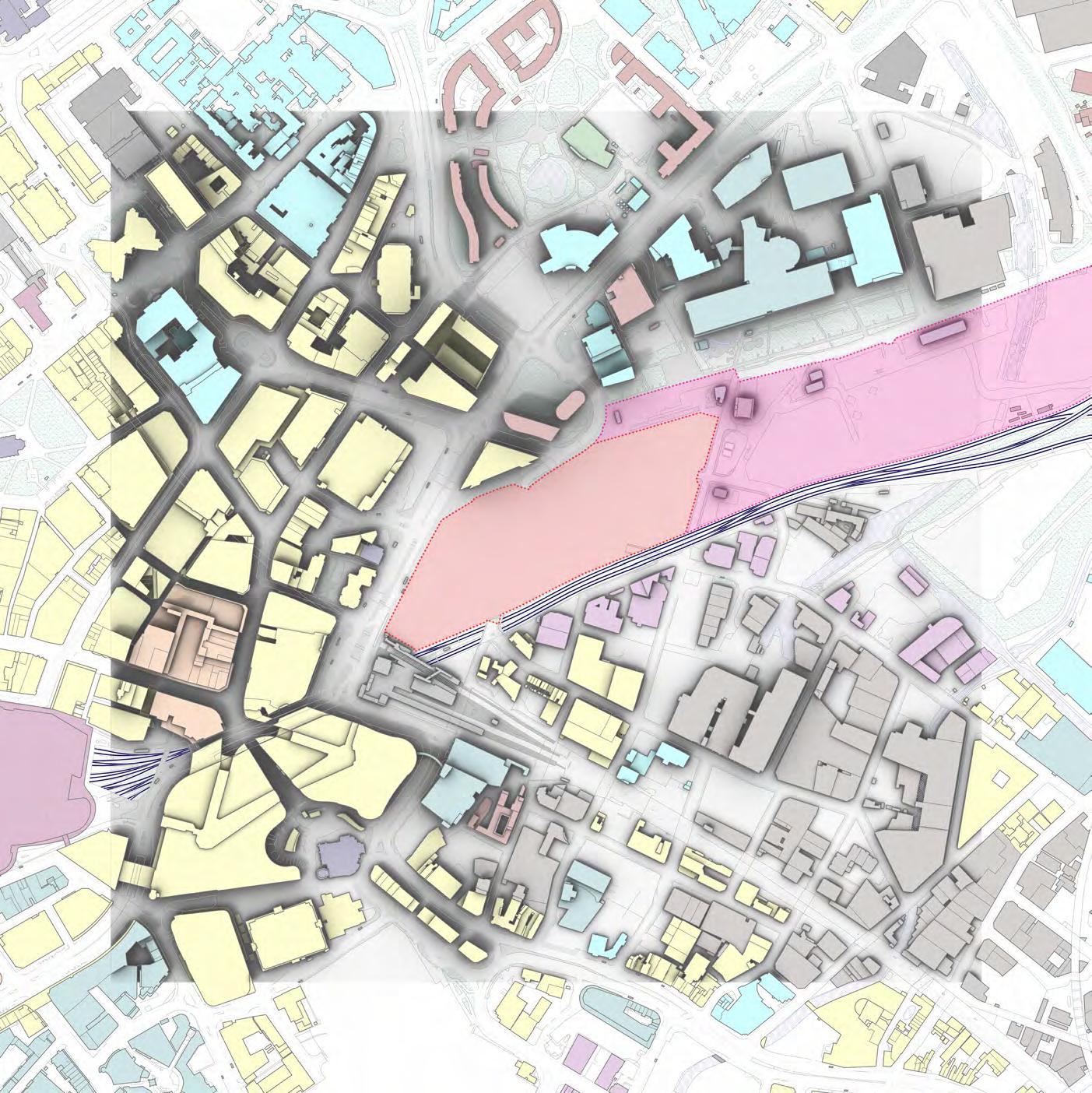

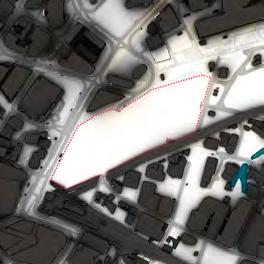

The site is to be located at the HS2 Birmingham Curzon Street station site, set in BirminghamCitycentreandincloseproximitytofurthertransportlinksaswellasadense generalpopulationalongsidevarioushighereducationfacililties.

AutomotiveIndustry

AstheheadquartersofthenewBritishLeyland, theproject’ssuccesswillbeakeysignifierand symbolicrepresentationofBritishautomotives.

ManufacturingIndustry

Intheambitionofrevitalisingmanufacturingin theUKandnorth,theprojectshallestablishdirect connectionstogrowtheregions’industries.

InternationalMotorsports

TheFormulaEpartnershipandspecticalwillbring additionalattentiontoBritishmotorsportsonthe internationalstageandbringgreatercompetition.

Key External Stakeholders

LocalResidents

Inadenseurbanpopulation,theprojectmustbe consideratetolocalresidents,incorporatingpublic interfaceelementsforsuccessfulcohabitation.

LocalBusinesses

Retailspacesfromthestationinterfacewillbring aboutopportunityforlocalbusinesses’expansion andaswellasincreasingtourismandcustomers.

LocalAcademicCommunity

ClosetieswithBirmingham’suniversitieswill enablenewopportunitiesandfacilitieswhile enablingdirectindustryinteraction.

SITE CONTEXT Brief

FIA

FormulaE Sponsorship

Client Partnerships

UK Government

Planning+Approval,Legislation,Funding, Oversight+Accountability,PublicConsultation

British Leyland ProjectClient

Project Delivery Team

Architects+ Consultants

Architect

Quantity Surveyor

Project Manager

HS2 Sponsorship+ OperationsPartner

Engineers+ Consultants

Structural Engineer

Timber Engineer

Interior Architect Civil Engineer

Landscape Architect

Transport Consultant

Hertitage Consultant Environmental Engineer

Automation Engieer

Construction Manager

Procurement Supply Chain

Tier 1

MainContractor JointVenture

Tier 2

Subcontractor/Supplier

Construction +Contractors

e.g.GroundworksCompany

Tier 3

Subcontractor/Supplier

e.g.PPEProvider,PlantHire

Tier 4 + 5

Subcontractor/Supplier

e.g.CateringCompany

Fire Engineer

Systems Engineer

MEP Engieer

Brief

CLIENT + PROJECT TEAM HIERARCHY

EU UK

04

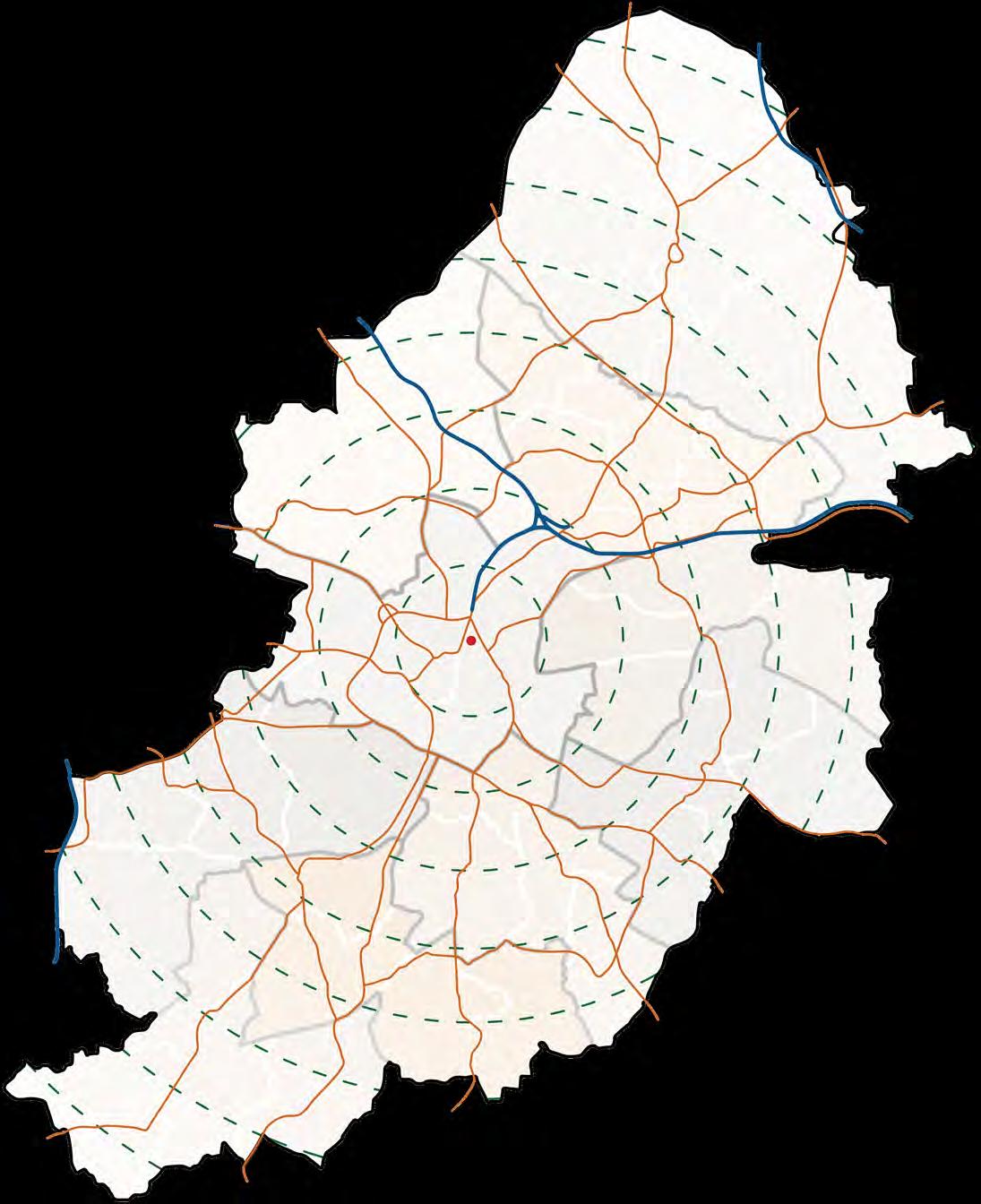

SiteContext+Masterplan GatewaytoBirmingham

ofallemploymentinBritish automotiveisintheMidlands 39%

autosectorjobsinthe EastMidlands 2,000 autosectorjobs acrosstheMidlands 80,000 oftheUKautomotive R&DisintheMidlands 60%

UK-builtcarsare manufacturedinDerby 1in11

worldleadingautomotivesuppliers havebasesintheMidlands 16oftop20

ThetwolargestBritishLeyland carproductionplants:

LongbridgePlant Birmingham, West Midlands

Built: 1895

Owners: AustinMotorCompany,1906-52

BritishMotorCorporation,1952-68 BritishLeyland,1968-86 RoverGroup,1986-2000 MGRoverGroup,2000-05 SAIC,2005-present Marques: MG,Rover,Mini,Austin

SolihullPlant Solihull, West Midlands

Built: 1936 Owners: BritishGovernment,1936-45 RoverCompany,1945-68

BritishLeyland,1968-86 RoverGroup,1986-2000 Ford,2000-09 JaguarLandRover,2009-present Marques: LandRover,RangeRover,Jaguar

DespiteholdingaroundhalfoftheUK’scarproduction,sincethecollapseofBritishLeyland,theWestmidlandshave followedaplateauinganddecliningtrendthathasbeenexacerbatedbythelossofMarquessuchasRoverGroup.

MIDLANDS MOTOR INDUSTRY + BRITISH LEYLAND

CurrentMidlandsMotorIndustry UK WestMidlands AutomotiveProduction,1970-2008 2.5million 2million 1.5million 0.5million 0 1million 1972 1988 1980 1996 1976 1992 1984 2000 2004 2008 Peugeot Rover LandRover Jaguar AutomotiveProductioninWestMidlandsFirms,1970-2008 1million 0.8million 0.6million 0.2million 0 0.4million 1972 1988 1980 1996 1976 1992 1984 2000 2004 2008 West Midlands Car Production SiteContext

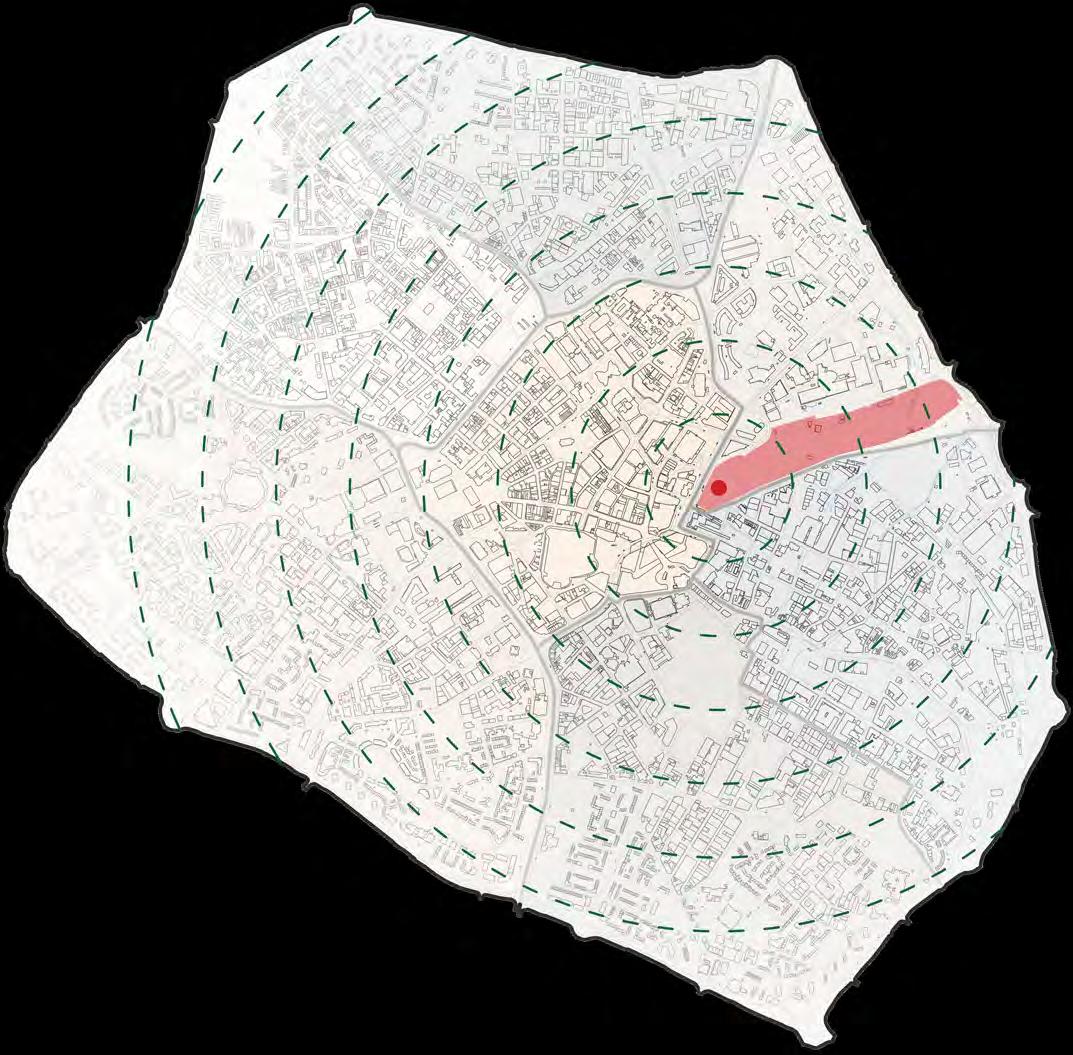

Birminghamisdividedintodistinctregions varyinginpopulationdensity,manufacturing hertitageandexistingresourcesandfacilities.

Intheinterestofexpandingmanufacturinginto BirminghamandtheMidlands,fromtheepicentre ofBirmingham’scitycentre,supportingsupply networkforBritishLeylandcanbeestablishedto utiliseregionalspecialities.

Sutton Coldfield 96,700

CustomerServices

AutomotiveComponents Metalwork+Engineering

Perry Barr 112,400

CustomerServices

AutomotiveComponents Education+Training

Ladywood 126,700

FullAutomotiveProduction AutomotiveDesign

SupplyChain+Logistics

Edgbaston 74,000

FullAutomotiveProduction

SupplyChain+Logistics AutomotiveComponents

SUTTONFOUROAKS SUTTONVESEY OSCOTT

PERRY

Erdington 103,200

AutomotiveComponents

MotorcycleManufacturing CustomerServices

SUTTONTRINITY

SUTTONNEWHALL

SHELDON SOHO

BARTLEYGREEN NECHELLS HODGEHILL SHARDEND WASHWOOD HEATH BORDESLEY GREEN

EDGBASTON HARBORNE WEOLEY

NORTHFIELD KINGS NORTON QUINTON

LONGBRIDGE

SELLYOAK

SPRINGFIELD SPARKBROOK

MOSELEYAND KINGSHEATH

SOUTHYARDLEY HALLGREEN

BOURNVILLE BRANDWOOD BILLESLEY

Northfield 103,700

CustomerServices

SupplyChain+Logistics Research+Development

STECHFORDAND YARDLEYNORTH ACOCKS GREEN

Hodge Hill 129,300

AutomotiveComponents

Metalwork+Engineering Research+Development

Yardley 113,000

FullAutomotiveProduction AutomotiveComponents Research+Development

Hall Green 115,900

Selly Oak 108,000

Education+Training Research+Development CustomerServices

AutomotiveComponents

MotorcycleManufacturing Metalwork+Engineering

SiteContext REGIONAL

FACILITIES

RESOURCES +

BARR HANDSWORTH WOOD LOZELLSAND EASTHANDSWORTH KINGSTANDING ERDINGTON TYBURN STOCKLAND GREEN

ASTON

LADYWOOD

Automotive Components Customer Services Education +Training Research+ Development SupplyChain +Logistics Metalwork+ Engineering Motorcycle Manufacturing FullAutomotive Production Key

Manufacturing Output Community Development Skills+ Training

Income+ Wealth CulturalHeritage Restoration SocialInclusion +Equality Environmental Sustainabililty Infrastructure Development Employment Opportunities

Jewellery Quarter St. George + St. Chad

Metalwork+Engineering

Manufacturing+Engineering Creative+Design FinancialServices Retail+Commercial PublicServices+Administration

City Core

Retail+Commercial

Education+Research BusinessServices EngineeringTechnology FinancialServices Creative+Design

Westside + Ladywood

Residential

Southside + Highgate

Manufacturing+Engineering

Eastside

Cultural+Entertainment SupplyChain+Logistics SupplyChain+Logistics Hospitality+Leisure PublicServices+Administration Cultural+Entertainment

Manufacturing+Engineering

LOCAL RESOURCES + FACILITIES SiteContext

BirminghamCity University AstonUniversity UniversityCollege Birmingham Bullring BirminghamArena MailboxBirmingham SciencePark

Digbeth

Automotive Components Customer Services Education +Training Research+ Development SupplyChain +Logistics Metalwork+ Engineering Sales+ Publicity FullAutomotive Production Key Existing Proposed

