ISSUE 1 / 2023 Start By Making Everybody A Salesperson Build Better Relationships How To Make Marketing More Magnificent Consumers Using ATMs More Than Ever A PUBLICATION OF AMERICAN BUSINESS MEDIA Recycle Those Benjamins Mergers Need An Overhaul Lisa Oliver, president and CEO The Cooperative Bank of Cape Cod

advantagediscover the NES Find your design partner to achieve your long-term goals. advantage discover the NES bank design project management branding equipment new england new york 508.339.6600 nes-group.com What makes us different? In-house capabilities to imagine, design, and deliver your project. Let us build off your goals and help you realize your environments' creative potential.

ISSUE 1 / 2023 Start By Making Everybody A Salesperson Build Better Relationships How To Make Marketing More Magnificent Consumers Using ATMs More Than Ever A PUBLICATION OF AMERICAN BUSINESS MEDIA Recycle Those Benjamins Mergers Need An Overhaul Lisa Oliver, president and CEO The Cooperative Bank of Cape Cod

Discover Where Your Competitors Stand In The Mortgage Market

Adapting to today’s dynamic mortgage market has changed the way we analyze trends and track competitors. Luckily, we have the tools you need to determine your competitors’ market share and see how individual loan originators are performing in their market.

Mortgage MarketShare Module

Our Mortgage MarketShare Module provides real-time market insights on all lenders, helping you easily benchmark your company’s market share, identify new and emerging markets, and measure your sales performance against your competition.

Loan Originator Module

Our Loan Originator Module provides you with access to the largest and most comprehensive loan originator database in the country. Take advantage of this access to identify top-producing loan officers, verify production, and monitor competitors.

GET A FREE MORTGAGE COMPETITOR ANALYSIS

BENEFITS

• Monitor Residential and Commercial Lending

• Measure Sales Performance and Market Activity

• Identify High-Performing Competitors

• Uncover Emerging Markets and New Opportunities

• Pinpoint Top Loan Officers for Recruitment

• Identify and Verify Loan Originator Performance

• Measure Loan Activity Against Competition

• Highlight Success for Market Positioning Visit

To show you just how powerful our modules are, we’re offering a free customized mortgage competitor analysis. Simply visit www.thewarrengroup.com/competitor-analysis and provide us with a few details. You’ll receive an updated 2021 vs. 2022 Quarterly Mortgage MarketShare Report at the company level paired with a Loan Originator Report highlighting top LOs and individual performance.

NEED MORE DATA?

Inquire about our NMLS Data Licensing and LO Contact Database options.

Questions? Call 617.896.5331 or email datasolutions@thewarrengroup.com.

www.thewarrengroup.com to learn more today!

Agencies Issue Joint Statement On Liquidity Risks Resulting From Crypto-Asset Market Vulnerabilities

Statement reminds banking organizations to apply existing risk management principles

Federal bank regulatory agencies issued a joint statement highlighting liquidity risks to banking organizations associated with certain sources of funding from crypto-asset-related entities and some effective practices to manage those risks.

Recent events in the crypto-asset sector have underscored the potential heightened liquidity risks presented by certain sources of funding from crypto-asset-related entities. The joint statement highlights key liquidity risks and some effective practices to monitor and appropriately manage those risks. The statement reminds banking organizations to apply existing risk management principles; it does not create new risk management principles.

The statement reminds banking organizations to apply existing risk management principles; it does not create new risk management principles. Banking organizations are neither prohibited nor discouraged from providing banking services to customers of any specific class or type, as permitted by law or regulation.

Deposits placed by a crypto-asset-related entity that are for the benefit of the crypto-asset-related entity’s customers (end customers).

The stability of such deposits may be driven by the behavior of the end customer or crypto-asset sector dynamics, and not solely by the cryptoasset-related entity itself, which is the banking organization’s direct counterparty. The stability of the deposits may be influenced by, for example, periods of stress, market volatility, and related vulnerabilities in the crypto-asset sector, which may or may not be specific to the crypto-asset-related entity. Such deposits can be susceptible to large and rapid inflows as well as outflows, when end customers react to crypto-asset-sectorrelated market events, media reports, and uncertainty. This uncertainty and resulting deposit volatility can be exacerbated by end customer confusion related to inaccurate or misleading representations of deposit insurance by a crypto-asset related entity.

