1 minute read

Kentucky Total Premiums Perspective

To provide perspective, in the table below is comparative data on Kentucky P&C premiums; and how Kentucky premiums compare to the United States in total, including some common groupings of lines of business, on a per capita basis. Also provided are the smallest/lowest state, and largest/ highest state for either total premiums, or per capita premiums.

Each of these groupings are organized as follows:

Advertisement

• Total (All Lines) includes premiums for all 32 P&C lines of business;

• Personal Lines includes All Private Passenger Auto, and Homeowners Multi-Peril;

• Commercial Lines includes All Commercial Auto, Commercial Multi-Peril, Other Liability (Claims- Made), Other Liability (Occurrence), Products Liability, and Workers’ Compensation; and

• Agricultural Lines includes Farmowners Multi-Peril, Multi-Peril Crop, and Private Crop,

In each case, the basis of the per capital comparative premium uses the most recent population estimate from the U.S. Census.

Source: © A.M. Best Company — Used by permission and U.S. Census Bureau, Population Division and Annual Estimates of Resident Population (Release Date: December 2022)

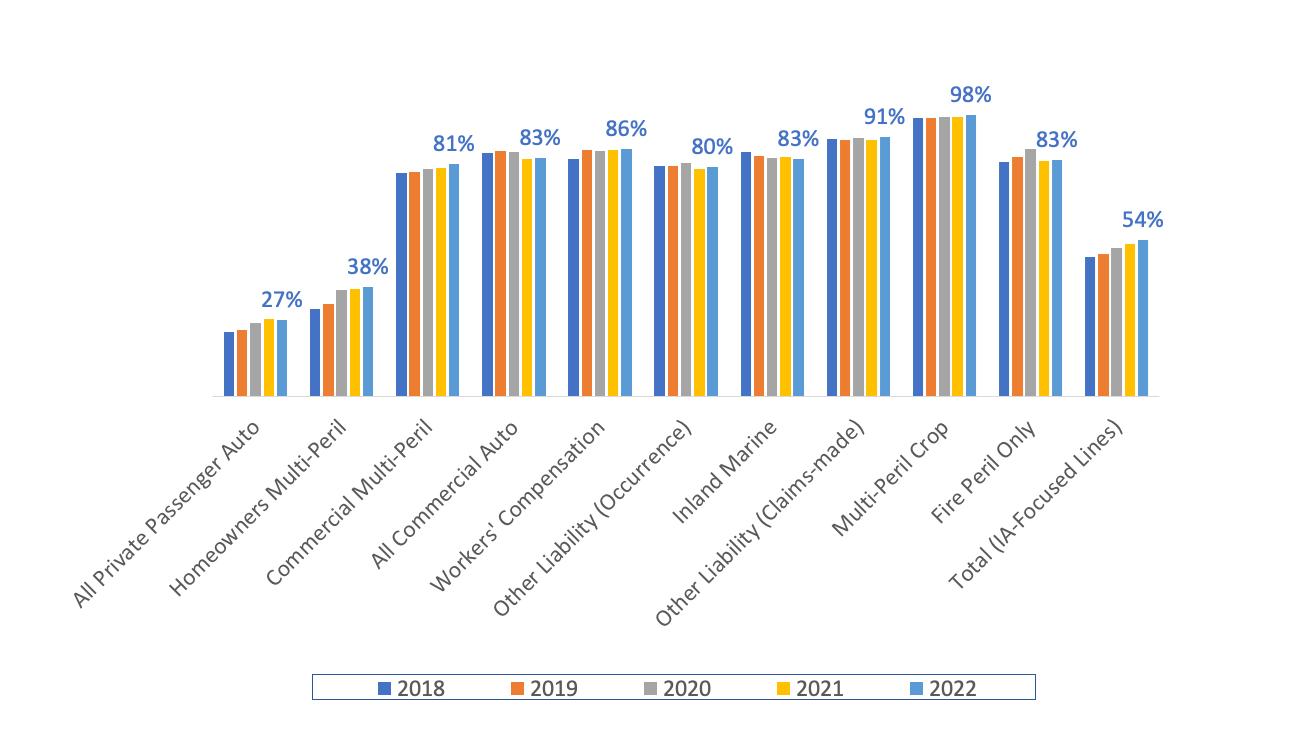

Kentucky Top 10 Independent Agent Lines of Business

Source: © A.M. Best Company — Used by Permission

The below pie charts show which lines of business are the most important to independent agents, based on direct written premiums. The top 10 lines of business are shown in each pie chart, with premiums from all other lines of business combined in the “All Other” pie section.

Data for Kentucky is used in the top two pie charts, with the lines of business ordered by rank order of premiums through independent agents in Kentucky. The left pie chart includes premiums only through independent agents. The right pie chart adds all premiums from all distribution styles included in each pie section. For comparison, data for the United States is used for the second two pie charts. The rank-order for the United States pie charts is based on premiums through independent agents in all of the United States.

For further information Appendix #2: Distribution Style Classifications gives the reader a detailed explanation of the classification of insurers into distribution styles, based on insurer reported marketing types. Also included in Appendix #2 is additional data on premiums by line of business for each distribution style, as well as the Top 10 insurers for each distribution style.