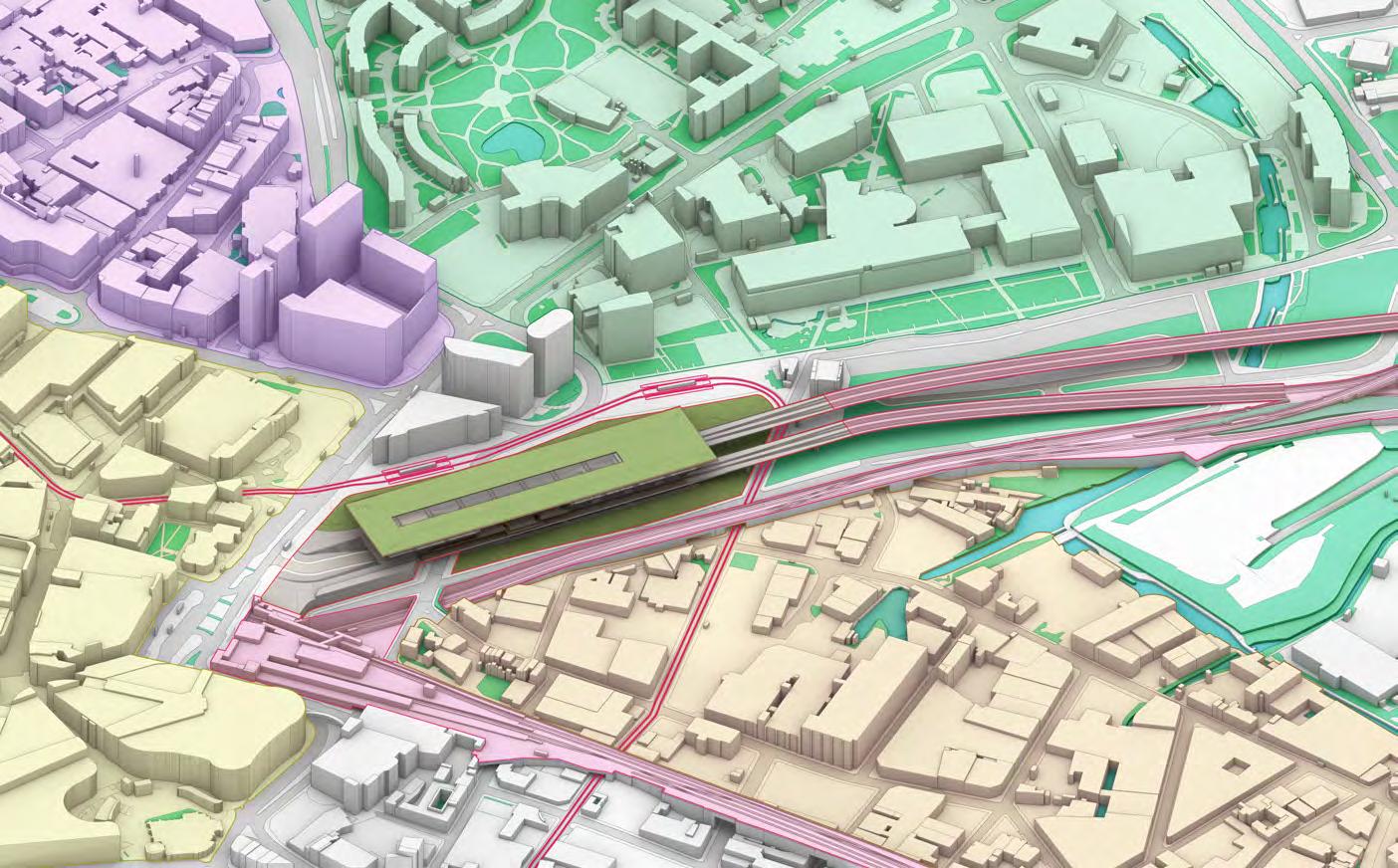

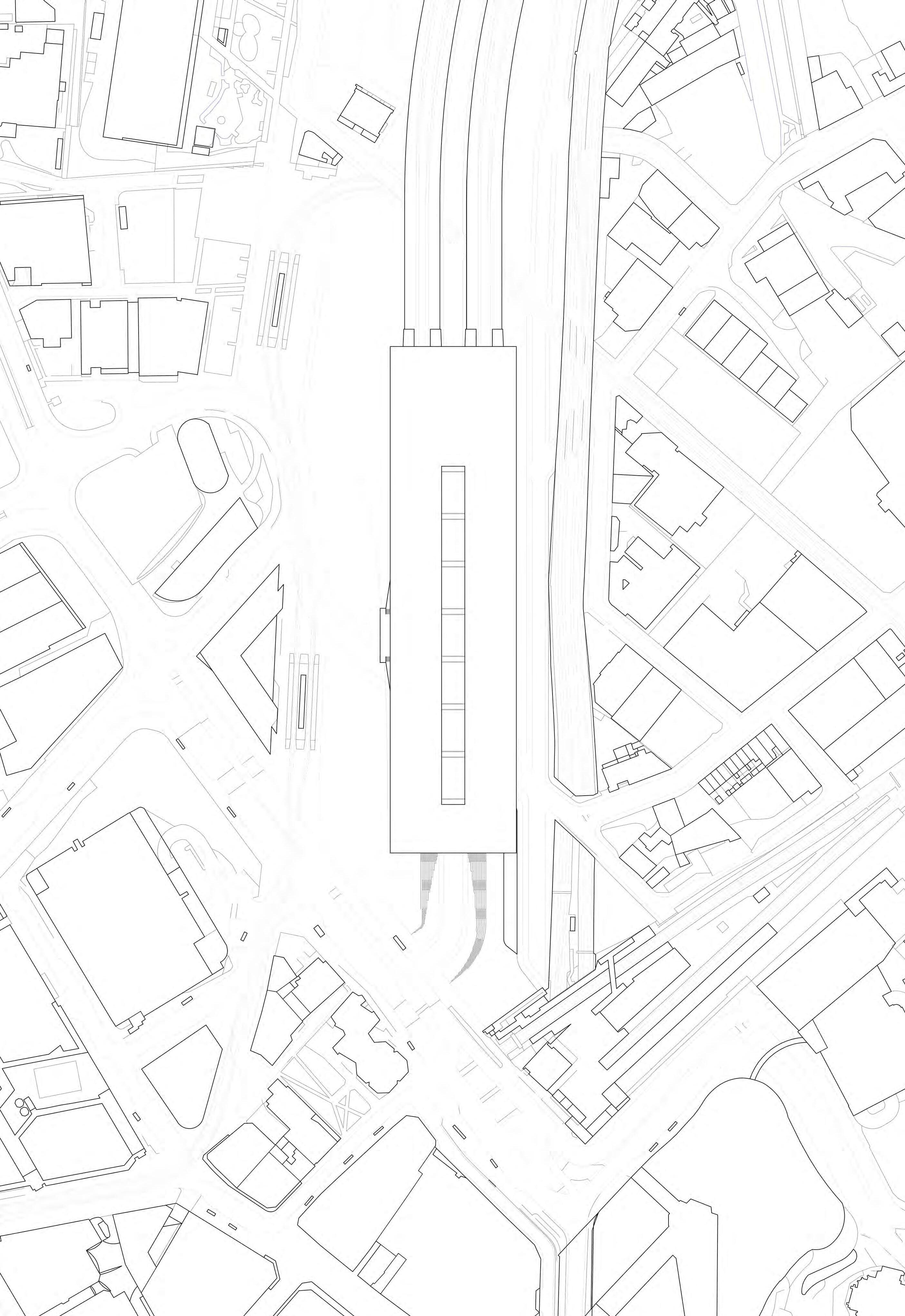

AstheUK’ssecondlargestcityandonesteepedinindustrialheritage,Birminghamhasthe desireforbothgrowthandretentionofitshertitage.TheHS2hubbeinglocatedinthecity centremarksitasakeylandmarkarrivalpointintothecity.

N 1:10,000 0 50m 100m 200m BIRMINGHAM CITY CENTRE SiteContext Cloudy, Sunny + Precipitation Days 30days 25days 20days 15days 10days 5days 0days Mar Jul Jun Oct Dec Feb May Sep Nov Jan Apr Aug Sunny Precipitation Days Partly Cloudy Overcast Precipitation Amounts 30days 25days 20days 15days 10days 5days 0days Mar Jul Jun Oct Dec Feb May Sep Nov Jan Apr Aug 20-50 <2mm 10-20 Dry days 5-10 2-5 Snow days Wind Rose N 1000 750 500 250 0 W E S >24 >31 >38 mph >0 >3 >7 >12 >17 Average Temperatures + Precipitation Mar Jul Jun Oct Dec Feb May Sep Nov Jan -10 0 10o 20 30 100mm 75mm 50mm 25mm 0mm Apr Aug Mean daily max Mean daily min Precipitation Hot days Cold nights Maximum Temperatures Mar Jul Jun Oct Dec Feb May Sep Nov Jan 30days 25days 20days 15days 10days 5days 0days Apr Aug Frost days >25 >0 >20 <0 o C >15 >10 >5 Science Park Aston University Learning+ Research Colmore Business District Paradise Circus Retail Core Snowhill Birmingham Smithfield New Street Station Key DesignHubboundary Conservationarea Enterprisezone Projectarea Canal RiverRea Characterareas /Keylocations Railline Metroline Metroextension

Local Plan + HS2 Creative

1. Knockhill

Length: 2.04km Turns: 8 Opened: 1974

5. SilverstoneNational

Length: 2.64km Turns: 6 Opened: 1948

2. Croft

Length: 3.42km Turns: 16 Opened: 1964(1995)

6. Snetterton

Length: 4.78km Turns: 12 Opened: 1941

3. OultonPark

Length: 3.59km Turns: 12 Opened: 1953

7. Thruxton

Length: 3.80km Turns: 11 Opened: 1950

4. DonningtonParkGP

Length: 3.19km Turns: 8 Opened: 1931(1977)

Length: 3.91km Turns: 11 Opened: 1950 8. BrandsHatchGP

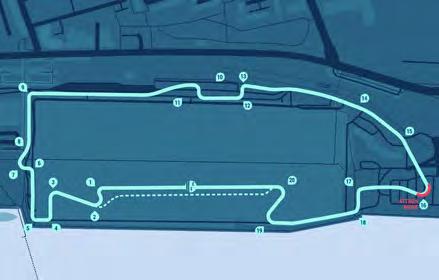

Iconic British Track Circuits

The Birmingham Leyland Circuit Aston University Business Core Birmingham City University

Length: 3.61km Turns: 15

Intended as both a test track for prototype British Leyland vehicles and as a race track for Touring Car competition,thiscircuitwouldactasaspecticalfeatureofthesitetoshowcasetheachievementsofBritish Leylandindirectcompetitionwithitsrivals.

1. 2. 3. 4. 5. 6. 8. 7.

Retail

PrimarySite SecondarySite

Core

N 1:5,000 0 25m 50m 100m

RailwayStation RailwayStation Education HistoricLandmark Education RailwayStation BirminghamNewStreet BirminghamSnowHill BirminghamMoorStreet AstonUniversity CurzonStreetStation BirminghamCityUniversity NationalCoachStation DigbethCoachStation LiveMusicVenue O2Institute ScienceMuseum ThinktankBirmingham Church St.Martin’sSquare Retail Bullring&GrandCentral Retail Selfridges CITYCENTRE JENNENSROAD JAMES WATT QUEENSWAY DIGBETH MOORSTREET QUEENSWAY B4100 DesignHubBoundary CarPlantBoundary SiteArea SiteArea Residential Commercial/Retail Industrial Recreation/Lesiure/Sport IndoorEntertainment/Leisure/Sport Public/Social/Educational/Medical Residential+Commercial Industrial+Commercial Other Religious Transport Transport+Industrial/Commercial RailwayLines Key N 1:5,000 0 20m 50m 100m LOCAL LAND USES + LANDMARKS SiteContext

SOLAR STUDIES SiteAnalysis Average Daylight Times Sunlight hours Monthly Average Jan 8hrs 6hrs 4hrs Feb Mar Apr May Jun Jul Aug Sep Nov Oct Dec Average Daily Hours of Sun Dawn Dusk Sunlight 12 18 24 06 00 Jan Mar Apr May Jun Jul Aug Sep Oct Nov Dec Feb Sun Path N 10o 30o 50o 70o S E W Summer Solstice Annual variation Sun rise range Sun set range Winter Solstice Equinox SummerSolstice 0600 20/06/2024 SummerSolstice 0900 20/06/2024 SummerSolstice 1200 20/06/2024 SummerSolstice 1500 20/06/2024 SummerSolstice 1800 20/06/2024 MarchEquinox MarchEquinox MarchEquinox MarchEquinox MarchEquinox 0600 20/03/2024 20/03/2024 20/03/2024 20/03/2024 20/03/2024 0900 1200 1500 1800 WinterSolstice 0600 22/12/2024 WinterSolstice 22/12/2024 0900 WinterSolstice 22/12/2024 1200 WinterSolstice 22/12/2024 1500 WinterSolstice 22/12/2024 1800 N

SiteForm+Size

0.46km2

TERRAIN + SITE INTERFACES

SiteAnalysis

N

SlopingTerrain

0.0m

Spotheights

Gradientdirection

0.5mcontourlines

Alignments+Interfaces

Publicfacingboundaryalignment

Privatefacingboundaryalignment

Public-privateinterfaces

Accesspoints

KeyBuildings+Approaches

Primaryapproaches

Keybuildings

Railwaylinestructures

Site

452.2m 140m -5.5 m 0.0m +10.2m PRIVATE PRIVATE PRIVATE PUBLIC PUBLIC PUBLIC PUBLIC N

SafetyGap10m

TrainWidth200m | TwoCoupledUnitsOption400m

TrainHeight3300mm

TrainWidth3180mm

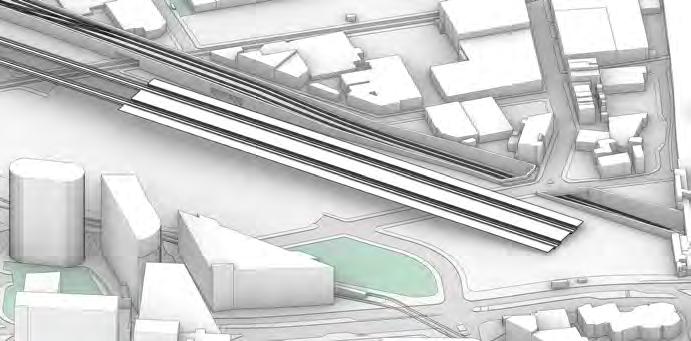

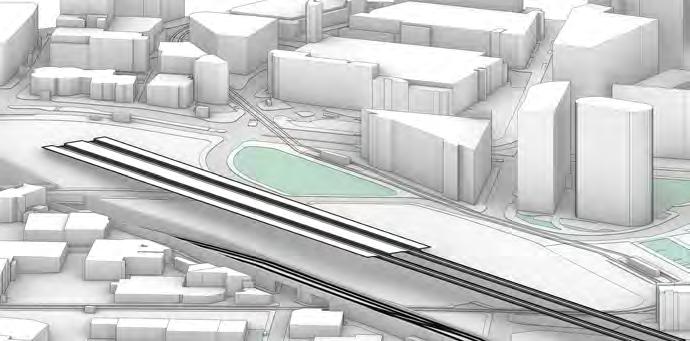

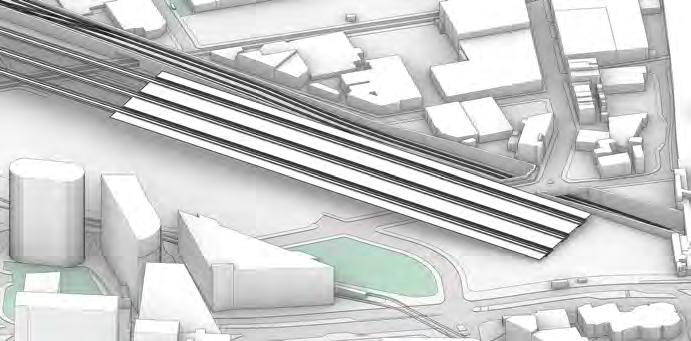

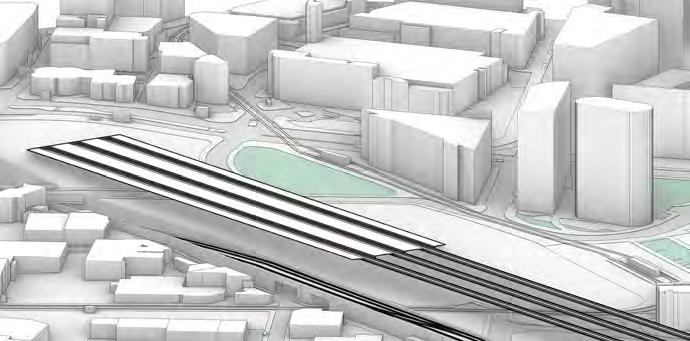

DoublePlatformWidth10m

PlatformGapWidth7m

SinglePlatformWidth6m

RailstoPlatform915mm

TrackWidth1472mm

Min.PlatformLength200m

CarriageLength16.5m

Dimension Constraints

Four Platforms

Six Platforms

Eight Platforms

PLATFORM FEASIBILITY Massing

Key

Siteboundary

Sitegradient

Steepbankslope

Previousroad

Visualbarrier

Listedbuilding

Keyresidentialfacade

Publictransportcorridor

Keyaccessroutes

Publicgreenspace

Significantbuilding

ExistingRoadEntry ExistingFootEntry Overlooking

Keyviewpoint

OPPORTUNITIES + CONSTRAINTS

SiteAnalysis

N 1:2,000

10m 25m 25m

0

Sunpath

Noisesource

BIRMINGHAM LEYLAND PARK MASTERPLAN Masterplan N 1:2,000 0 10m 25m 25m Key Siteboundaries Proposals Station+raillines FormulaEspectating Privateservicesroute Pedestrianconnection ListedBuilding Landmarkbuilding Vehicleaccess Canal Existingrailline Proposedrailline Potentialsupportfacilities TEST TRACK / PUBLIC SPACE FORMULA E SEATING DESIGN HUB (ABOVE) HS2 STATION (ABOVE) CAR SALES CENTRE FORMULA E WORKSHOP PUBLIC PARK VIADUCT PARK PUBLIC SQUARE PUBLIC PARK SALES/ DISTRIBUTION CAR PARK

Massing,Programme+StructureStudies Form+StructureGenesis

05

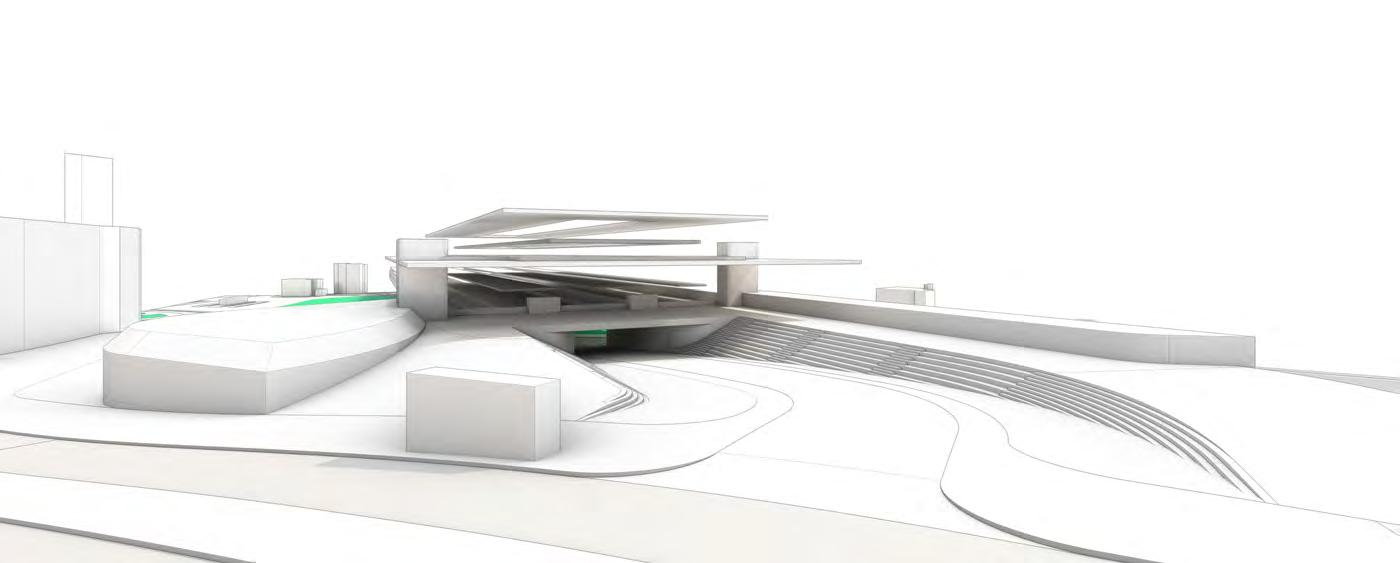

AsthegatewayintoBirmingham,theproposal issettomergeintotheurbanlandscapeofthe cityasaninhabitableurbanfabricthatbuildsthe approachtothestationanddesignhub.

MERGING URBAN LANDSCAPE Massing

Park / Formula E

HS2 Urban Interface

British Leyland

INITIAL STRUCURE STUDY Structure

SKELETAL VIADUCT FRAGMENT Structure

SKELETAL UNDERBELLY STUDY Structure

1. Viaduct + Formula E

Settingoutkeypillarsofthestationviaductandblending of the site approach into the landscape. Divided by the Formula E track running through the landscape with seatingcarvedoutintothegradient.

2. HS2 Station

MergingtheHS2stationintothepublicrealmasanonenclosed public interface to eminate transparency and accessibilityoftheLondon-Birminghamgateway,withthe stationconcoursepublicallyaccessible.

3. Mezzanine Entrance

The entrance to British Leyland’s design hub being integrated into the concourse at a different level, also blended into the public station interface as an elevated leveloftheconsoursewithgrandstaircaseapproaches.

4.DesignHub

The semi-private level of British Leyland, acting as a hub of car design, prototyping and exhibition, as well as incorporating Formula E spectating through a street facingstandtoprovideanelevatedraceddayexperience.

5.InhabitedRoof

The world of British Leyland set above that of HS2, as the creative mind of the building watching over the development of Birmingham. With atrium spaces connectingtothelevelsbelowforpublictransparancy.

6. Shared Shelter

Sheltering the activities of British Leyland, HS2 and FormulaEunderasingleroofstructureasasybolicshared unity of the triad, creating a sense of shared place and destinationwhenarrivingatthegatewaysite.

SITE MASSING STRATEGIES Form

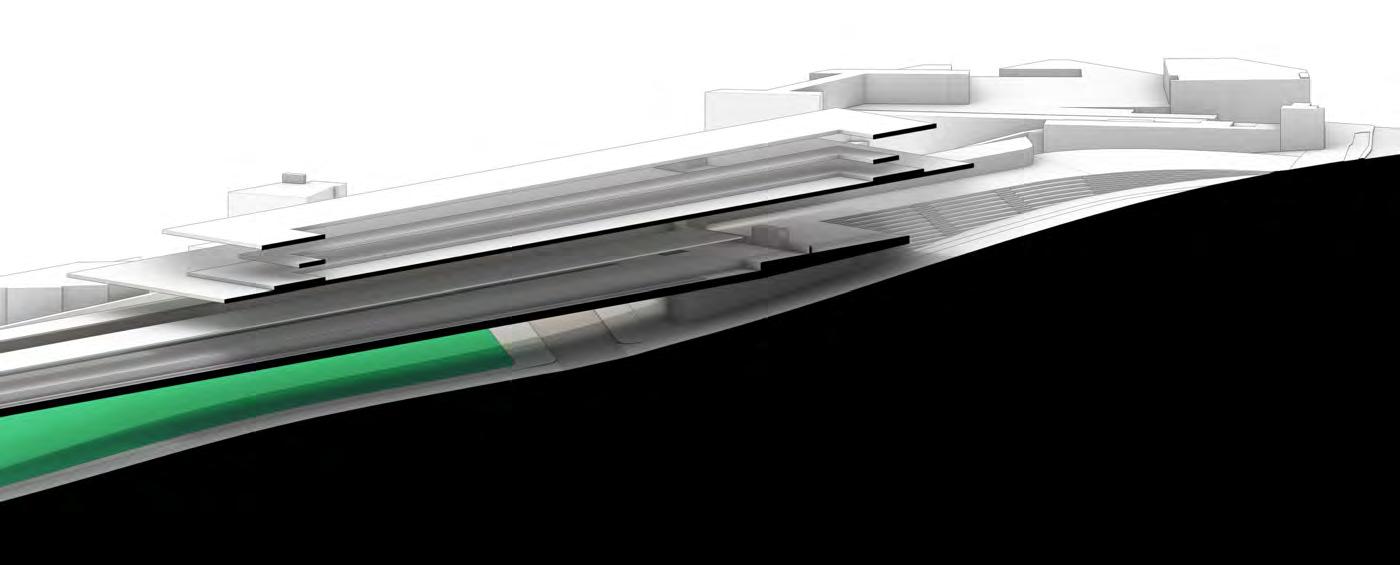

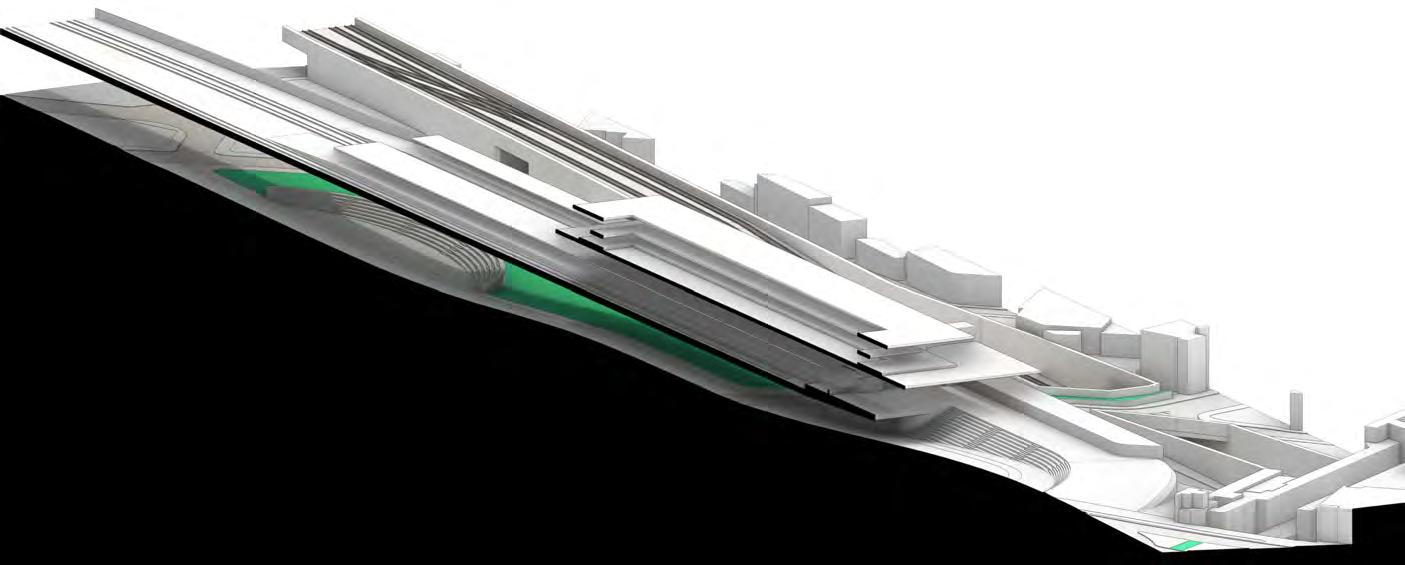

1.SiteLevelMassing

Respondingtotheslopinggradientoftheterraintodetermineprogrammemovementandsettwobase leveldatums:thefirstatstreetlevelandthesecondatalowerroadlevel.