More broadly, when a banking organization’s deposit funding base is concentrated in crypto-asset-related entities that are highly interconnected or share similar risk profiles, deposit fluctuations may also be correlated, and liquidity risk therefore may be further heightened. Banking organizations are neither prohibited nor discouraged from providing banking services to customers of any specific class or type, as permitted by law or regulation.

CEO, PUBLISHER, EDITOR-IN-CHIEF

Vincent M. Valvo vvalvo@ambizmedia.com

ASSOCIATE PUBLISHER

Beverly Bolnick bbolnick@ambizmedia.com

EDITORIAL DIRECTOR

Christine Stuart

EDITOR

David Krechevsky

SENIOR EDITOR

Keith Griffin

HEAD OF MULTIMEDIA

Mike Savino

STAFF WRITERS

Katie Jensen, Steven Goode, Sarah Wolak

SPECIAL SECTIONS EDITOR

Gary Rogo

DIRECTOR OF STRATEGIC GROWTH

Alison Valvo

CHIEF MARKETING OFFICER

Steven Winokur

DESIGN MANAGER

Meghan Hogan

GRAPHIC DESIGN MANAGERS

Christopher Wallace, Stacy Murray

DIRECTOR OF EVENTS

Navindra Persaud

UX DESIGN DIRECTOR

William Valvo

HEAD OF CUSTOMER OUTREACH AND ENGAGEMENT

Andrew Berman

MULTIMEDIA SPECIALISTS

Tigi Kuttamperoor, Matthew Mullins, Angelo Scalise

PROJECT MANAGER

Julie Carmichael

MARKETING & EVENTS ASSOCIATE

Melissa Pianin

ONLINE ENGAGEMENT SPECIALIST

Kristie Woods-Lindig

ADVERTISING ASSOCIATES

Nicole Coughlin, Nichole Cakirca

BANKING NORTHEAST MAGAZINE | 3 OUR MISSION Banking Northeast magazine is dedicated to providing quality informational/educational content that betters the banking process at every step. The content is oriented to help professionals progress their understanding of the banking business and develop their skills at improving efficiency and profitability at all levels.

© 2023 American Business Media LLC All rights reserved. Banking Northeast magazine is a trademark of American Business Media LLC. No part of this publication may be reproduced in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage and retrieval system, without written permission from the publisher. Advertising, editorial and production inquiries should be directed to: American Business Media | LLC 88 Hopmeadow Street | Simsbury, CT 06089 | Phone: (860) 719-1991 | info@ambizmedia.com

www.ambizmedia.com

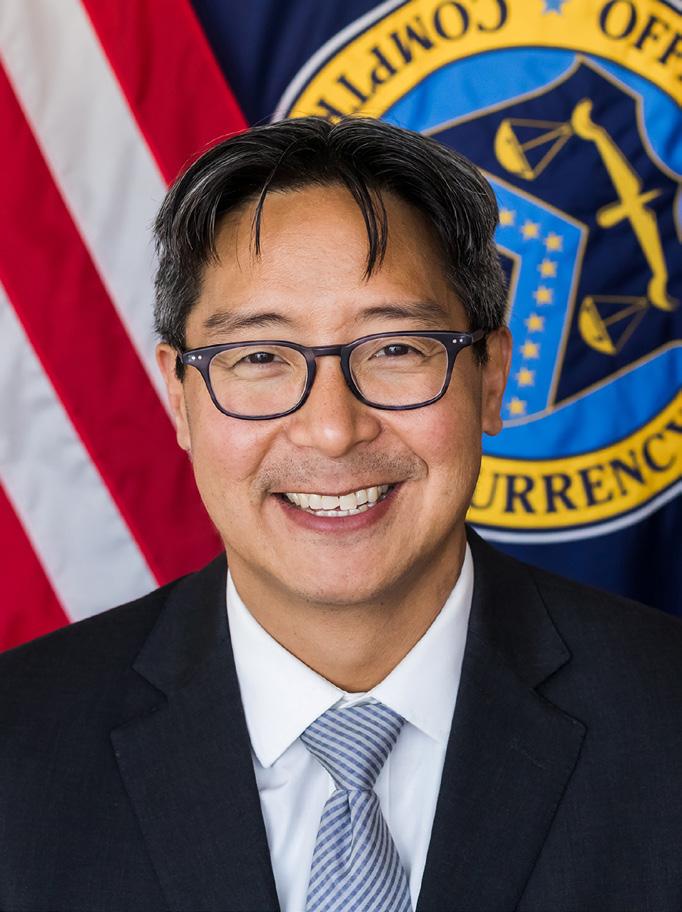

Framework For Analyzing Bank Mergers Needs Updating

Acting OCC head says too much data is outdated

BY MICHAEL J. HSU, SPECIAL TO BANKING NORTHEAST MAGAZINE

I’d like to address two questions: first, why it’s important to have a discussion now about bank mergers, and second, why I believe this symposium can help to advance that discussion.

On the first question, bank mergers have received significant attention during my time as acting comptroller. There is a robust ongoing debate about the effects of bank mergers on competition, on U.S. communities, and on financial stability. At the same time, many experts have raised questions about the ongoing suitability of the current bank merger standards at a time of intense technological and societal change.

As I’ve said before, the framework for analyzing bank mergers needs updating. Without enhancements, there is an increased risk of approving mergers that diminish competition, hurt communities, or present systemic risks. By the same token, a moratorium on mergers would lock in the status quo and inhibit growth and improvements that could help communities and increase competition.

We need to build a better mousetrap so that healthy mergers get approved while unhealthy mergers get rejected. Importantly, this mousetrap needs to be not only theoretically sound and consistent with our values, but also capable of implementation within the statutory criteria for merger review.

Consider, for instance, the competition prong of the merger review framework.

Michael J. Hsu

Bank regulators currently use the Herfindahl–Hirschman Index, or HHI, to assess market concentration before and after mergers. The most recent Bank Merger Competitive Review guidelines from the Department of Justice establish a safe harbor for mergers resulting in HHI levels below 1800 points for a given market with a rise of less than 200 points.

This approach has a number of positive attributes. HHI is a transparent, empirically proven, efficient, and easily understood measure of concentration. The index is objective, based on a consistent

measure of market presence based on deposit share. Furthermore, the use of HHI is efficient, in that it is simple to compute and provides ex ante certainty for merger participants.

Nevertheless, in some ways, HHI might have become less relevant since the bank merger guidelines were last updated in 1995. For example, the growth in online and mobile banking and rise of nonbank competitors may have made HHI - which is based only on deposits - a less effective predictor of competition across product lines. This is so because a bank’s deposit base may have become less probative of its offering of other banking products. In addition, the size of the relevant markets for these products may have expanded exponentially with the rise of online banking products and services, while nonbank competitors have grown to an extent unimagined in 1995. I expect a discussion of the use of deposit share to define markets will be one of many topics our panelists will discuss today.

Another key topic for today will be financial stability, which became a mandatory component of merger analysis following the enactment of the 2010 Dodd-Frank Wall Street Reform and Consumer Protection Act. From my perspective, the current framework for assessing the financial stability risks of bank mergers bears examining.

As I discussed in a speech last year at the Wharton School of the University of Pennsylvania, there is a resolvability gap for large regional banks in that our

4 | BANKING NORTHEAST MAGAZINE

OPINION

resolution tools may not be up to the task.

I look forward to hearing perspectives on this issue and potential practical solutions from our panel on financial stability.

Also crucial to merger review is the analysis of a merger’s effects on the convenience and needs of communities served, from branch closures to changes in product offerings and terms.

An assessment of each bank’s Community Reinvestment Act (CRA) performance is of course a critical part of this analysis, and I believe CRA performance and ratings are only a starting point.

The OCC has heard many times from bankers and community groups on the value of public feedback and community

reinvestment plans in the regulatory assessment of bank mergers. Our panel on convenience and needs will discuss the many ways that we may refine bank merger analysis to improve banking services in communities across the nation.

On the second question of why this symposium can help advance the discussion, in my experience, sometimes it takes in-person exchanges of ideas to spur us to action.

Michael J. Hsu, the acting comptroller of the currency, made these remarks at the opening of the OCC Bank Merger Symposium in February.

BANKING NORTHEAST MAGAZINE | 5

We need to build a better mousetrap so that healthy mergers get approved while unhealthy mergers get rejected.

&QA

Banking Northeast Magazine caught up with Jason Wolf, senior manager, advisory services, Diebold Nixdorf, and Matt Dunlap, director, banking product SMEs, Americas, Diebold Nixdorf, after their talk at BankWorld 2023 on cash recycling.