FormingpublicurbanpromenadesatthestreetlevelleadingintotheHS2platforms,andintheviaductspace underthestation,untilisedfortheFormulaEcourse.Elevatedtoenablethefreeflowofpeoplethroughout.

3.InhabitedRoof

ElevatingandinhabitingtheroofspacetobecomethedesignhubofBritishLeyland,actingasanenclosed spaceperchedabovetheunenclosedstationbelow.

4.Visual+CirculationInterfaces

Horizontalandverticalcirculationprovidedintotheinhabitedroof,withvisualinterfaceswiththelandscape andstationbelow,particularlylinkingwithspectationofFormulaEevents.

5.CantileveredCanopy

Expansionoftheinhabitedrooftoformasinglecanopytoshelterallinhabitantsofthesitewhilstenabling unenclosedspaces.Alsointroducingatriumspacesforvisualtransparencythroughthebuilding.

DESIGN GENESIS Form

2. Elevated Urban Promenade

INHABITED ROOF FORM Form

TECTONIC FORM Structure

BirminghamIndustrialPrecedents

SolihullPlant

LongbridgePlant

LucasIndustries,GreatKingStreet

JaguarLandRover,CastleBromwich

Fisher&LudlowWorks

Structural Strategy

Transferofdeadloadsthroughprimarystructure

Deadloadsincurredfromground

Naturalwind/snow/rainloads

Liveloads

TECTONIC FRAGMENT STUDY

Structure

Utilising and expanding the existing network of manufacturing facilitiesadjacenttositetosupport small component and powertrain production,thentransportedtosite forcustomcarassembly.

Close relationship with local universities and educational facilities to enable growth of car manufacturinganddesignindustry, with facilities made avilable within theDesignHubfortraining.

Use of local office space and businesssupportfacilitiestoenable the service side of British Leyland, maintaining a close connection to the Design Hub to form an interconnectedcampus.

Locating sales and experience stores within Birminghams famous Bullringshoppingcentreasawayof spreadingBritishLeyland’sinfluence andimagetolocalinhabitantsand visitingtourists.

Maintaining a close connection to the regional rail interchange of BirminghamMoorStreetandSnow Hill stations as an transit facility of bothpeopleandgoods.

SITE ADJACENCIES Programme EDUCATIONAL CORE RAILWAY INTERCHANGE BUSINESS CORE RETAIL CORE MANUFACTURING CORE CityCentreConnections ManufacturingCore Educational Core Business Core Retail Core RailwayInterchange

TicketOffice Courtyard

/ gniniD ImpulseRet

/ gniniD mI p u lse Retail / Dining

teRnoitanitseDia l / Dining

PromenadeApproach

InteriorCicrulation

HS2Station

VisualFormulaEConnection

FormulaESpectating

StudentDesignCentre

SharedWorkshops+Exhbition

BritishLeylanDesignHub

Barriers

Design Studios

dentExhibition

PROGRAMME ADJACENCIES Programme

P u b l ci

ai

WaitingArea s

gnitaeS ImpulseRet

l

ai l

T c ketBarriers

noitanitseD iD/liateRin n g

s pac e W ro pohsk

Ticket

Refreshment Hub R eception itanitseDno R e tail/Dining

StudentWork

S t u

C u s

ClayM o d e l l gni

tnevE hT e a t r e

P r o m

Atrium HS2Platforms

snoitibihxE Spectator S t a n sd WCs WCs WCs WC s

tomerDesign M e e t ing Rooms 3DPrinting

Design Studios

alumroF egnuoLE

enade Concourse

FormulaECircuit Track

VerticalCirculation Exhibition

PublicCarCustomisation

FormulaESpectating

EventTheatre

StudentDesignCentre BritishLeylanDesignHub

4.InhabitedRoof

Within the enclosed roof are the student design interface with adjoiningeventtheatre,andBritish Leylanddesignhub,whileexhibition spacespermiatethroughtheatrium.

3.FormulaE+Prototyping

From the cantilevered platforms the building divides in two, Formula E interfaces in the street facing half and continuation of car customisationintherearhalf.

2.PublicInterface

From the atrium lobby, circulation splitstoboththeheritageexhibition and public car customisation interfaces across the atrium and externalcantileveredplatforms.

1. Station Entrance

Urban interface approaches from upper and lower levels, leading to theHS2stationlevelfromwhichthe buildingisaccessed.