Their seminar focused on how banks and CUs are seeing more cashdeposit volume at the ATM than ever before. With notes-in reaching the tipping point, there is an urgency within the industry to understand how to implement a recycling program and how to size/measure the expected benefits. With cash servicing comprising 20%-30% of the ATM’s average operating expense, recycling-enabled ATMs will be a crucial component of controlling future costs that are expected to increase over the next five years.

This presentation discussed the key steps in determining how to prioritize the deployment of recycling across a financial institution’s network, estimated cost savings associated with servicing a recycling network, the hidden benefits of offering denomination selection options and what institutions must do to prepare for a recycling future.

Here is what Wolf and Dunlap had to say during their post-session interview with Banking Northeast Magaine Senior Editor Keith Griffin.

Cash Still King With Consumers Banks,

CUs need to explore trends in recycling to save money

BY KEITH GRIFFIN, SENIOR EDITOR, BANKING NORTHEAST MAGAZINE

Q. What are some of the consumer transaction trends you're seeing in cash recycling? Are more customers avoiding bank tellers for example?

WOLF: I wouldn't say they're necessarily avoiding tellers. In some instances, I think after COVID and the lockdown, people got used to doing transactions at an automated or self-service device. So, lobbies weren't open. They were forced to go through drivethroughs or access ATMs. So they got a little more comfortable doing things not face-toface. I think also due to some of the staffing shortages that we observed during COVID, there just weren't enough people to fill the teller position. So, you have fewer people in the branch and wait times get longer, so people start avoiding that situation and then change their behavior to utilize a channel that might be a little more convenient.

Q. Are you seeing that among more of a certain demographic? Is it younger people, older people? Who's getting more impatient waiting in line?

WOLF: It might be concentrated within older segments because they are typically heavier branch users. So once that teller capacity is removed from those branches, they're used to a certain level of service, those times go up, they might seek out other means to make that transaction.

I think younger folks have been pretty good at adopting some of the other self-service channels, so doing things at the ATMs, mobile check deposit, they're a little more open to doing these transactions and were probably already doing them pre-pandemic.

Q. Why does the utility of cash remain strong?

WOLF: It definitely remains strong, but within certain segments and certain payment types. For instance, we see strong cash usage within in-person small dollar transactions. What that means is I go to a coffee shop and I'm going to buy a $5 latte. I'm going to pay for it with cash. So we still see cash in that sense remains strong. It also remains strong for different segments, so older segments typically prefer to operate in cash. So those folks that are maybe 65 and older. And then we also see lower-income groups more reliant on cash.

Q. Why is cash more important to the lower household income groups?

WOLF: Some of those folks might be considered underbanked. So, they're maybe not utilizing a typical bank. They also might be operating in more cash-intensive businesses where they're getting paid in cash, and there's also maybe a little bit of mistrust within the banking system within that lower-income segment. Another

6 | BANKING NORTHEAST MAGAZINE

TECHNOLOGY

thing we observed is cash can be utilized for budgeting purposes. So, you know, setting up an envelope for groceries, for the gas bill. So it allows them to be able to control what they're spending a little bit easier than, you know, just swiping everything on a debit card.

Q. Why are banks in credit unions seeing more cash deposit volume? It seems almost against the trend.

DUNLAP: We’re seeing a pretty steady trend of deposited notes being more and more at the ATM level. Many people are more comfortable with depositing notes at a self-service system like an ATM. You think about 20 years ago, people were all going to the teller line to do their deposits, but we introduced ATMs. They could take envelopes at some point. That was probably 15, 20 years ago. People started to put deposits in envelopes, and then the technology of cash deposits really evolved over the last 10 to 15 years to be able to take notes directly in at the ATM and scan them and validate them. And people were becoming more comfortable with that. That's one of the reasons why more and more people want to deposit those notes at the ATM. They also get credit for those notes a little quicker than they would at night drop. That's all playing into that trend as well.

Q. What are some of the consumer transaction trends?

DUNLAP: So, you just mentioned the deposit volumes are coming up. That's a trend we're keeping a close eye on, especially when you're thinking about the next phase of technology when it comes to cash recycling, taking those

down week per week, but we're seeing some shift in what's going on with those transactions.

Q. Just to follow up a little bit on withdrawals versus deposits. There's been changes in both of those, correct?

DUNLAP: Right. One thing we monitor is the cash into out ratio. So that's the number of notes coming into the ATM versus what's being dispensed. And 2010, I think it was about 20% of cash coming into those types of ATMs was available for dispense. So, 20% of those notes were deposit notes. Now it's closer to 30 to 40%. We're seeing a heavy trend of more notes coming and, and less notes coming out. That trend and ratio is coming up as well.

Q. What are some of the global trends you're seeing that might be coming to the United States?

DUNLAP: Globally there's really a lot more focus on cash recycling. Some of the major markets in Asia and Europe and even South America have been doing cash recycling for some time. They're already leveraging the benefits of using those deposited notes to dispense those notes back out and also reduce that cycle time between, uh, visits to go on, either add cash or remove cash. So, those are trends we're seeing globally. Obviously, there's different markets that have different requirements, so we're using those lessons learned of those markets and applying them here to the U.S. market that's getting ready for it.

Q. Why should banks and credit unions get behind cash recycling? What are the advantages to them?

notes and recycling them back out. Another trend we're seeing is check transactions. They're kind of fading away, although they're still popular in the United States, one of the bigger markets for usage of checks. We're also seeing a trend where cash dispense transactions are declining a bit as well. So the transactions are coming

DUNLAP: There are two major advantages. One is the reduction of cash and transit cycles or replenishment cycles, you know, could be done by the cash transit companies or with branch tellers. The number of times they have to touch the machines will come down with cash recycling. That's a major one. It's just less visits, and less cost if you're using cash transit companies. The other major one is you don't have to touch the unit as often. So, as we often see in this industry, failures happen when people are involved. They open things up, they close them wrong, or they put the notes in wrong. When you use cash recycling, you're out there touching the unit less. It really improves the reliability of that equipment (and) extends the life cycle of that equipment because it's just less workload on that entire ecosystem of ATMs. Also, if you're reducing the cycle times, you’re going to save money with the operational cost to keep that unit running.

BANKING NORTHEAST MAGAZINE | 7

“If you're reducing the cycle times, you’re going to save money with the operational cost to keep that unit running.”

–Matt Dunlap

Matt Dunlap, director

Jason Wolf, senior manager

Relationship Banking Is Key To Success

Focusing just on the bottom line guarantees failure

BY LISA J. OLIVER, SPECIAL TO BANKING NORTHEAST

COVER STORY 8 | BANKING

MAGAZINE

NORTHEAST

Lisa Oliver, president and CEO of The Cooperative Bank of Cape Cod (The Coop), speaks to banking executives at American Business Media's 2022 Women in Banking conference held in Newport, Rhode Island. Photo by Mary Quinn; A Bear With Thumbs LLC

Lisa Oliver, president and CEO of The Cooperative Bank of Cape Cod (The Coop), speaks to banking executives at American Business Media's 2022 Women in Banking conference held in Newport, Rhode Island. Photo by Mary Quinn; A Bear With Thumbs LLC

ur personal uniqueness is the very basis of what makes relationship banking so necessary. We're all individuals with individual needs, goals, and dreams. We need to think of our customers the same way; after all they’re individuals too. And in a world that changes daily, we need to continuously reevaluate how we do business with each other. That's true whether you're a banker, a chef, or a small business owner.

Despite the myriad of incredible advancements in technology, particularly artificial intelligence, it's the human connections that are the most critical to driving our economy forward. The title of my talk is “Be Real, How Strong Relationships Drive Sales Success.”

But before I dig into this further though, I have to issue a disclaimer up front. Although I've been a salesperson my entire life, I never realized how many people consider the word sales or selling to be the Voldemort of banking. Shout out to all you Harry Potter fans, the thing that shall not be spoken, especially in the community banking world.

The only way I can understand why this may be is to believe that people have been trained to push product, create volume, hit sales goals, call targets, and it makes everybody feel a little dirty, devalued, a gun for hire. I challenge this perception. There are many things that go into the art of selling. And if I can give you more of a sense of ease as we get going, know that I don't like to sell, but I like to solve problems.

When a customer understands what you can bring to the table, not just in terms of available products and services, but as a relationship manager, someone who's always thinking about them, you're almost guaranteed to see a higher return on that relationship. Working hard to make it work will yield better results and we need to be go-givers, not go-getters.

If you're wearing a brand on a name tag

Oor your paycheck has a company name on it, every employee is a salesperson because it could happen over a backyard barbecue, it could be at an event. You are always representing whom you work with. We should always be asking the customer what they need and what they want by connecting the dots to past experiences with them. Or if they're a prospect asking questions that have to do with our knowledge of their industry or if we don't have that our research into their history.