SPATIAL ORGANISATION

Programme

+ CIRCULATION

Form+StructureRefinement DesignDevelopment

06

CANTILEVERED TERRACES FragmentStudies

SideApproachView FrontElevation SideElevation

TerracesFragment

ATRIUM CORRIDOR FragmentStudies ViewFromEntranceLobby ViewOntoEntranceLobby

AtriumFragment

IntersectingUrbanInterfaces

APPROACHES + URBAN INTERFACE FragmentStudies

UrbanInterfacesFragment

StreetApprochPromenade

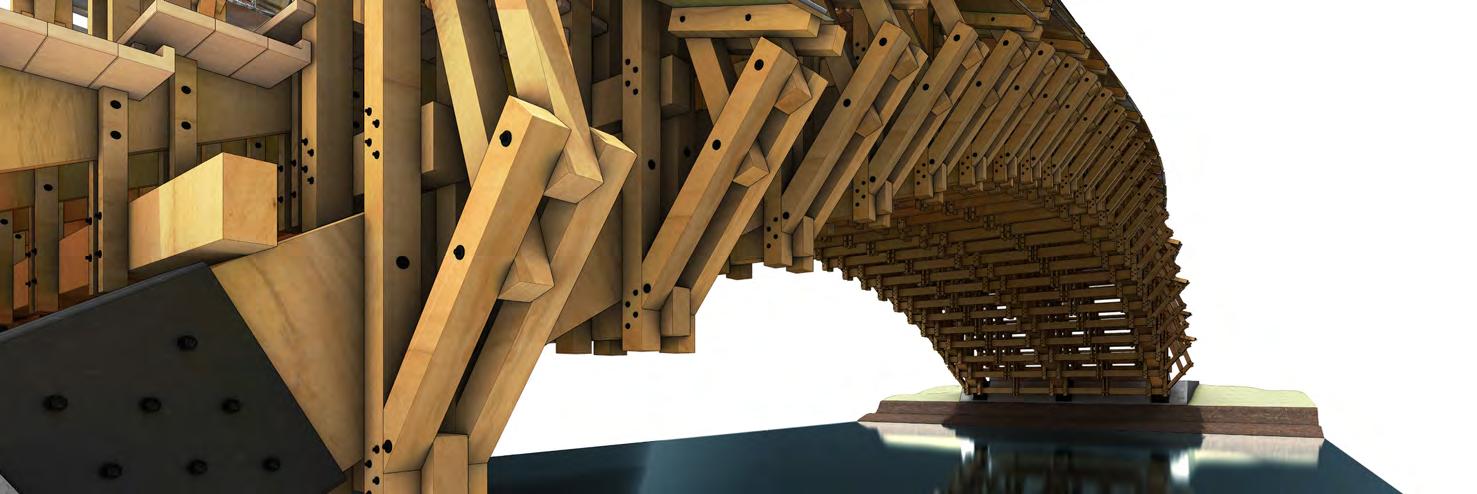

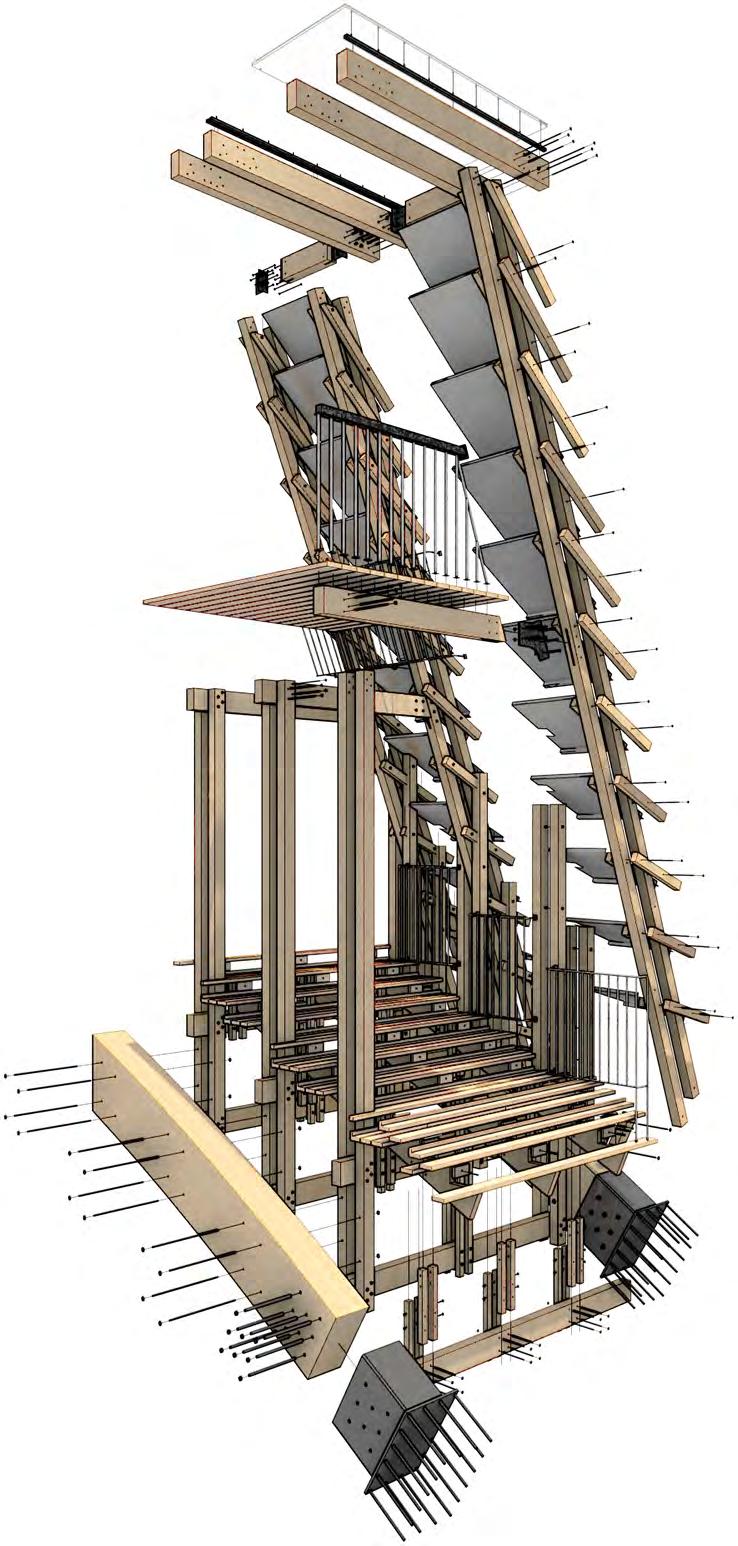

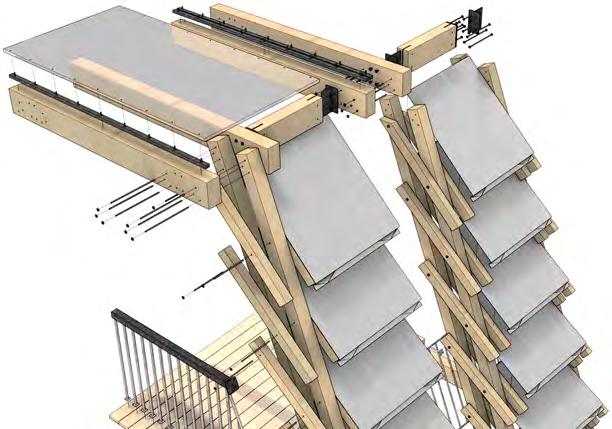

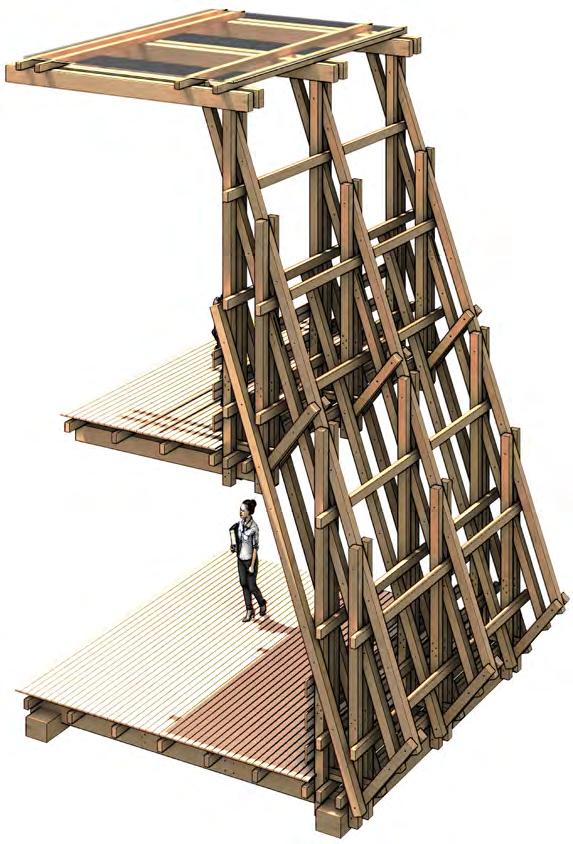

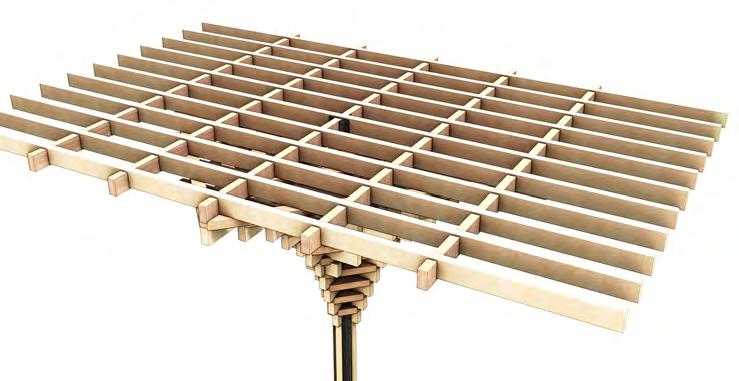

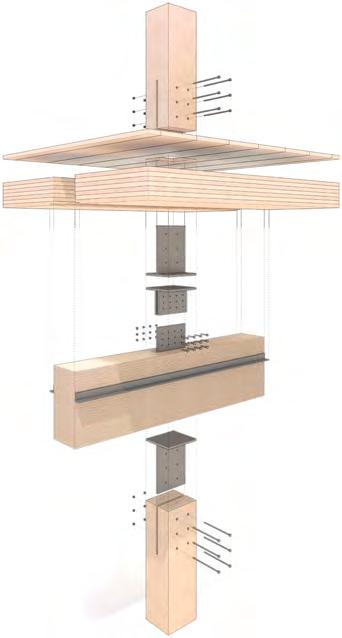

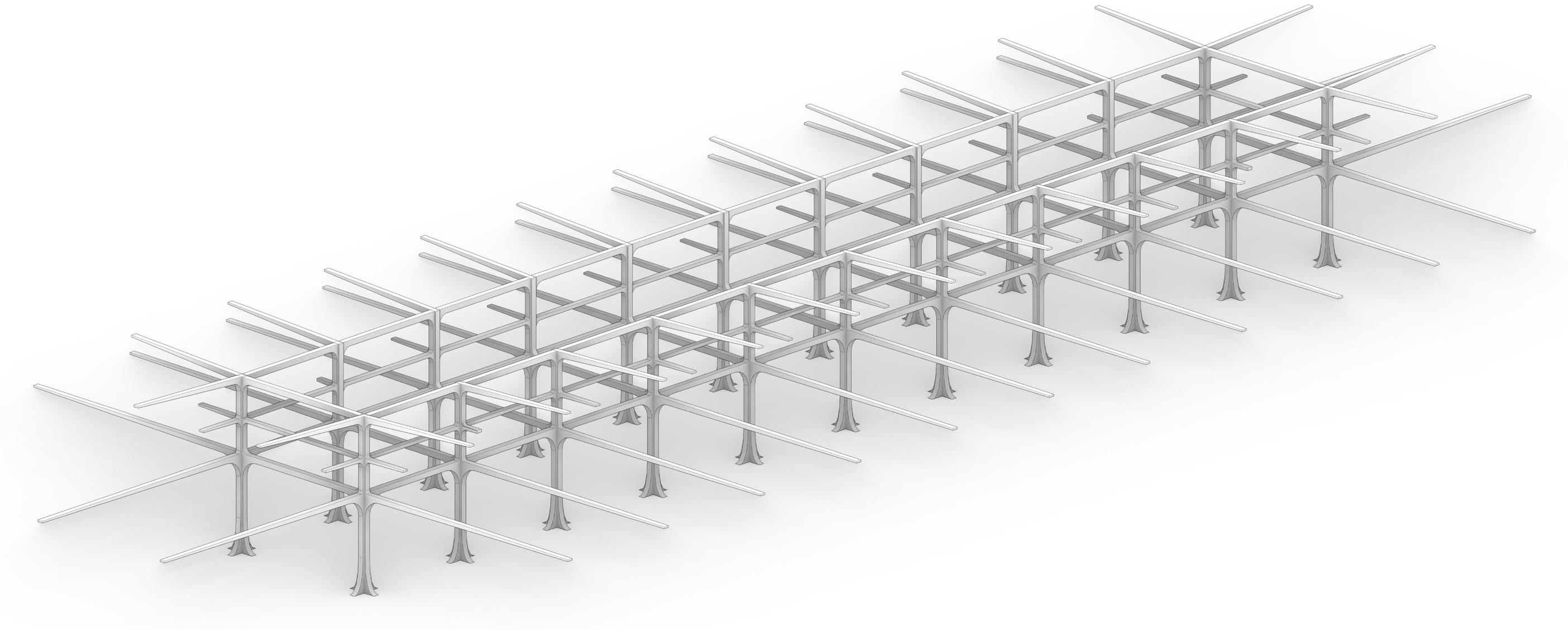

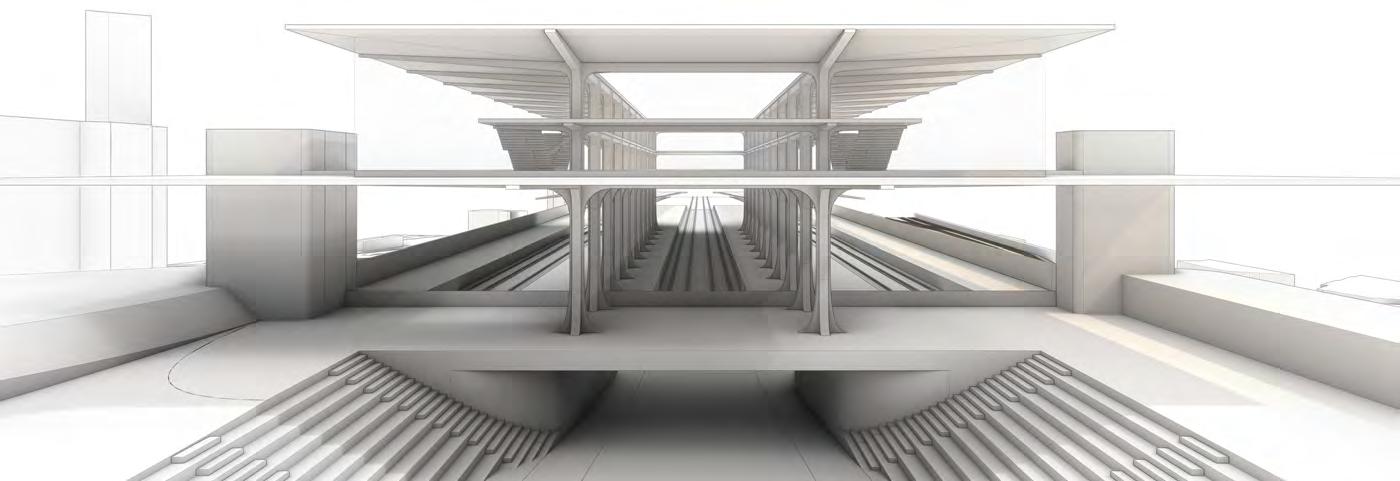

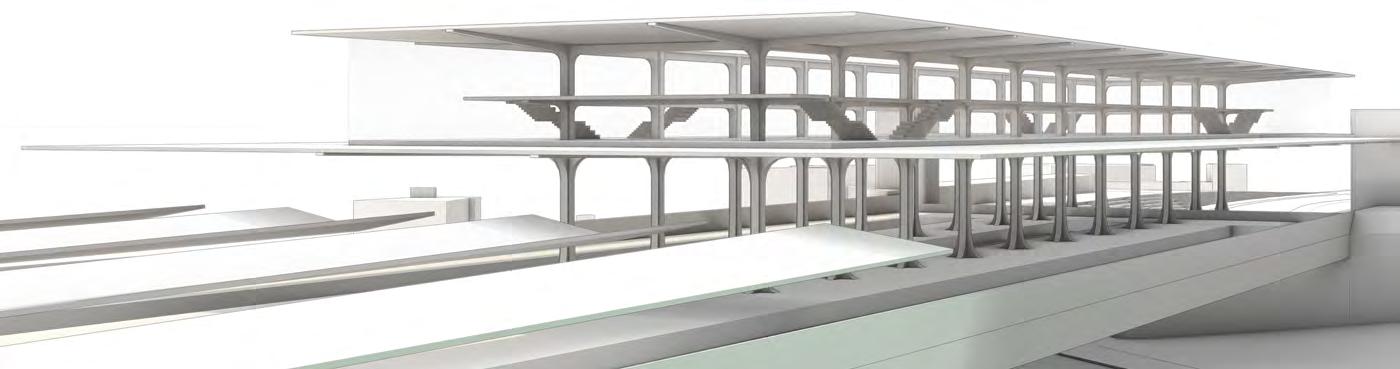

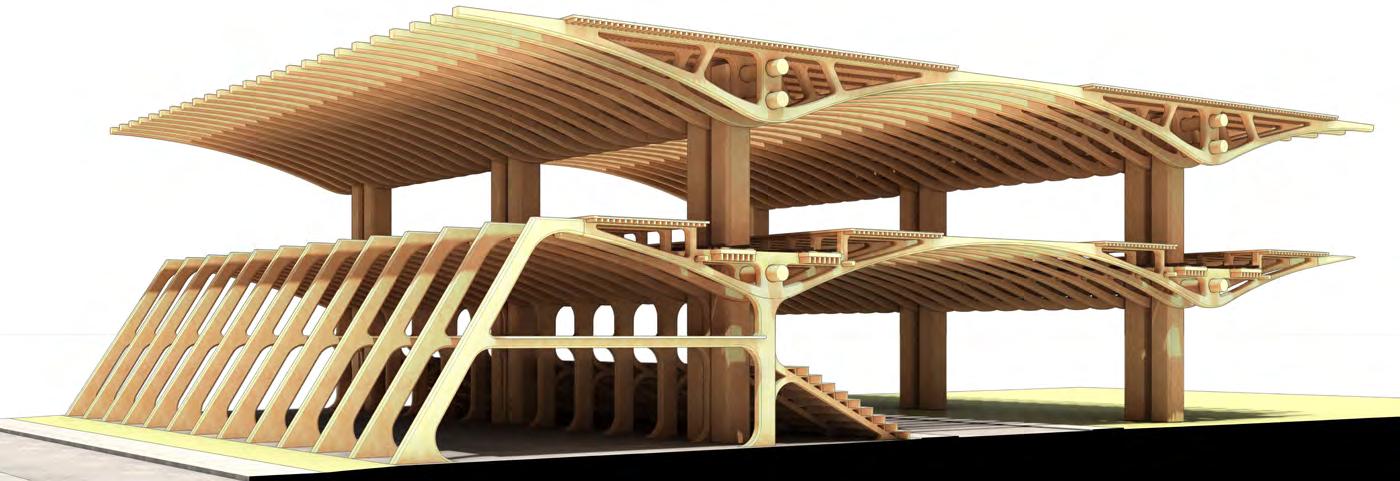

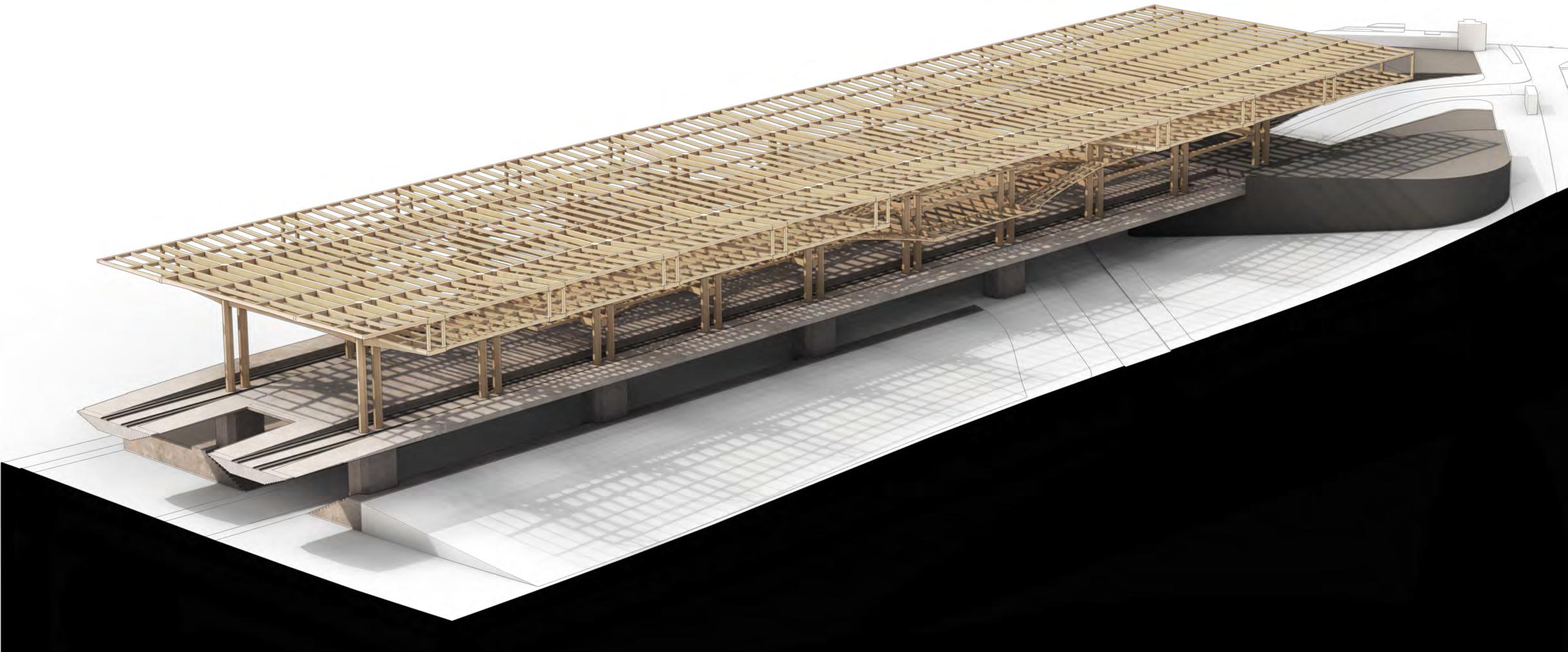

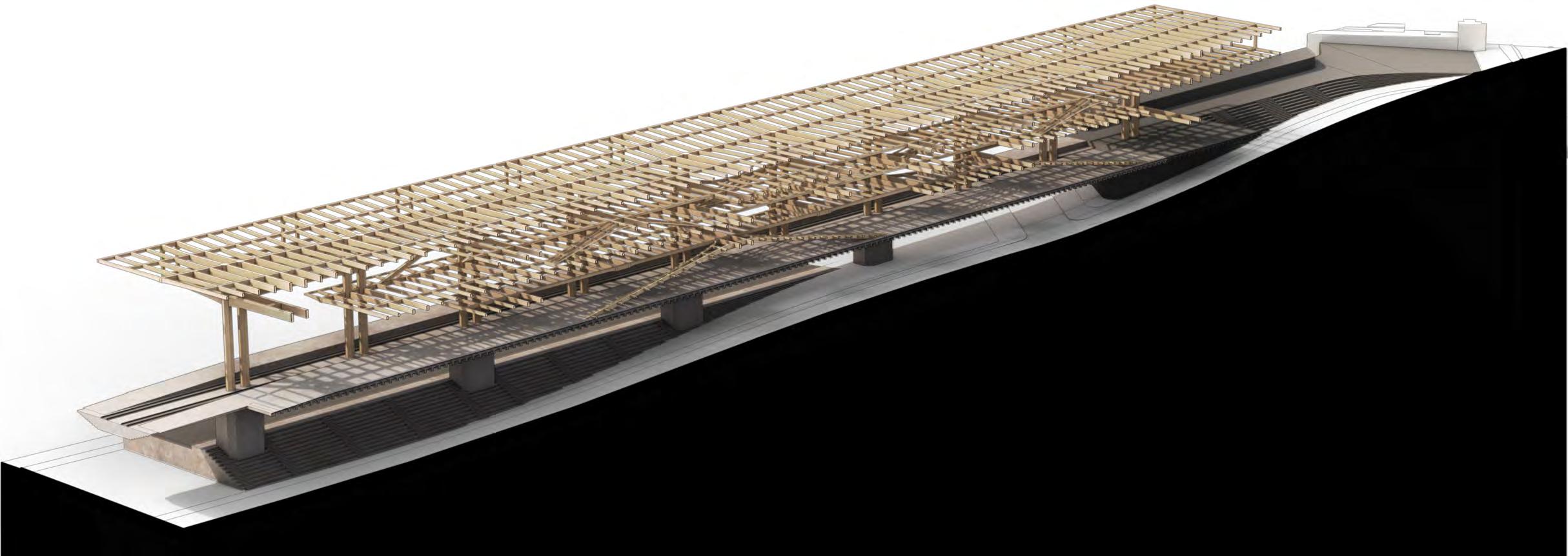

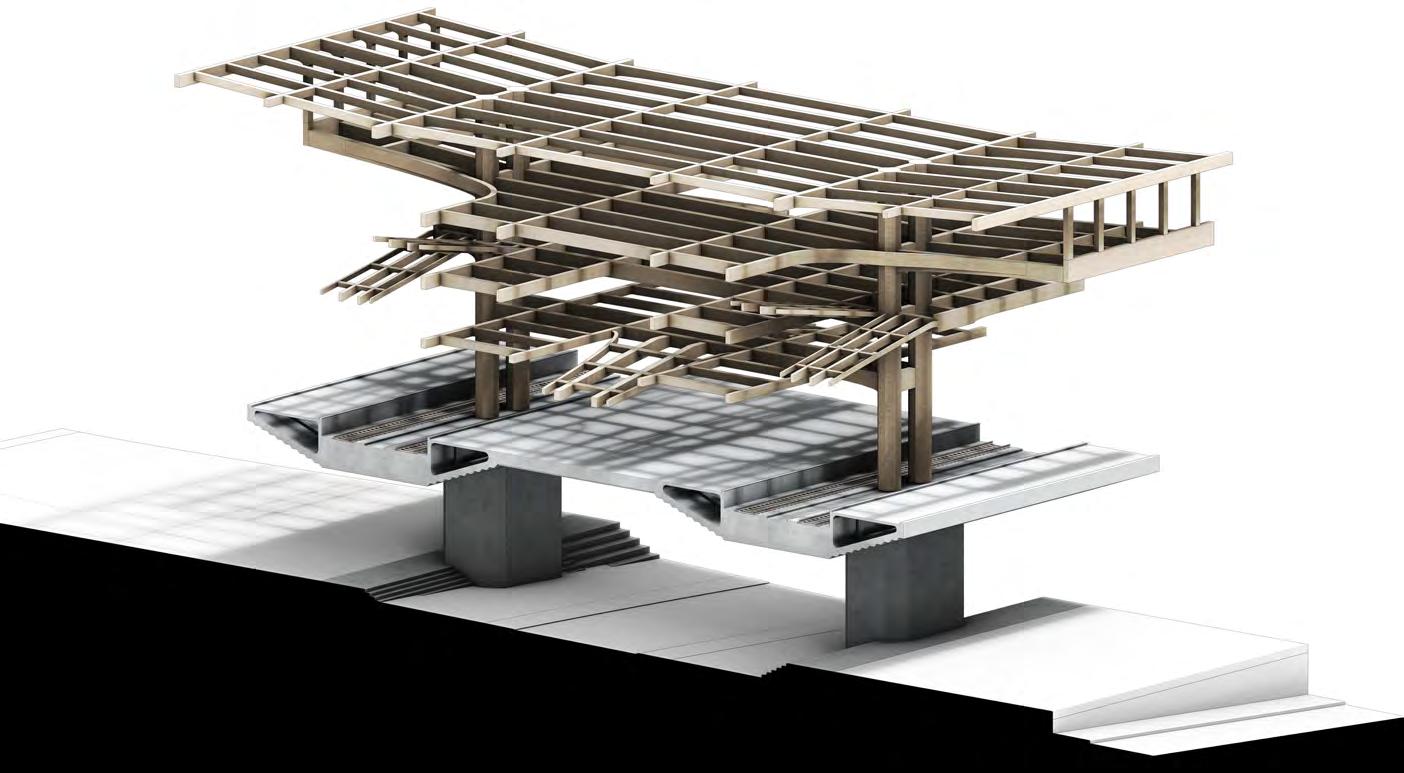

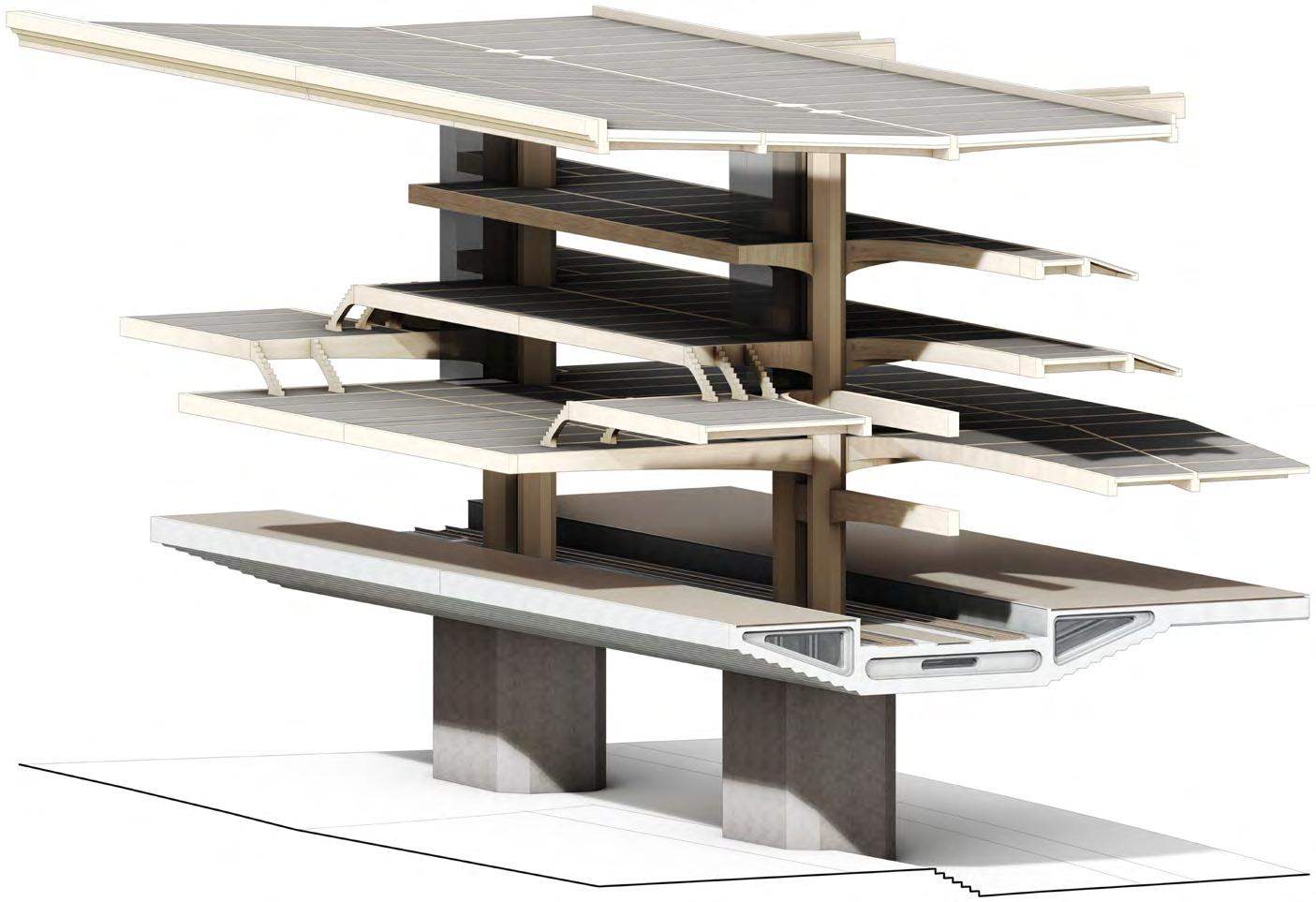

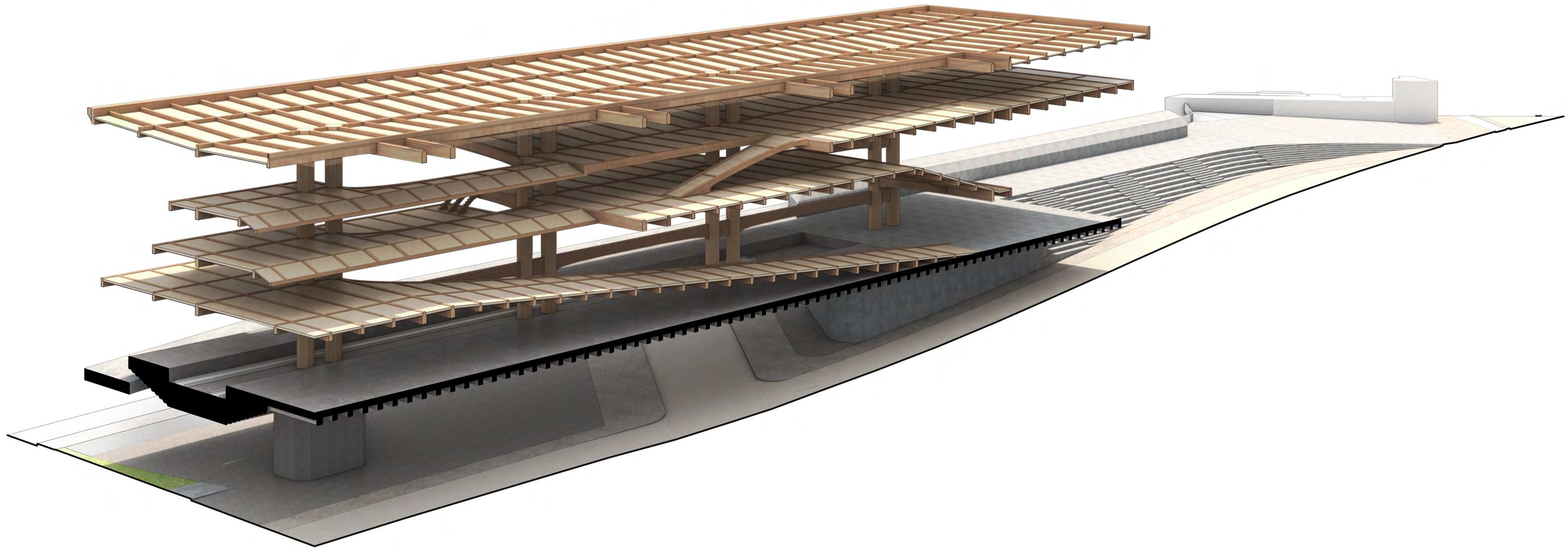

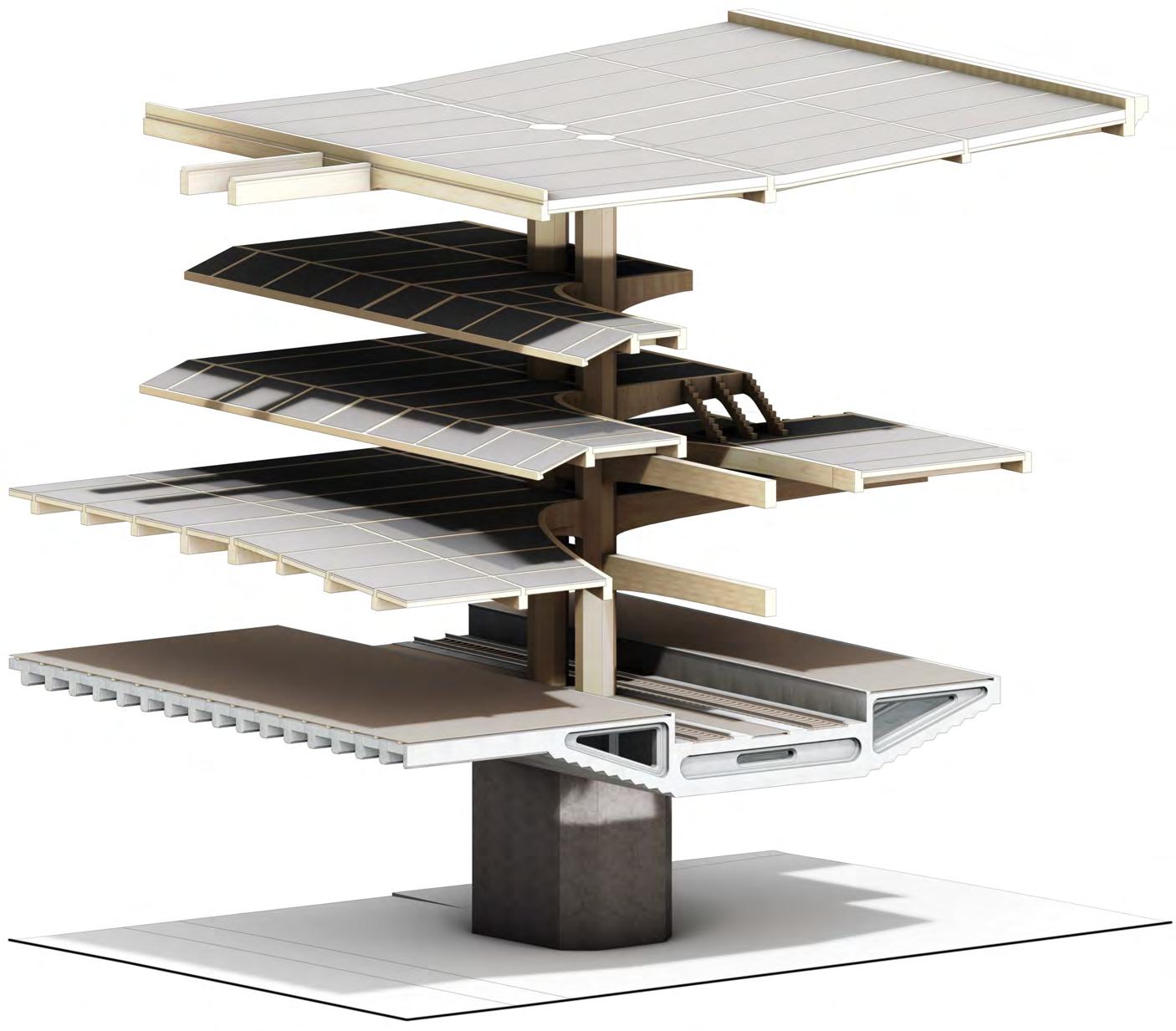

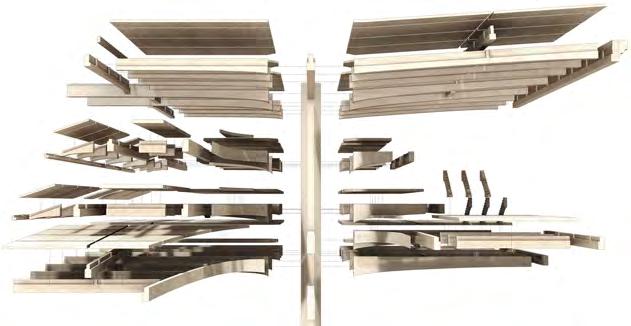

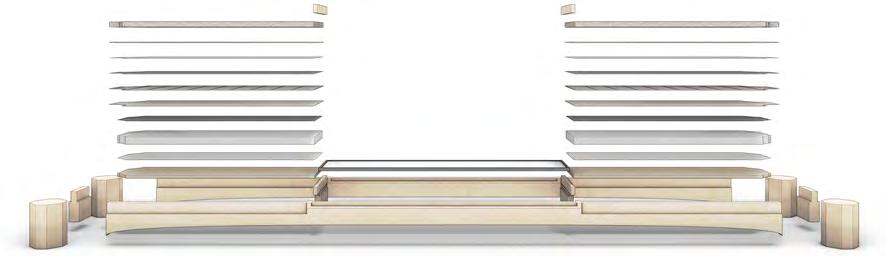

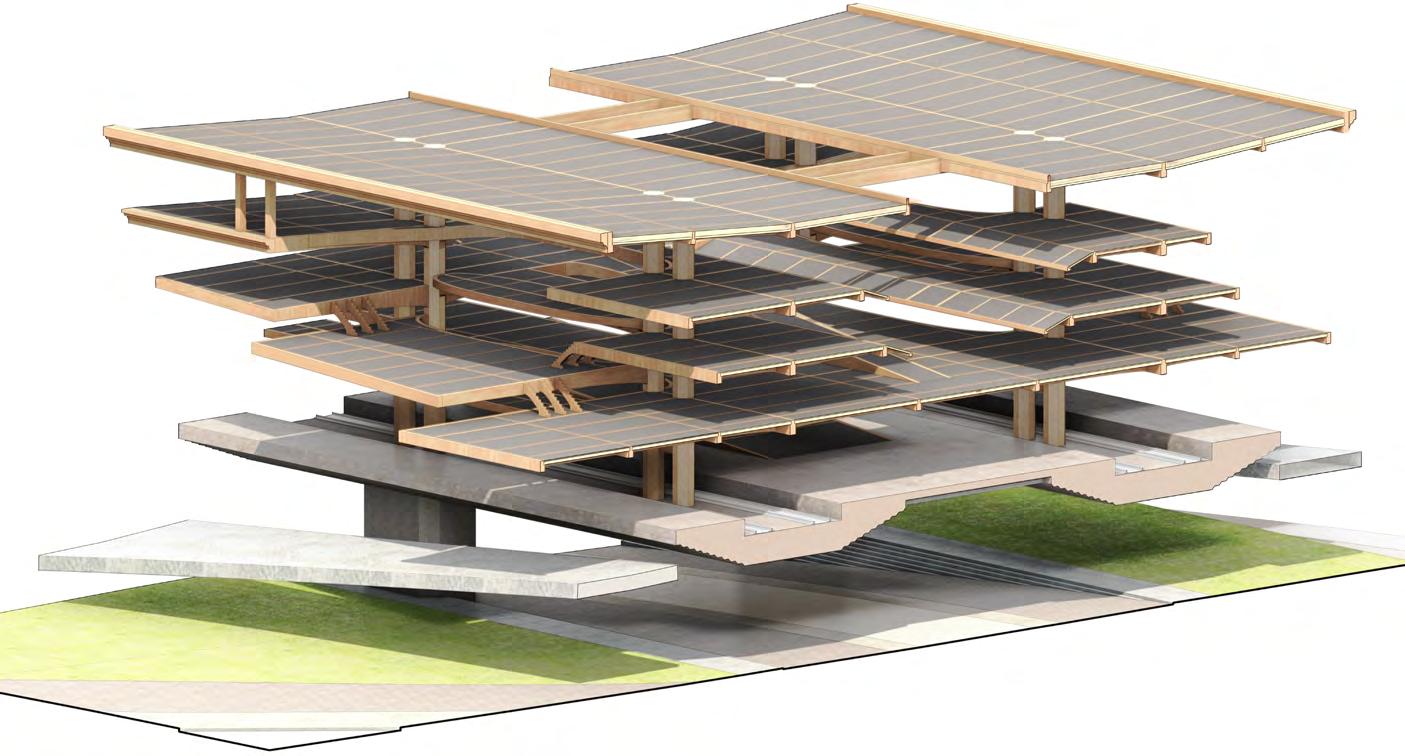