BETTER QUESTIONS FOR BETTER RESULTS

Make an effort every time asking better questions helps us better understand the goals of our customers, which means we can deliver the best possible service. Make it your goal to become a trusted problem solver, not a commodity, when asked who they rely on for service. Before a client makes a decision, I want them to make sure they call me. We often refer to this kind of customer-centric, proactive problem-solving approach as high touch. An effective tool to help you on this journey is a relationship review.

How do we differentiate ourselves in a fragmented overbanked market? We all need to listen first, then be well-armed with the knowledge, training tools, and resources to effectively communicate solutions to our clients and prospects. And we all recognize that we're not the only ones providing financial advice, right? Remember the thing called the Internet or the Google, as my mother calls it? Any guesses as to what percentage of a customer's journey is done digitally? Anybody have an idea? 67%. That means before a customer ever says a single word to you, they've likely already been exposed to products they may have already.

They may already think they know which product they're going to pursue and maybe the product they're pursuing is the best one for them. But what if it's not? What if they're thinking only about short-term needs without understanding or considering longterm impacts? What if their needs of today are going to be different from their needs of tomorrow? Acknowledge when they're right, when they have the right solution. And offer facts to teach them about other alternatives. Expecting nothing in return.

Did you know that according to one report I read, 42% of salespeople feel as

10 | BANKING NORTHEAST MAGAZINE

“Long-term relational business development where clients are apt to refer you to others is the ideal environment.”

–Lisa J. Oliver

though they don't have enough information before making a call to a customer or prospects? Now if the call is missing information, then it's OK. But what if the team member is calling to offer solutions to the customer? How do you think that conversation is going to go if they don't feel prepared? Probably not.

Well, in fact, the same report will also tell you 85% of prospects and customers are dissatisfied with their phone experience. It's not because the salesperson is rude, or maybe they are and that's a whole other conversation. It's likely because they don't receive regular coaching through one-onones and pre-call planning before they actually get out there in order to achieve a high-touch, solution-focused relationship.

Research shows that for every dollar invested in sales training, you can expect $29 in incremental revenue. Seems like a pretty good investment to me.

ADVISORS, NOT SALESPEOPLE

If we can work with our teams to better understand relationship banking to become advisors, not salespeople, to become expert service providers, then the production will take care of itself. I promise you that much like we want our teams to focus on the individual goals of customers, we too should be focused on the individual professional and personal gains of our team members. What is it that your team members want to be better at doing? How can we help them reach those goals? What plans can we put in place to ensure they remain focused and on track to be successful? Why do they come to work each day?

It's important to understand the numbers and it's important to get to the numbers, but getting to the numbers for number sake is not the way to do it. We have to be hyperfocused on the activity and the value of delivering more to our clients. If we don't and we only focus on the numbers, it'll [undo] the foundation or the culture on which we're trying to better serve our clients.

So going back to the hiring process for a moment, I threw out a question earlier, but one of the questions you should ask candidates when you're hiring is why they're interested in the bank. Most are probably going to say something like, I want to help the bank become more successful. Some might say, I'd like to take my income to the

next level, but you want the ones who say, “I want to help solve problems. I'm looking to help the bank build stronger relationships with clients.” Follow up by asking for an example. Use your behavior-based interview tactics to ask for an example of a customer that they worked with whom they helped achieve their dreams.

If they're good salespeople, they're going to get that question and they're going to be able to answer it for you. And when it comes to coaching, here are five things to consider. I can't expect my teams to do what I'm not willing to do or try to do or try and fail to do. Demonstrate good and bad conversations. Focus on weak areas and exhibit better ways to perform in certain situations. Make sure you give and get clear directions and instructions. Role play. You're better when you practice as your team works its way through the learning process, which never ends by the way. Let them put their new knowledge to the test.

I remind them that I'm not going to save them as a coach. You can't save the salesperson. You have to let them try and fail and pick them up.

MOVING FORWARD

What is the plan of action moving forward? What successes can be built upon? Where are their knowledge gaps? Presentation challenges? How can more teamwork help to make the lives of our sales teams and, thus our clients more productive and with better outcomes?

If you build strong relationships, your customers will gladly refer others to you. The strongest relationships are your best ambassadors who will tell their connections to call you before they are even asked.

Our goal when networking is to build a relationship through common interests. If we're all bankers in a room, what else is different? Talk about dogs. Talk about wine. Talk about sailing. Talk about sports. Talk about vacations. Be of interest. Be interested in what others are doing and determine through that process. And interesting facts. Yes, matching your expertise with their needs. It won't happen in one encounter. Think about how you could improve that introductory comment to be an interested and interesting person to nurture these relationships.

As you build your network, you'll be less reliant on yourself sourcing business and

BANKING NORTHEAST MAGAZINE | 11

“We should always be asking the customer what they need and what they want by connecting the dots to past experiences with them.”

–Lisa J. Oliver

your network will do it for you. You go from being someone who has to cold call and drive new business to a network person whose phone just rings.

How do we know when we've succeeded in relationship building? We get referred to others. We're on the list of most trusted advisors. The biggest indicator of developing a trusted relationship is that we're not a commodity. Said another way, we're not the lowest price. We provide value through ideas and solution and speed and knowing our customer inside and out. We're invaluable and therefore we're worth 15 basis points, 25 basis points, maybe a whole percent more in pricing for the value received.

Creating this culture is rooted in our ability to avoid a short-term transactional relationship and build on a long-term strategic engagement. Remember the goal is to be a trusted advisor who knows and anticipates the customer's needs and can be thinking proactively on their behalf is what we should be aiming for. It takes time to get there. But if you invest the time and get to know the customer, the relationship will continue to pay dividends for a long time. Short-term selling may result in higher quantitative sales metrics up front, but it'll come with lower pricing and lower revenue.

Long-term relational business development where clients are apt to refer you to

others is the ideal environment. And one additional thought: don't desperation sell. Everybody else is making deals. I have to go find a deal. OK, I'm going to just go say I'll get the lowest rate. And you come back to the bank and you beg for the lowest rate and you bring this client in.

Guess what? In a heartbeat that client leaves for the next lowest rate and you haven't developed a relationship. I had a boss say to me once, "The reason you win a deal is the reason you're going to lose a deal." And if you want a deal, because you are the lowest rate, as soon as there's a lower rate, that person's gone. If you win a deal because of a relationship and you add value and you get the ultimate, which is that person, that client pays more to bank with you even a little bit and doesn't go with the lowest rate. That client will stay with you because you add value, not go to the next lowest rate.

Lisa J. Oliver is the president and CEO of The Cooperative Bank of Cape Cod (The Coop). She is the first female CEO in its 100year history and in 2020 was named the bank’s first chair of the board of directors. The above comes from remarks she made at the 2022 Women in Banking conference held in Newport, Rhode Island.

12 | BANKING NORTHEAST MAGAZINE

Lisa Oliver spoke at American Business Media's 2022 Women in Banking conference held in Newport, Rhode Island. Photo by Mary Quinn; A Bear With Thumbs LLC

“... if you invest the time and get to know the customer, the relationship will continue to pay dividends for a long time.”

–Lisa J. Oliver

BANKING NORTHEAST MAGAZINE | 13

Clearview FCU Names Florian First Female President

The Clearview Federal Credit Union, based in Moon Township, Pa., announced that Lisa Florian will be the first female president and CEO in its history, effective April 1. Florian's appointment to the Clearview helm follows the announcement of the departure of the current President & CEO, Ron Celaschi, who will retain the position and aid with the transition until March 32..

Florian currently serves as senior vice president, member experience, digital strategy, and marketing, a role she was promoted to in 2020. Florian has been with Clearview since 2015, holding the positions of vice president, member experience and marketing, and vice president, finance and assistant vice president, strategic research and analysis. She has over 25 years of experience in the financial services and credit union industries.

Florian is active in her community, currently serving on the West Jefferson Hills Foundation for Education Board and Thomas Jefferson High School Football Boosters Board. She has also served on numerous committees for nonprofits in the greater Pittsburgh region and spends time volunteering throughout the year.

"I am very excited and honored to be chosen by our board of directors as the next president and CEO of Clearview," Florian said. "I look forward to building on the foundation of providing financial solutions that help our members enjoy a

better life and leading Clearview to continued success and growth."

As president and CEO, Florian will focus on the brand's evolution while remaining committed to building a community and member-forward culture, increasing access through digital channels, and implementing continuous improvement through organizational leadership.

Cenlar Names Daras CEO & President

D. James “Jim” Daras has been named CEO and president of Cenlar FSB, the Ewing, N.J.-based financial institution announced.

“Jim is an accomplished and exceptional executive leader with a great deal of experience who will ensure Cenlar continues its commitment to providing high-quality service to our customers,” said Chairman of the Board Dave Applegate.