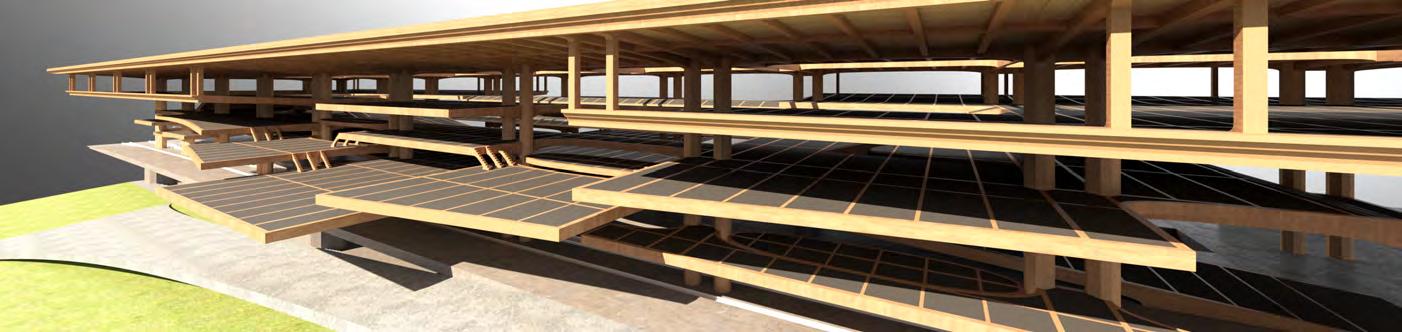

STRUCTURAL COMPOSITION TechnicalStructure

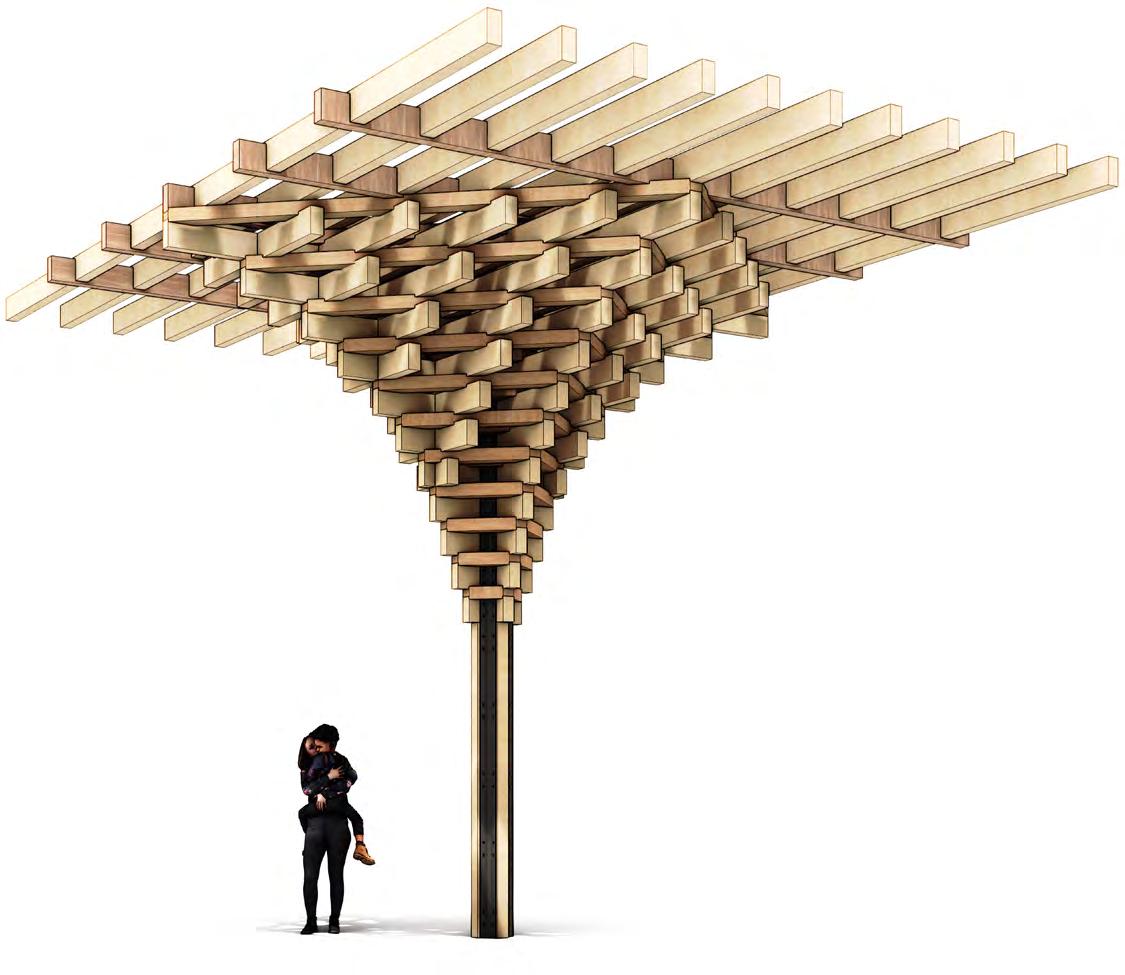

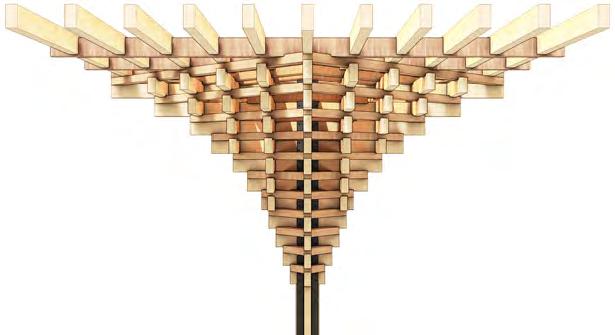

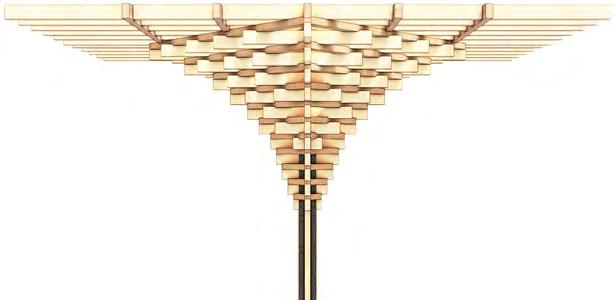

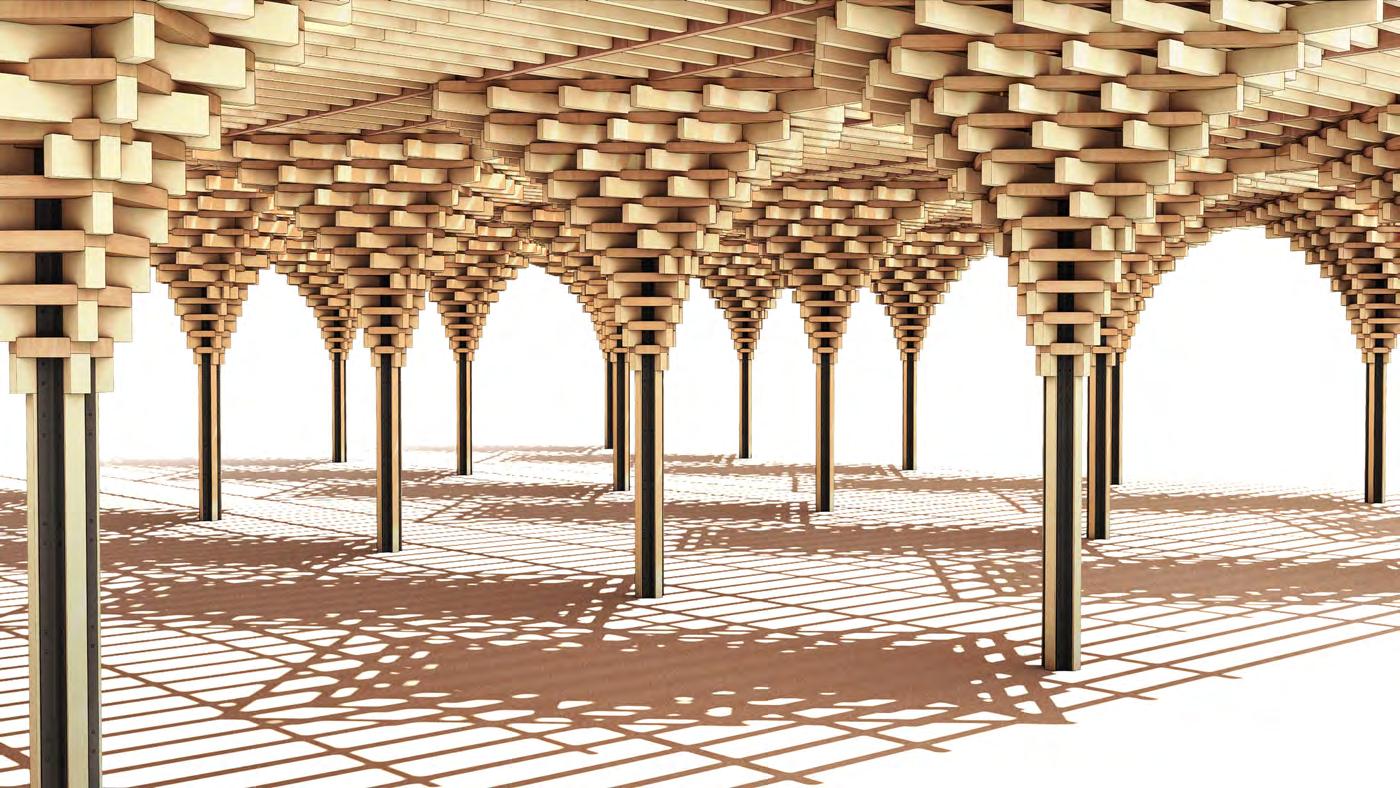

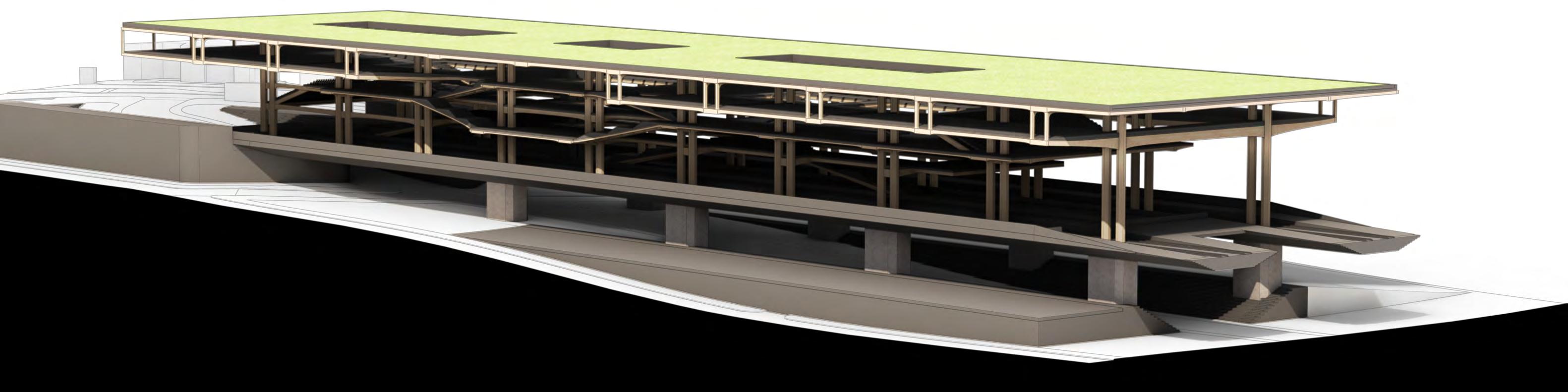

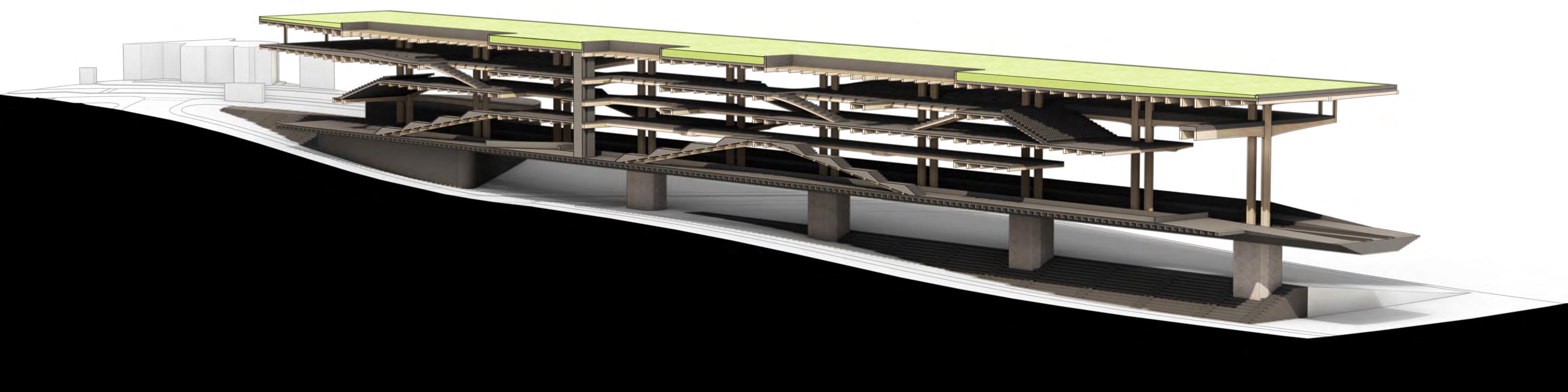

200mm 8-ply CLT panel 1500x1500mm glulam column 31m spanning glulam beam, 1500x500mm curving profile 60mm flooring grade rigid wood fibre insulation 12mm recycled rubber sound absorption layer Breathable floor protection membrane 1.5m spanning glulam beam 1500x500mm profile ExplodedFloorLayering+Structure 5.UnderFloorBuildup

1.Glulam+ConcreteColumns

2.PrimaryGlulamBeams 3.SecondaryGlulamBeams 4.CLTPanels

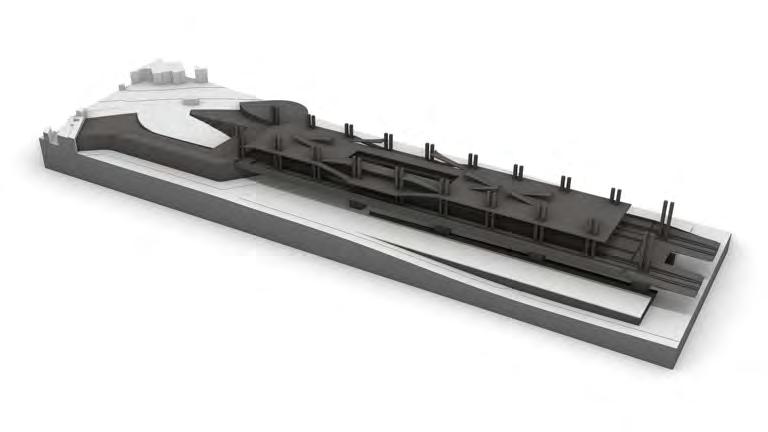

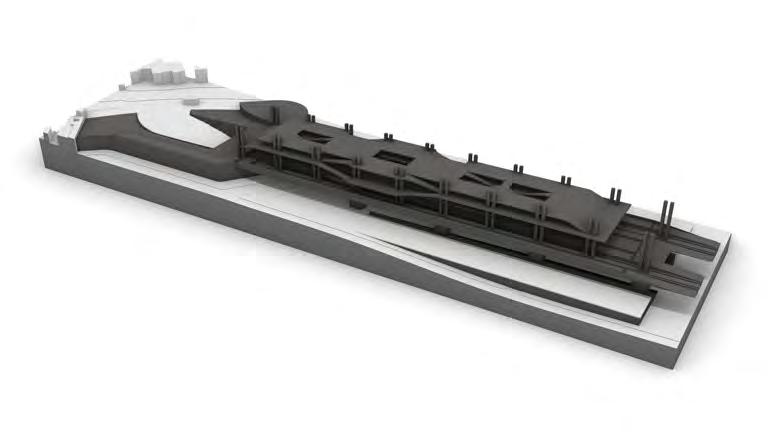

Glulam+CLTSuperstructure

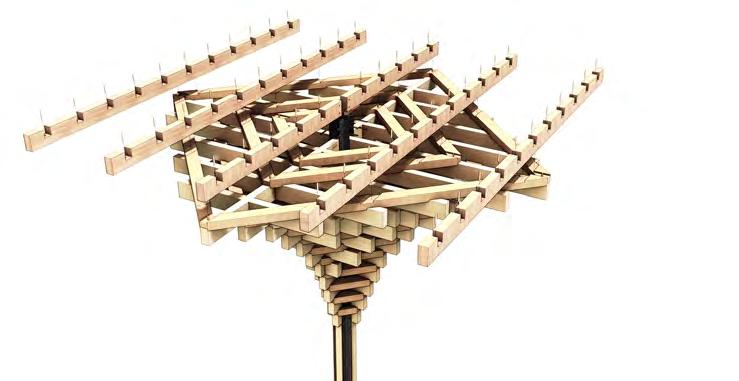

EXPLODED STRUCTURE TechnicalStructure

400mm

flat

fibre insulation board

145mm 5-ply CLT panel 19mm fine sand 25mm course sand

timber upstand ‘Flownet’ polyethylene drainage mesh 360mm

roof-grafe wood

Polymer bitumen membrane

30mm

1500x1500mm glulam column

concrete pavers

Growing

Geotextile (filter-grade fabric A14)

medium soil

PlantedRoofLayering+Structure

spanning glulam beam, 1500x500mm curving profile

1500x500mm

Double glazed

roof skylight Weather-resistant, air tight vapour control membrane

31m

1.5m spanning glulam beam

profile

ColumnBranches+FoundationsFragment

2.CantileveredPrimaryBeams

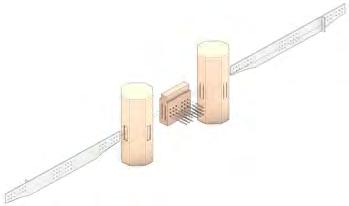

Structural Junction Studies

3.Primary+SecondaryBeams

4.AssembledFrame

1.DoubleColumnConnection GlulamFrameAssembly

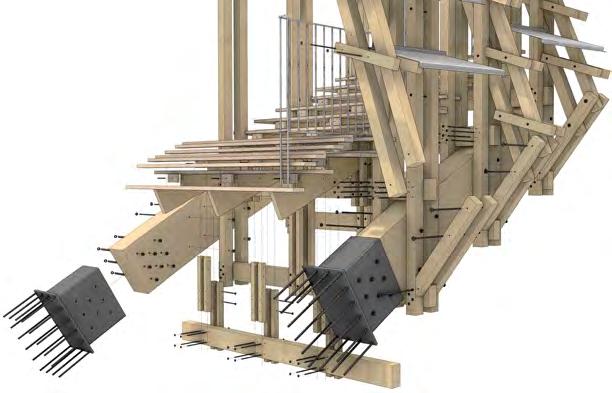

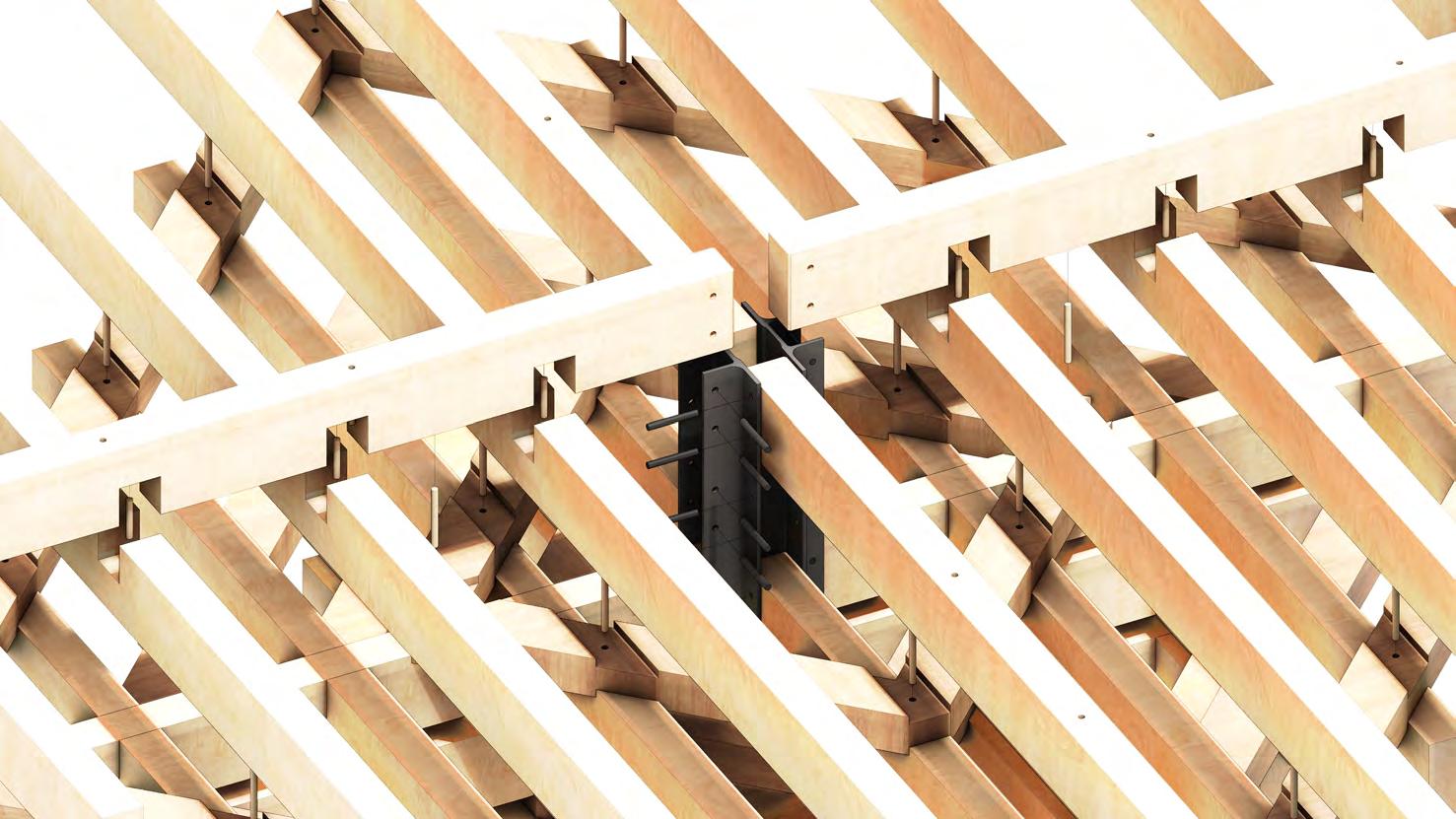

CONSTRUCTION DETAILS TechnicalStructure

Small diameter multiple concrete pile foundations

Reinforced concrete pile cap

Soil, sand + gravel layered backfill

Primary

Secondary

Internally ribbed reinforced concrete deck

glulam beam

Glulam

double column

glulam beam

CLT floor slabs

Stone maisonary stepped pomenade

Inset

Reinforced concrete pier

floor/roof buildup cavities

TECTONIC STUDIES TechnicalStructure

TECTONIC STUDIES TechnicalStructure

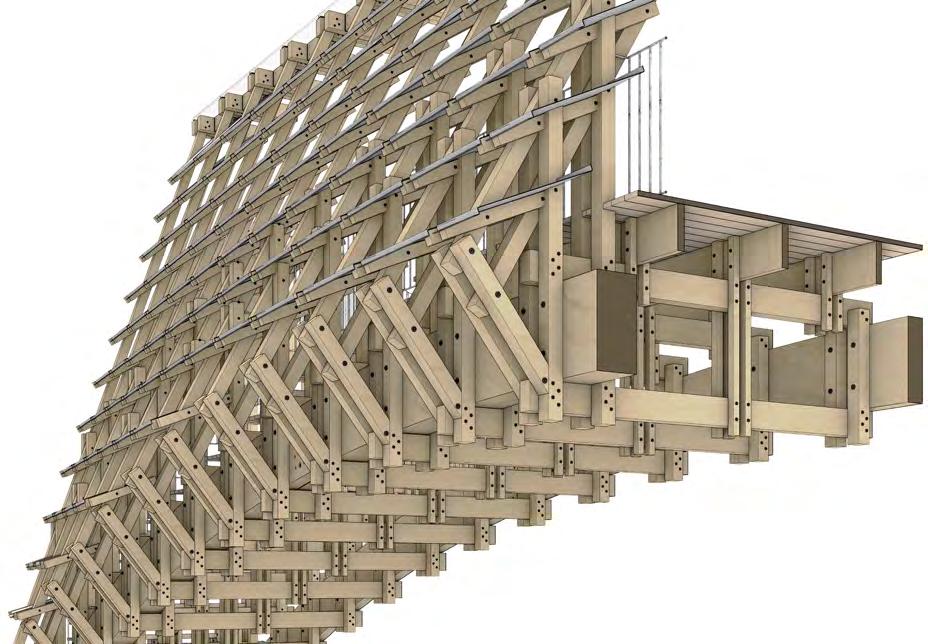

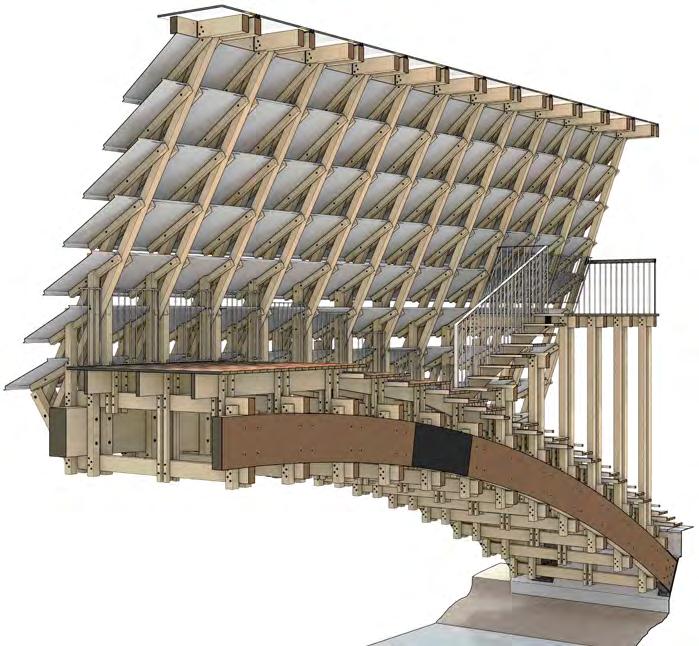

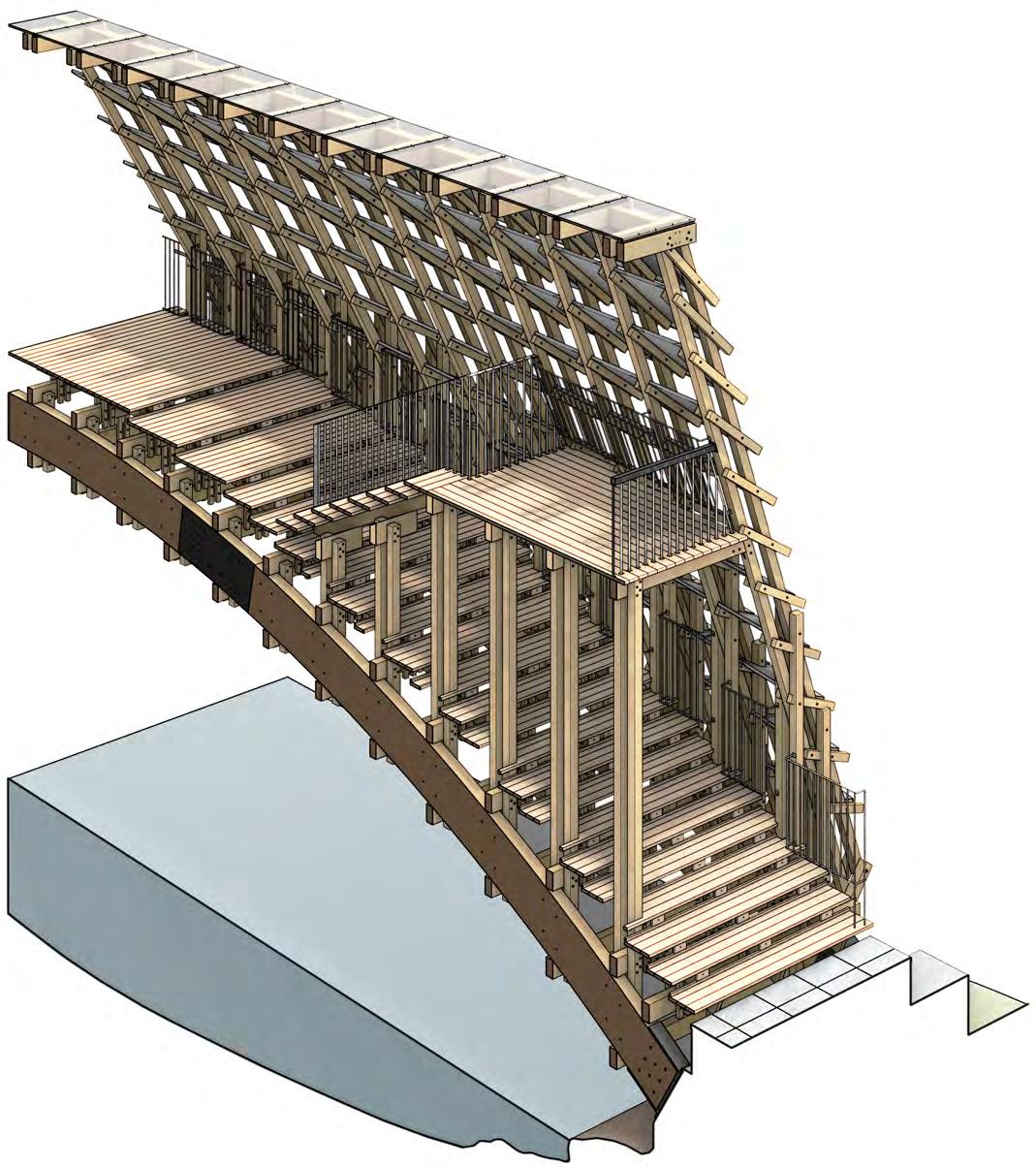

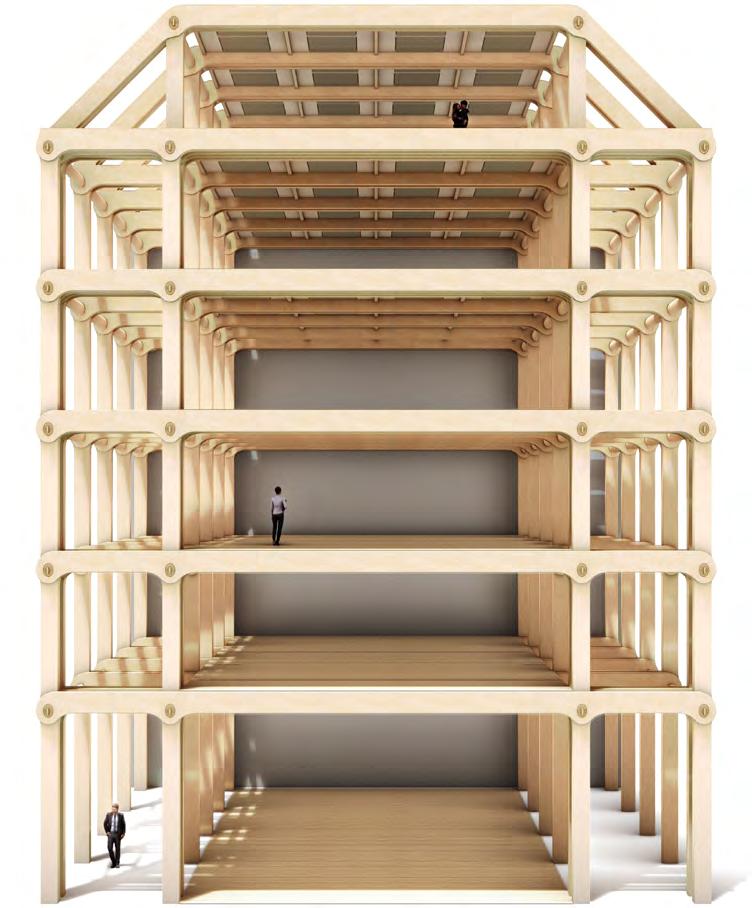

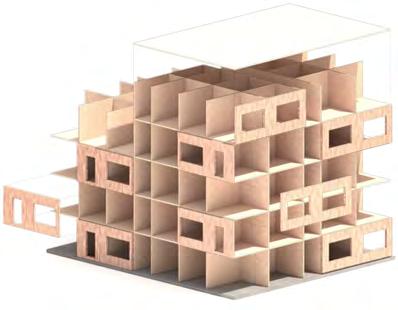

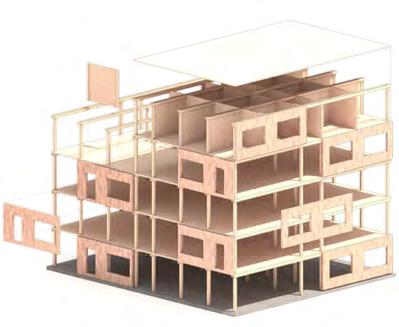

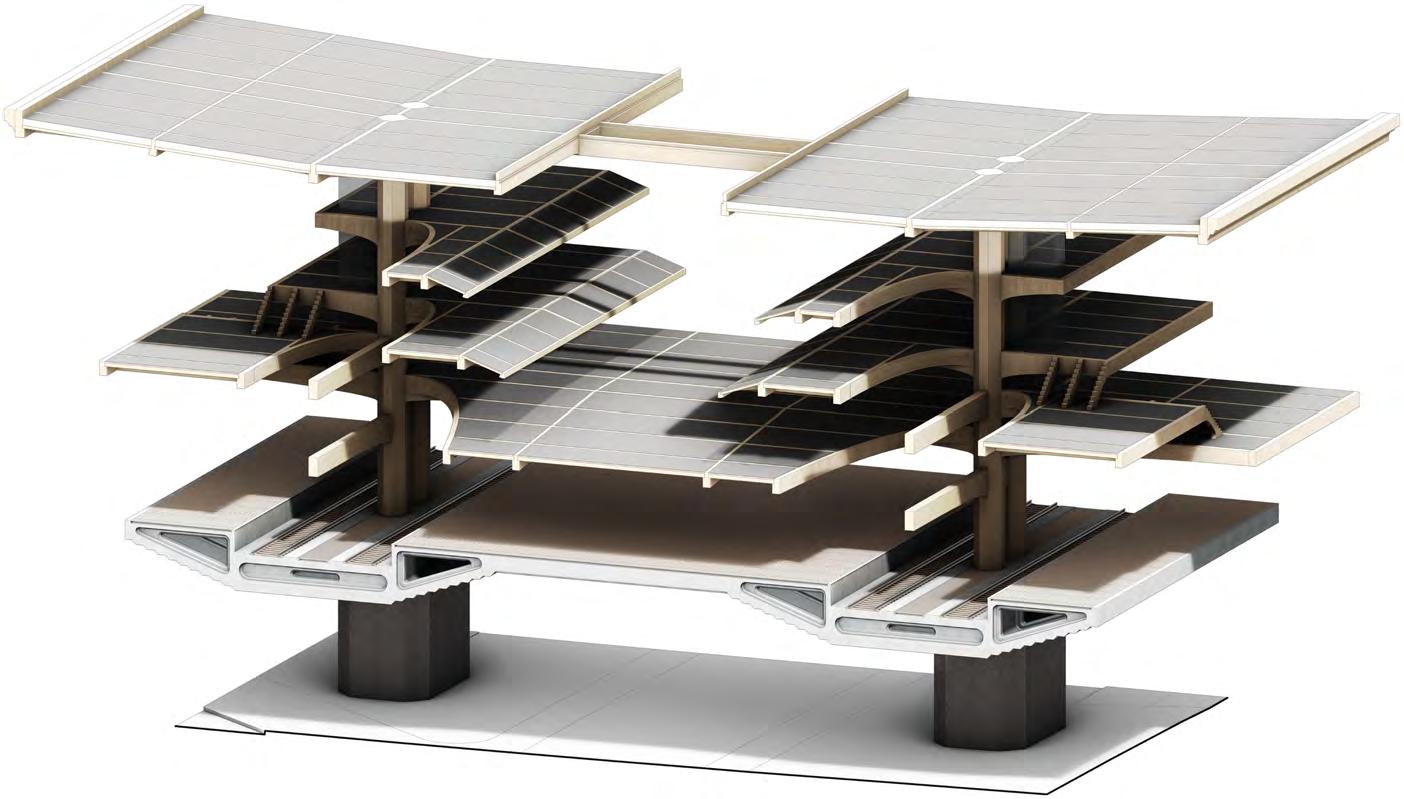

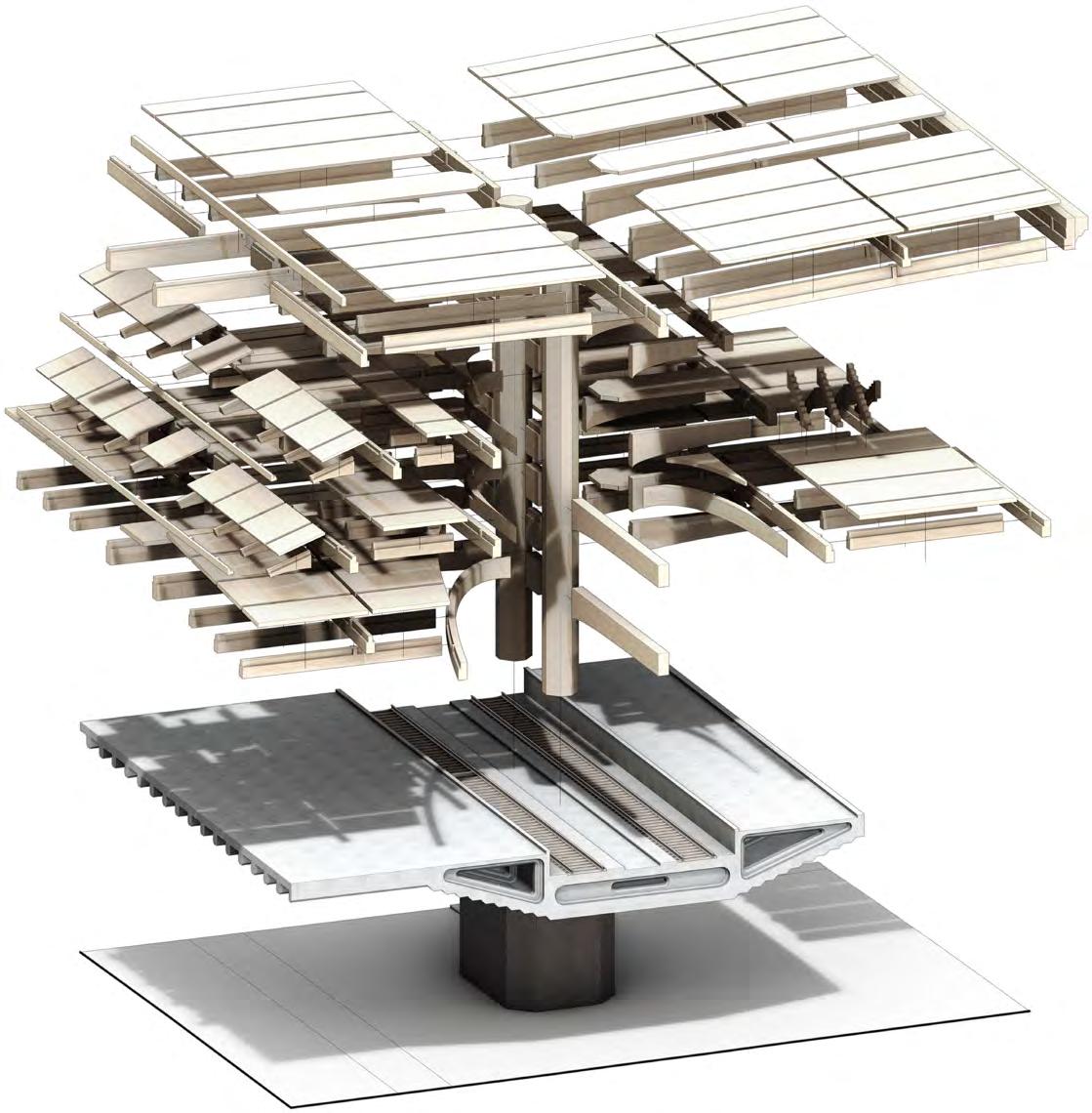

TechnicalStructure STRUCTURAL SYSTEM OVERVIEW

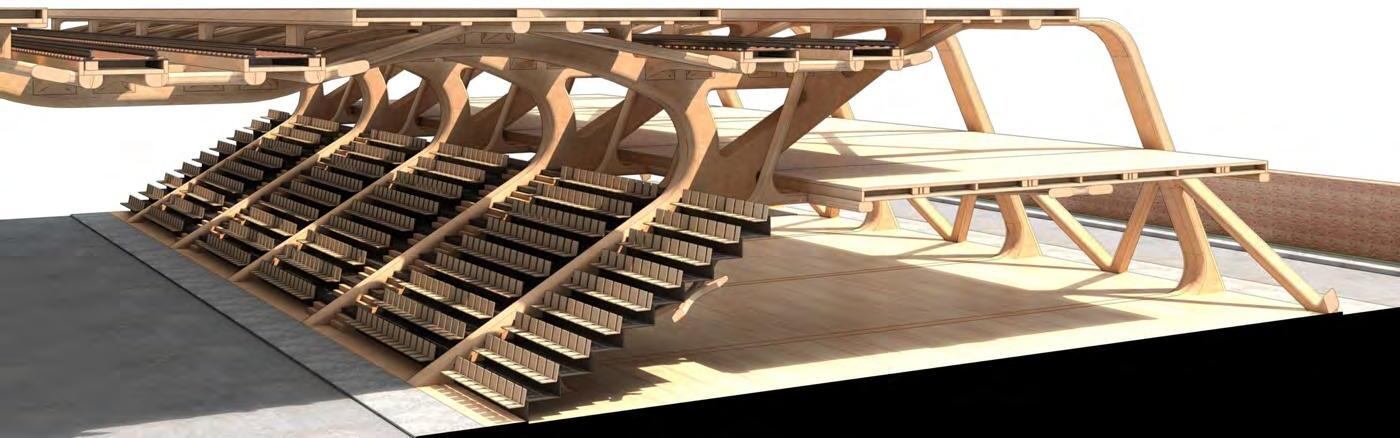

EXPANDING TERRACE

PLATFORMS FragmentStudies

TerracesFragment

RearExhibitTerraces

SteppedTerraceExtrusions EntranceExhibitPlatforms

DesignResolution

BuildingForm+Function

07

StationEntrance+FormulaESpectating

HS2Platforms+FormulaESpectating

+ FORMULA E INTERFACES

HS2

ProgrammeStudies

LevelInteractions

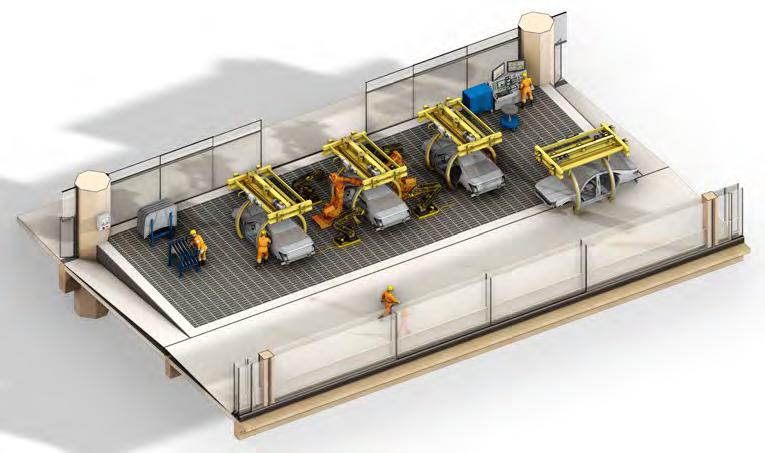

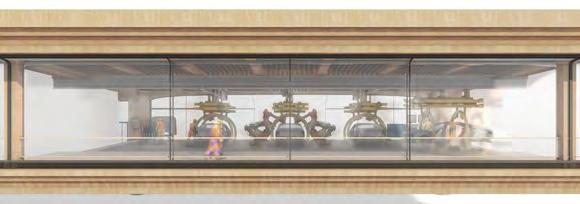

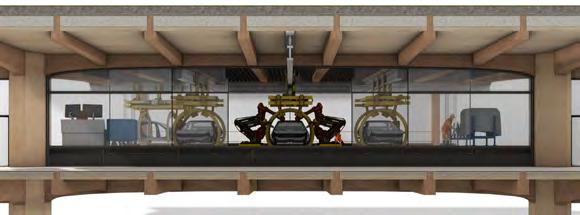

CAR CONVEYOR SYSTEM AutomatedConveyorSystem

ProgrammeStudies

ASSEMBLY BAY FRAGMENT ProgrammeStudies

ElevationViews AssemblyBayFragment

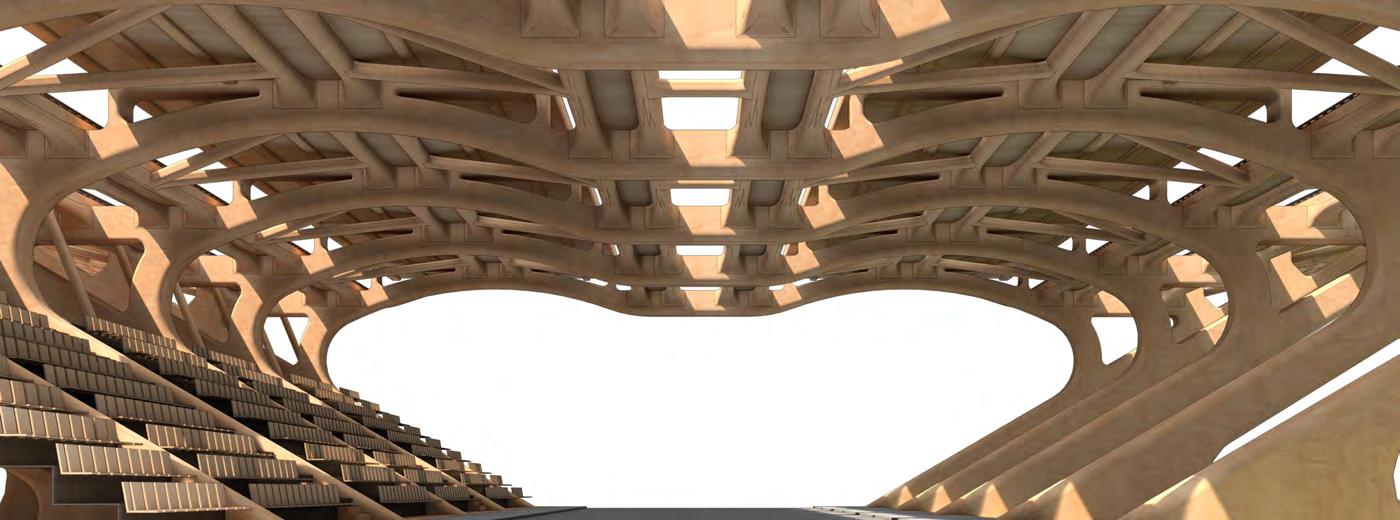

DOUBLE SKIN ROOF FACADE Envelope EnvelopeSection Interior Section ExteriorElevation EnvelopeInterior EnvelopeExterior Planted roof layering Structural roof layering Acoustic timber baffles Guttering + water colection Copper coping cover Interior ventilation out Exterior ventilation out Interior glazing Exterior glazing Openable facade Balustrade Guttering Exterior ventilation in Interior ventilation in Envelope cavity Acoustic Thermal AirFlow

ENVELOPE SYSTEM Envelope EnvelopeStrategy Fully enclosed space Photovoltic power generating skylight Planted roof Partially enclosed space Unenclosed sheltered space OpenableDoubleSkin 9m full bay opening 9m full bay opening 1m single bay opening Sliding walls contained in cavity Full height sliding glass walls

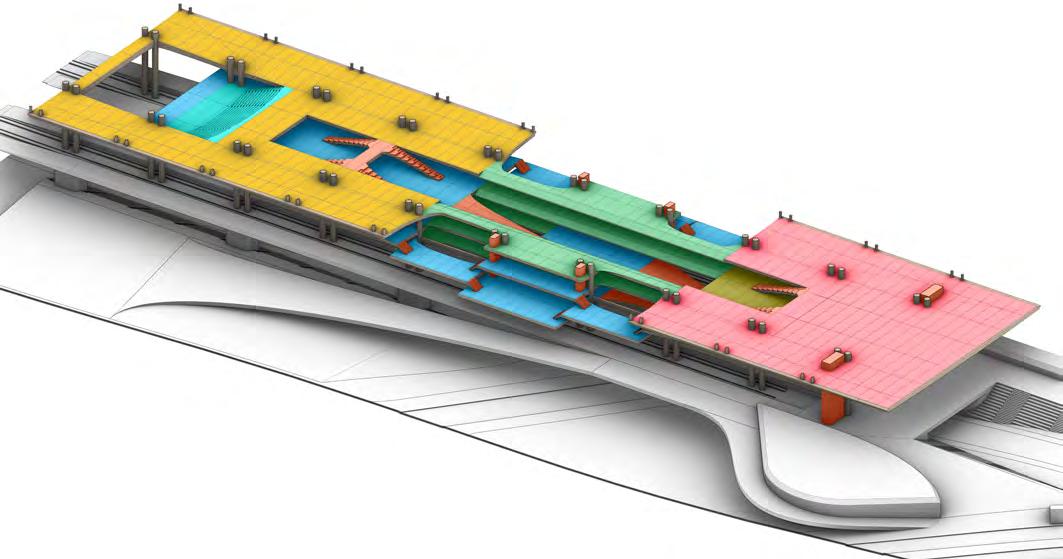

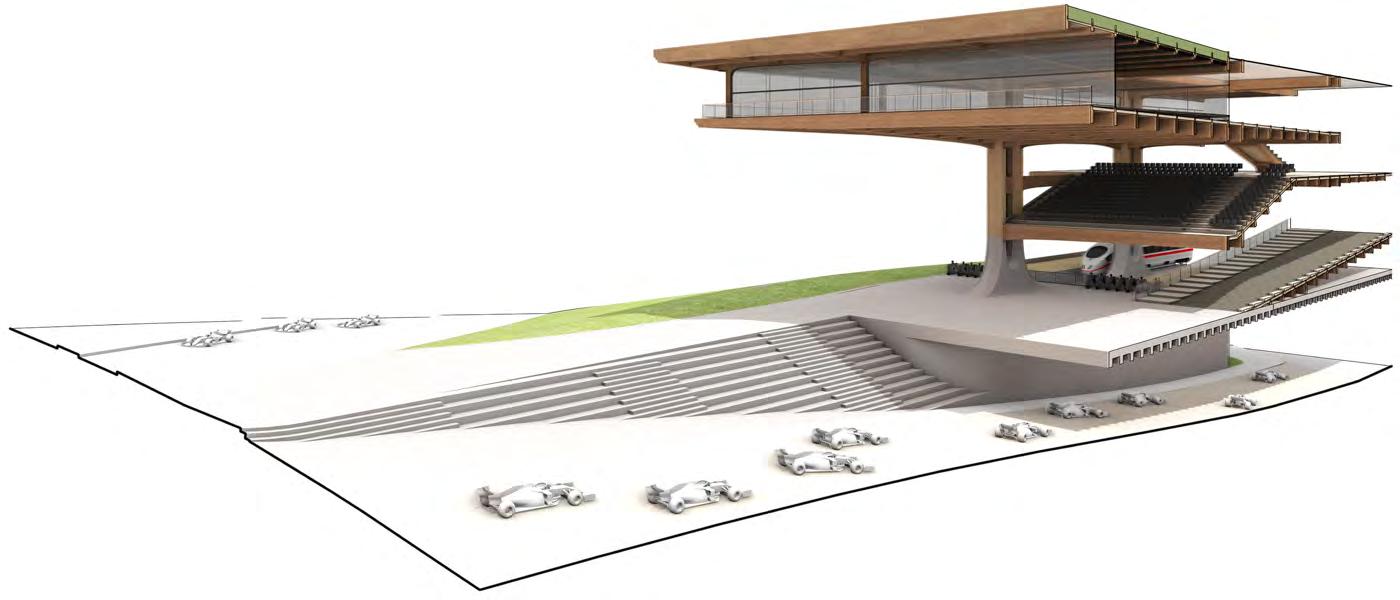

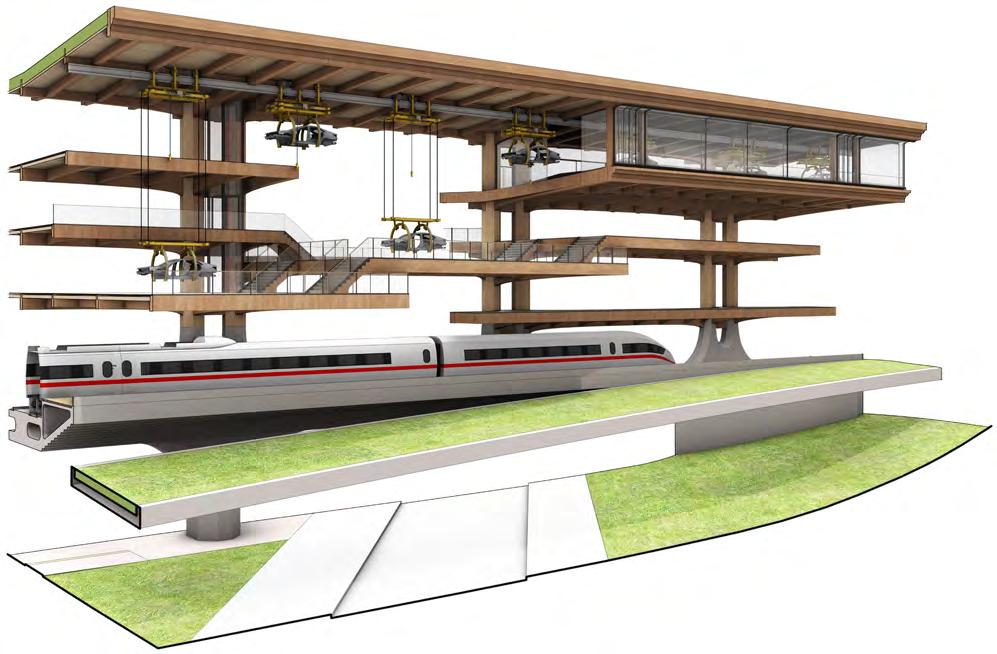

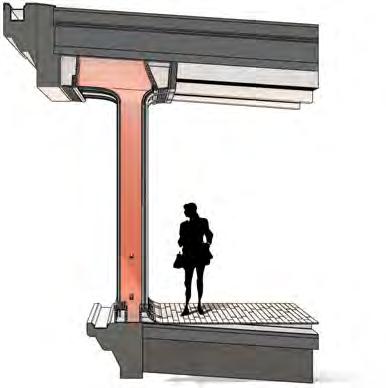

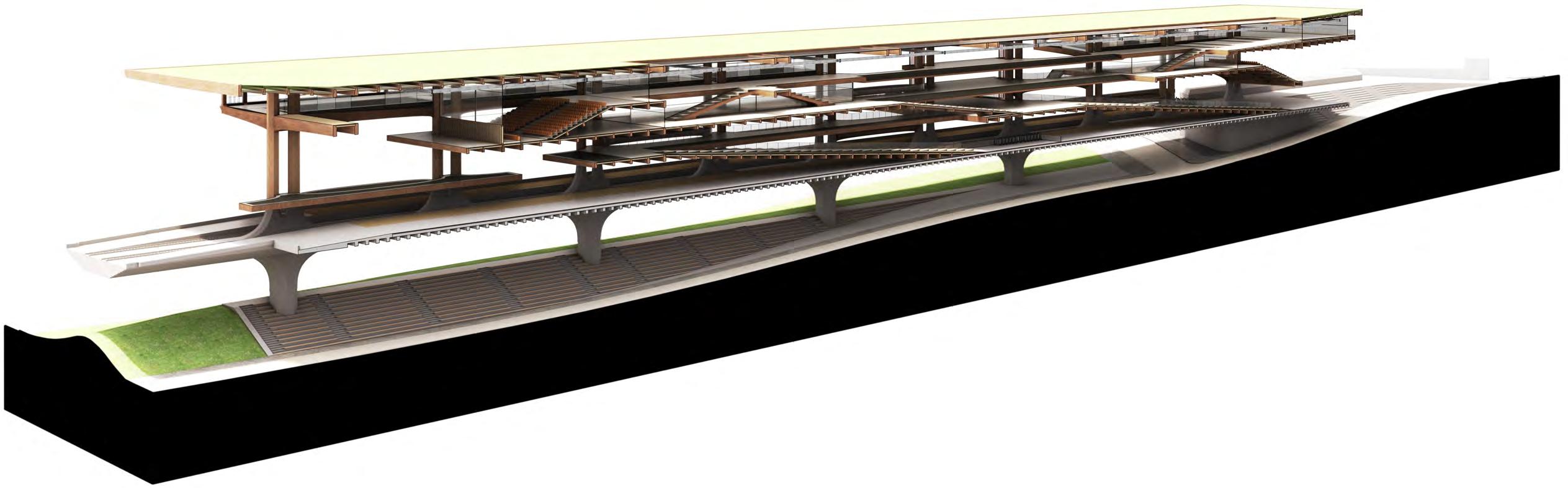

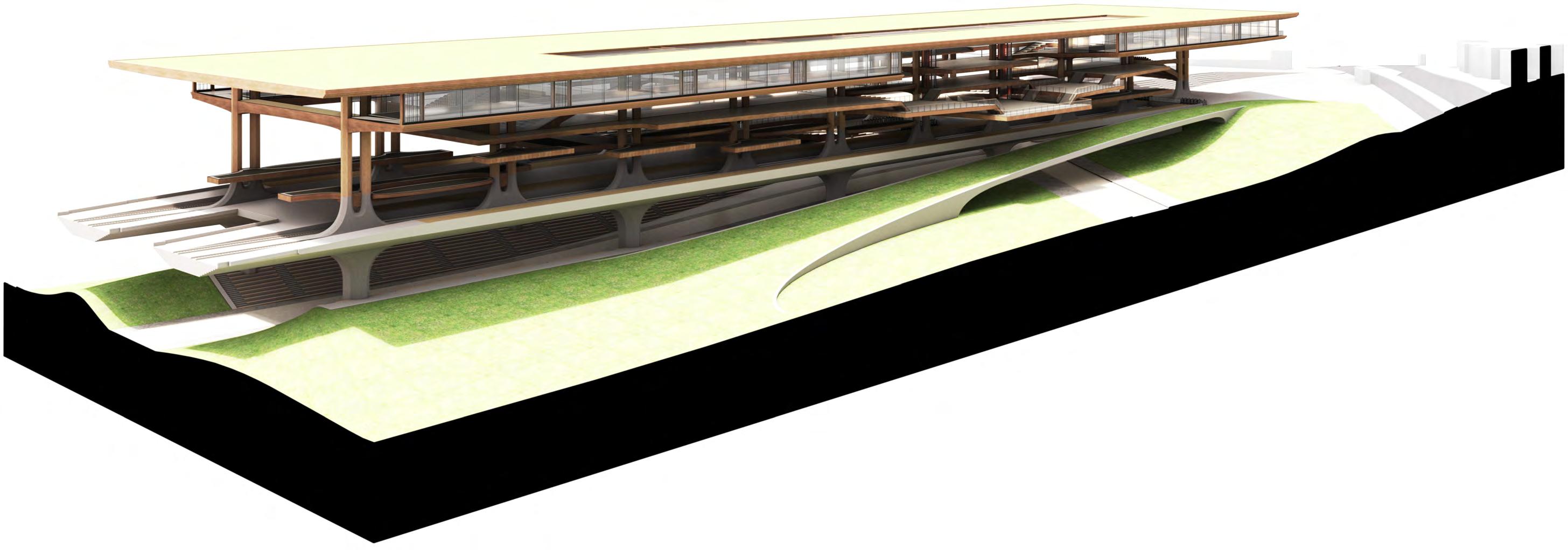

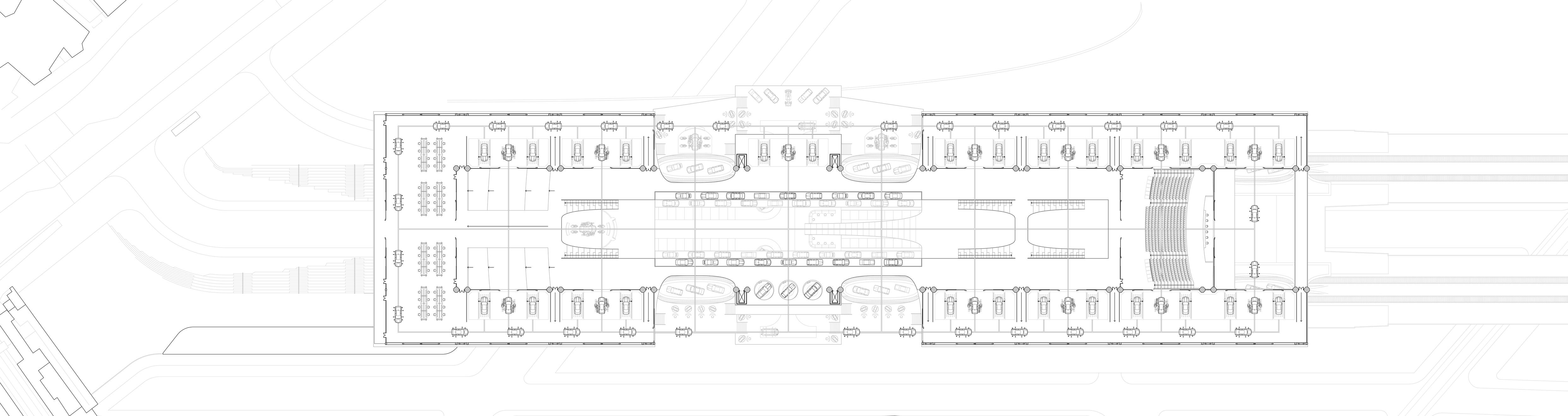

Ceilingcarconveyorrailingsystem 36.Prototypecardisplay+discussion 37.Designhub+prototyping 38.Cityoverlookbalcony 39.Carmanufacturingbays

Openingconveyorpassagedoors

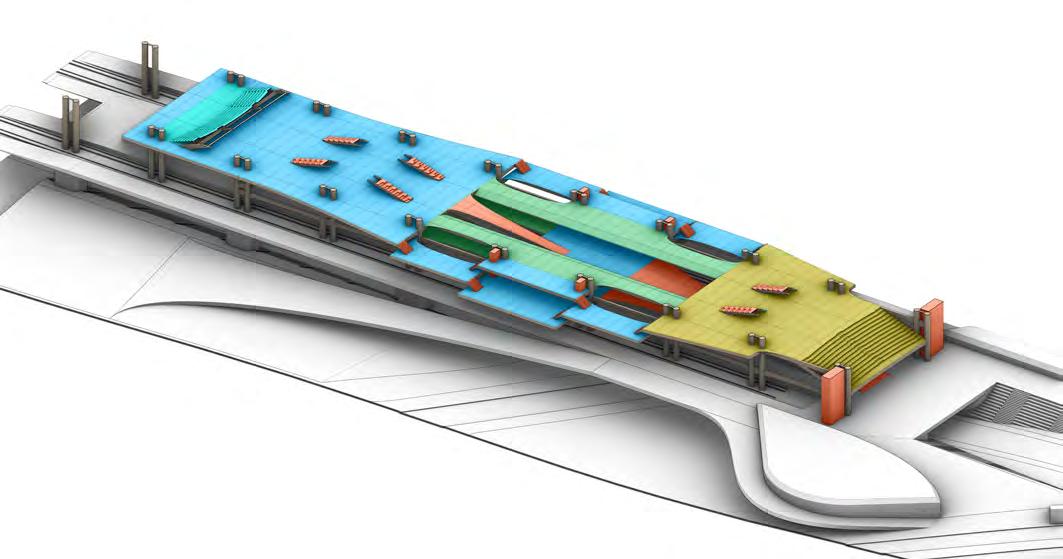

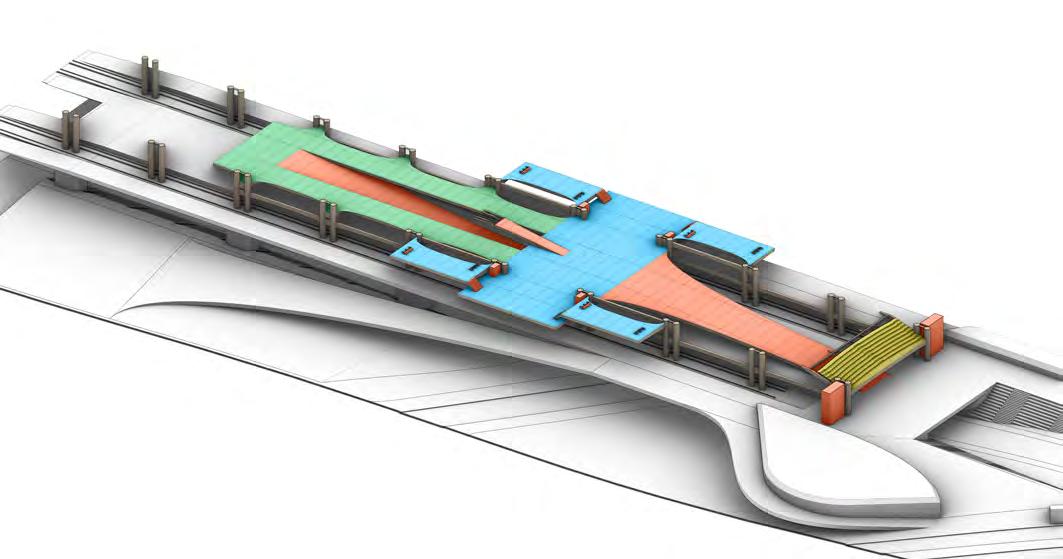

BUILDING OVERVIEW ProgrammeStudies 40 39 41 23 8 19 22 24 30 18 42 43 3 10 11 12 20 13 25 33 31 32 34 26 27 35 28 21 14 15 16 4 5 6 37 38 36 29 17 7 9 2 1 1.Slopingplantedbank 2.Viaductpiercolumns 3.Steppedpromenadeandspectating 4. FormulaEcoursetrack 5.Intersectingroadtocitycentre 6.Entrancepierandinternalcarparking 7.Steppedpromenadeandseating 8.Plantedbridgepassagetoentrance -1F:FormulaEPromenade 0F:HS2Station 9.Railwayviaduct 10. Concretecolumnbase 11.Stationexhibitionplatforms 12.Stationplatforms 13.Stationconcourseentrytobuilding 14. Ticketbarrierthreshold 15. Stationconcourse 16.Primaryentrytobuilding 17. Ticket+stationoffice+ammenities 18. Stationentrance 19.Birminghamcitycentre 2F: FormulaE+Educational 25.Externalcarexhibitbalcony 26. Presentation+eventstheatre 27.Studentdesign+trainingcentre 28.Atriumexhibitiondisplays 29. FormulaEstandsandammenties 30.FormulaEentrance+exhibitplatform 4F: PlantedRoof 42.

43.Photovolticatriumrooflight 1F: Exhibits+Customisation 20.BritishLeylandheritageexhibition 21.Atriumentrancelobby 22.Carexhibitionplatforms 23.Customcardesign+deliveryplatform 24.Customcarassemblyplatform

31.

32.

33.

34.

35.

41.

Biodiversityupliftgreenroof

3F: BritishLeyland+Manufacturing

Primarydoubleglulamcolumns

Primaryglulambeams

Externalbridgepassage

Eventdisplayspace

40.Liftlobby+exhibitplatform

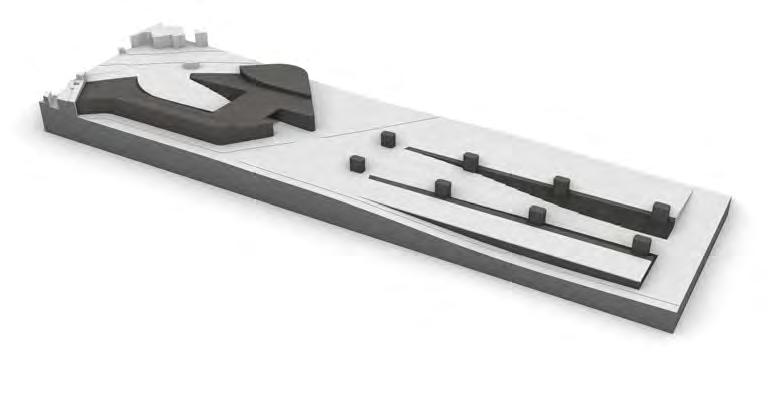

SITE PLAN Plans+Sections N 1:2,000 0 10m 25m 50m

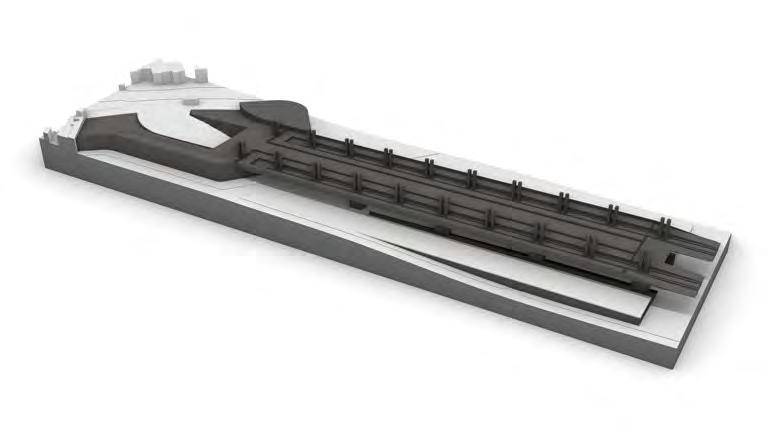

-1F: FORMULA E PROMENADE N 1:500 2m 5m 10m Key 1.Steppedpromenadeandseating 2.Goodsdeliveryanddropoffpoint 3.Viaductpiercolumns 4.Plantedbridgepassagetoentrance 5. FormulaEcoursetrack 6.Steppedpromenadeandspectating 7.Slopinggrassbank 8.Intersectingroadtocitycentre 9.Intercitytramtracks 1 6 9 3 5 2 4 8 7 Plans+Sections BB BB AA AA

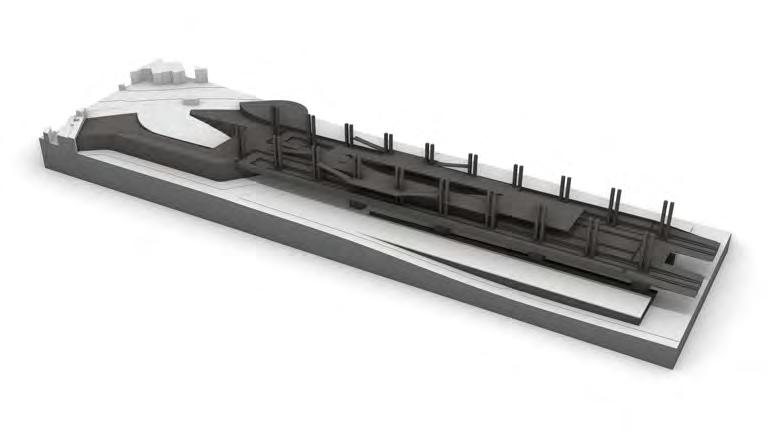

0F: HS2 STATION N 1:500 2m 5m 10m 6 7 5 1 2 3 4 8 14 9 12 13 11 10 Key 1.Busstop 2.Destinationretail/dining 3.Impulseretail/dining 4.Ticket,information+stationoffice 5.Steppedpromenadeandseating 6.Primarystructurecolumns 7.Plantedbridgepassagetoentrance 8. Stationentranceticketbarriers 9.Primaryentrytobuilding 10.HS2stationplatforms 11.Stationconcourse+kioskspaces 12. Ticketbarrierthreshold 13.Stationconcourseentrytobuilding 14.Railwayviaduct Plans+Sections BB BB AA AA

1F: EXHIBITS + CUSTOMISATION N 1:500 2m 5m 10m 1 3 4 8 6 11 9 10 7 13 12 14 5 2 Key 1.FormulaEspectatorstands 2.Carexhibitplatforms 3.Primaryentrytobuilding 4.Customcarassemblyplatforms 5.Customcarcustomerdesignplatforms 6.VR/ARexhibits 7.Cardisplaybalcony 8.Carconveyordeliverypoint 9.Atriumentrancelobbyreception 10.Staircasetoupperlevels 11.Passengerliftstoupperlevels 12.Stationconcourseentrytobuilding 13.BritishLeylandheritageexhibition 14.Stationcarexhibitplatforms Plans+Sections BB BB AA AA

2F: FORMULA E + EDUCATIONAL N 1:500 2m 5m 10m 1 5 3 4 6 7 8 9 10 11 12 13 2 1.FormulaEspectatorstands 2.Spectatorkiosksandammenities 3.FormulaElounges 4.FormulaEentrance+exhibitplatform 5.Interactivecarassemblycustomisation 6.Carexhibitplatforms 7.Atriumcarexhibitionledges 8.Liftlobby+exhibitplatform 9.Studentdesign+trainingcentre 10.Externalworkspace 11.Collaborativedesignreviewspace 12. Presentation+eventstheatre 13.Externalcarexhibitbalcony Key Plans+Sections BB BB AA AA

3F: BRITISH LEYLAND + MANUFACTURING N 1:500 2m 5m 10m 3 4 5 6 7 8 9 10 11 12 2 1 3 1.Cityoverlookbalcony 2.Ceilingcarconveyorrailingsystem 3.Designhub+prototyping 4.Prototypecardisplay+discussionspace 5.Car3Dprinting+manufacturingbays 6.Openingconveyorpassagedoors 7.Non-enclosedmanufacturingexhibit 8.Liftlobby+exhibitplatform 9.Atriumcarexhibitionledges 10.Eventdisplayspace 11. Presentation+eventstheatre 12.Externalbridgepassage Key Plans+Sections BB BB AA AA

4F:

N 1:500 2m 5m 10m Plans+Sections

PLANTED ROOF

3.

4.

5.

4 3 2 1 5 BB BB AA AA

1.Plantedroofparapet 2.Atriumskylightparapet

Biodiversityupliftgreenroof

Primaryglulambeams

Photovolticatriumrooflight Key

FormulaEspectatorstands

Spectatorkiosksandammenities

Atrium+platformexhibits

Collaborativedesignreviewspace

Externalcarexhibitbalcony

Cityoverlookbalcony

SECTION AA Plans+Sections N 1:500 2m 5m 10m Key 1.

2.

3.

4.

7.

14.

15.

16.

17.

18.

19.

20.

21.Prototypecardisplayspace 22.Atriumcarexhibitionledges 23.Interactivecarassemblyplatform 24.Eventdisplayspace 25. Presentation+eventstheatre 26.Externalbridgepassage 27.Photovolticatriumrooflight 28.Biodiversityupliftgreenroof 1 3 2 14 15 22 23 12 13 16 10 4 17 18 25 26 28 27 24 6 5 11 19 20 21 8 7 9 BB BB

Steppedpromenadeandseating

FormulaEcoursetrack

Stationpierandinternalcarparking

Plantedbridgepassagetoentrance 5.Viaductpiercolumns 6.Steppedpromenadeandspectating

Primarystructurecolumns 8.Primaryentrytobuilding 9.Carexhibitplatforms 10.Stationconcourse+kioskspaces 11.Stationcarexhibitplatforms 12.Atriumlobbyreception 13.BritishLeylandheritageexhibition

Designhub+prototyping

SECTION BB Plans+Sections N 1:200 1m 2m 10m 2 1 4 6 5 11 10 15 16 17 18 14 12 19 20 9 13 3 7 8 Key 1. FormulaEcoursetrack 2.Plantedbridgepassagetoentrance 3.Railwayviaduct 4.Viaductpiercolumns 5.Stationconcourse+kioskspaces 6.Stationconcourseentrytobuilding 7.Carexhibitplatforms 8.Stationplatforms 9.Cardisplaybalcony 10.Customcardeliveryviaconveyor 11.BritishLeylandheritageexhibition 12.Atrium+platformexhibits 13.Atriumcarexhibitionledges 14.Customcarcustomerdesignplatforms 15.Interactivecarassemblycustomisation 16.Ceilingcarconveyorrailingsystem 17.VR/ARexhibits 18.Openingconveyorpassagedoors 19.Photovolticatriumrooflight 20.Biodiversityupliftgreenroof AA AA

ConcludingDesignProposal FinalDrawings

08

SITE FinalDrawings

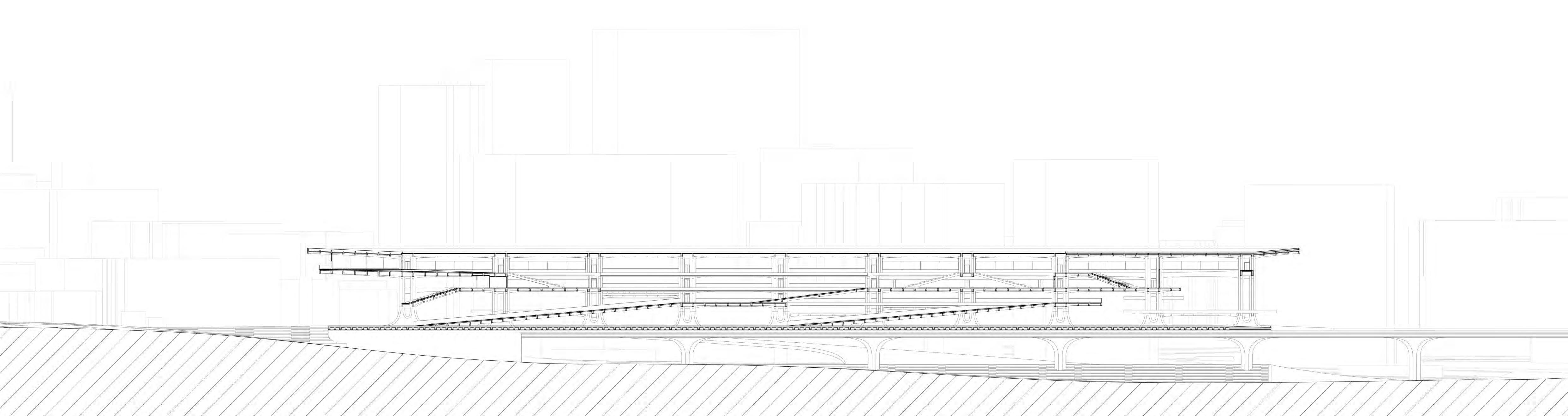

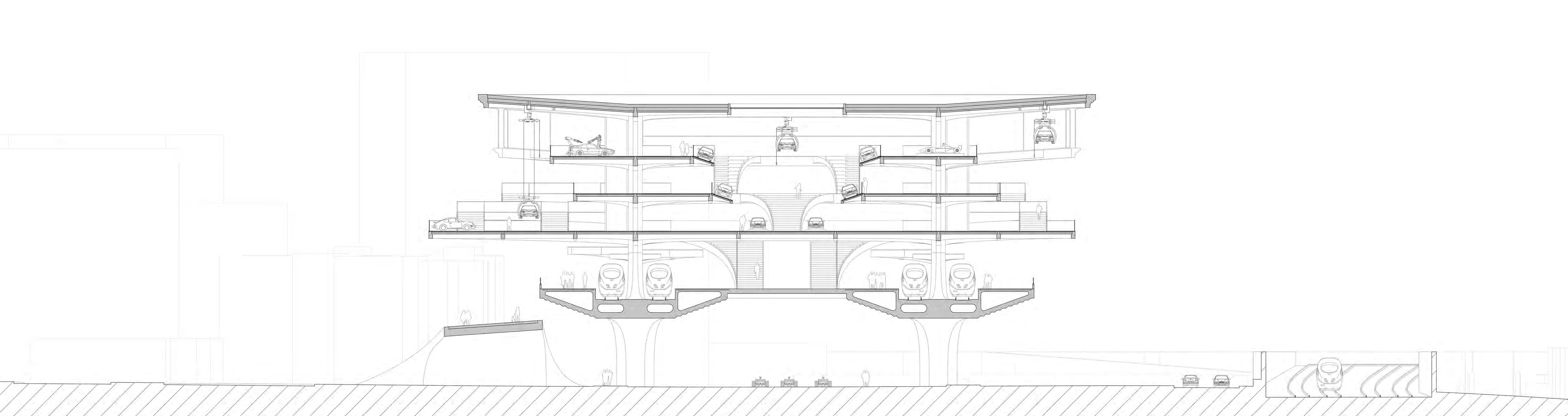

SECTION FinalDrawings

SECTION Drawings

APPROACH FinalDrawings

APPROACH Drawings

ENTRANCE FinalDrawings

ENTRANCE Drawings

ATRIUM FinalDrawings

ATRIUM Drawings

CONCOURSE FinalDrawings

CONCOURSE Drawings

STATION FinalDrawings

STATION Drawings

CIRCULATION FinalDrawings

CIRCULATION Drawings

TERRACES FinalDrawings

TERRACES Drawings

PARKSIDE FinalDrawings

PARKSIDE Drawings

GATEWAY FinalDrawings

GATEWAY Drawings

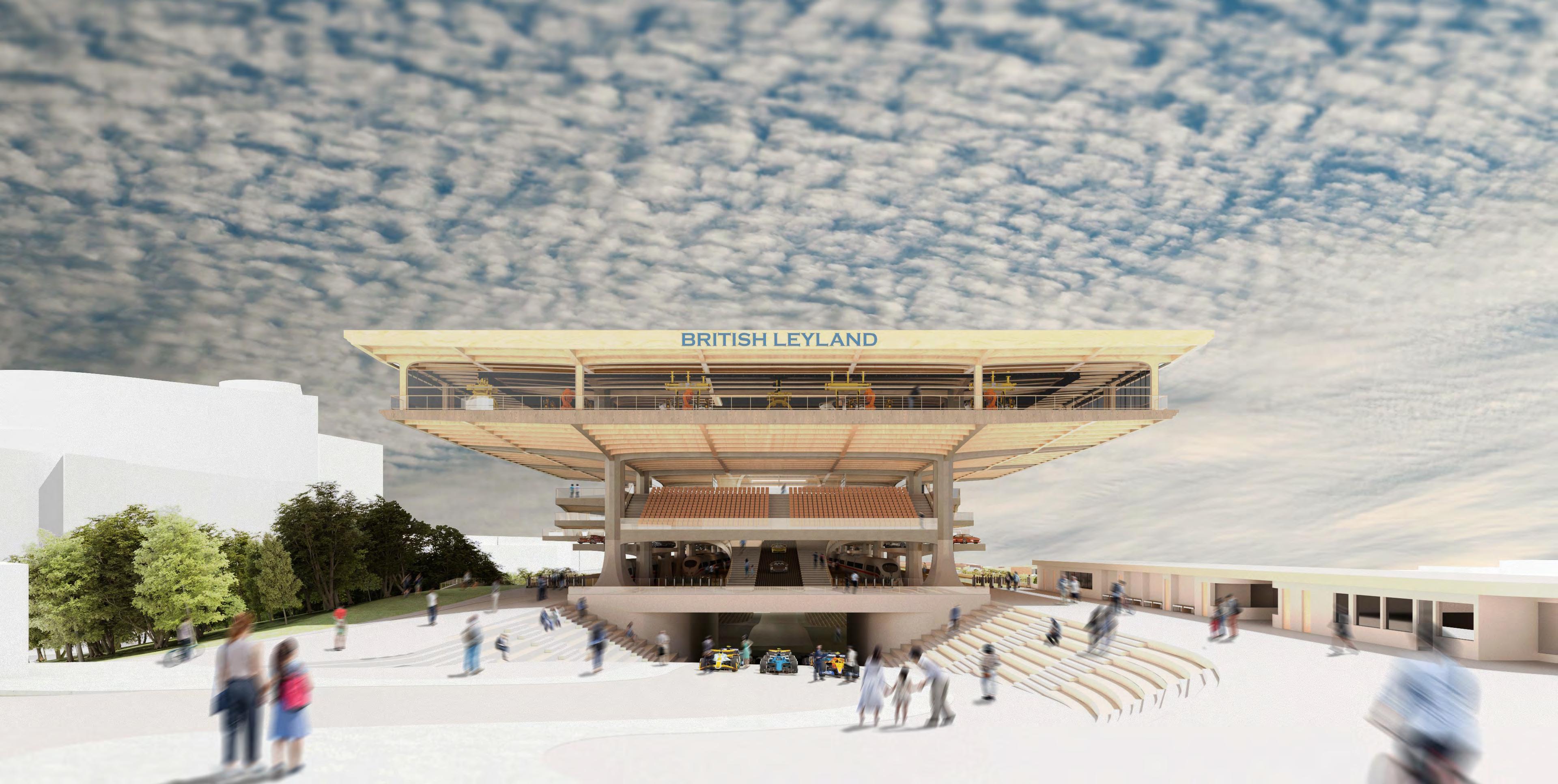

BRITISH LEYLAND FinalDrawings

LEYLAND Drawings

All work produced by Unit 14 Unit book design by Charlie Harriswww.bartlett.ucl.ac.uk/architecture

Copyright 2021 The Bartlett School of Architecture, UCL All rights reserved.

No part of this publication may be reproduced or transmited in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage and retreival system without permission in writing from the publisher.

-

@unit14_ucl UNIT

CRAFTED HORIZONS 2024

At the center of Unit 14’s academic exploration lies Buckminster Fuller’s ideal of the ‘The Comprehensive Designer’, a master-builder that follows Renaissance principles and a holistic approach. Fuller referred to this ideal of the designer as somebody who is capable of comprehending the ‘integrateable significance’ of specialised findings and is able to realise and coordinate the commonwealth potentials of these discoveries while not disappearing into a career of expertise. Like Fuller, we are opportunists in search of new ideas and their benefits via architectural synthesis. As such Unit 14 is a test bed for exploration and innovation, examining the role of the architect in an environment of continuous change. We are in search of the new, leveraging technologies, workflows and modes of production seen in disciplines outside our own. We test ideas systematically by means of digital as well as physical drawings, models and prototypes. Our work evolves around technological speculation with a research-driven core, generating momentum through astute synthesis. Our propositions are ultimately made through the design of buildings and through the in-depth consideration of structural formation and tectonic. This, coupled with a strong research ethos, will generate new and unprecedented, one day viable and spectacular proposals. They will be beautiful because of their intelligence - extraordinary findings and the artful integration of those into architecture.

The focus of this year’s work evolves around the notion of ‘Crafted Horizons’. The term aims to highlight the architect’s fundamental agency and core competency of the profession to anticipate the future as the result of the highest degree of synthesis of the observed underlying principles. Constructional logic, spatial innovation, typological organisation, environmental and structural performance are all negotiated in a highly iterative process driven by intense architectural investigation. Through the deep understanding of constructional principles, we will generate highly developed architectural systems of unencountered intensity where spatial organisation arises as a result of sets of mutual interactions. Observation as well as re-examination of past and contemporary civilisatory developments will enable us to project near future scenarios and position ourselves as avant-garde in the process of designing a comprehensive vision for the forthcoming. The projects will take shape as research based, imaginative architectural visions driven by speculation.

Thanks to: ALA, Boele Architects, Daab Design, DaeWha Kang Design DKFS, Heatherwick, Knippershelbig, NK3, RSHP, Seth Stein Architects, ZHA, Expedition Engineering.

UNIT 14 @unit14_ucl

All work produced by Unit 14 Unit book design by Charlie Harriswww.bartlett.ucl.ac.uk/architecture Copyright 2021 The Bartlett School of Architecture, UCL All rights reserved.No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage and retreival system without permission in writing from the publisher.