Daras has more than 40 years in the banking and mortgage banking industry. He has extensive knowledge in risk management, banking and corporate finance functions, bank restructuring, company start-ups and venture capital investing. He worked at Cenlar from 1985 to 1990, leaving his post as chief financial officer to join Dime Bancorp in New York City. Until returning to Cenlar in 2015, Daras worked with several venture capital firms investing in financial services companies, including Loan Servicing Solutions in 2007, where he served as CEO. Daras

was executive vice president and was appointed chief risk officer at Cenlar. In 2019, he moved to an advisory capacity before returning full-time to manage the company’s banking functions. He joined Cenlar full-time in 2022 as executive vice president to manage the company’s banking functions.

Last summer, Daras and Executive Vice President and Chief Operating Officer Robert “Rob” Lux were both appointed co-CEO after Chairman of the Board, President and CEO Greg Tornquist announced his retirement from Cenlar. Lux will continue in his role of COO reporting to Daras.

Patriot FCU Names Celaschi To Top Spot

Ronald Celaschi has been named as the new CEO at Patriot Federal Credit Union in Chambersburg, Pa. Celaschi will join Patriot on April 3 and succeed Brad Warner.

Warner, who has over nine years of service at Patriot, including as the credit union’s CEO since 2015, announced his intention to retire in August 2022. He has spent over 43 years in the financial services industry, including over 30 as a credit union CEO. He is assisting Celaschi in the transition.

“I want to take a moment to thank our board of directors for their many hours of hard work; but most importantly for an excellent selection,” Warner said. “Ron embraces the Servant Leadership philos-

14 | BANKING NORTHEAST MAGAZINE

ON THE MOVE

D. James “Jim” Daras Chelen Reyes

ophy and he is looking forward to beginning his new role at Patriot.”

Celaschi has more than 31 years in the credit union movement. During his career, he spent over 14 years at the Pennsylvania Credit Union Association (PCUA), where he was a senior planning consultant for members of the credit union league. He became CEO of Frick Tri-County Federal Credit Union in 2005, a post he held for three years before joining Clearview Federal Credit Union as vice president – lending. Celaschi also served as senior vice president – lending and operations before taking the helm at Clearview as president/CEO in 2018.

A graduate of Indiana University of Pennsylvania (IUP) with a Bachelor of Science degree in business administration/ finance, Celaschi completed his Master’s degree in business administration from California University of Pennsylvania. He and his wife, Tricia, have two children.

Rockland Trust Company, Independent Bank Corp. Appoint Tengel To CEO

Rockland Trust Company and its bank holding company parent Independent Bank Corp. announced the appointment of Jeffrey J. Tengel as the successor to current CEO Christopher Oddleifson.

The Massachusetts financial institution said Oddleifson has served as the bank’s CEO since 2003. Under his leadership, Rockland Trust has grown total assets

from just over $2 billion to nearly $20 billion and expanded from its southeastern Massachusetts roots to a bank with over 120 retail branches, commercial and residential lending centers, and investment management offices.

Tengel most recently served as senior executive vice president, head of commercial specialty banking at M&T Bank. Prior to M&T’s recent acquisition of People’s United Financial, Tengel was president of People’s United where he was responsible for commercial banking, retail banking, and wealth management. He joined People’s United in 2010 from PNC Bank where he worked following PNC’s acquisition of National City Bank. At National City, Tengel served as executive vice president of corporate banking, managing the specialized industry, capital markets, commercial real estate, equipment finance, and private equity business lines

Union Savings Bank Names Chelen Reyes President

Union Savings Bank, a Danbury, Conn.based community bank, announced that Chelen Reyes is the bank’s next president.

“As we conducted our search for the next president of Union Savings Bank, Chelen rose to the top, embodying so many of the qualities we believe are necessary to lead this institution well into the future,” said Lucie Voves, USB’s board chair.

Reyes will be responsible for managing the day-to-day operations of the bank, which has 25 branches in Connecticut. He comes to Union Savings Bank from Hudson Valley Credit Union, where he served in a number of executive roles - most recently as HVCU’s senior vice presidenthaving responsibilities for retail delivery, marketing and lending.

In his two decades in banking, Reyes has held positions in retail banking, lending, wealth management, and marketing with institutions of varying sizes. He has led numerous initiatives focused on strategic growth, new product rollouts, customer relationships, compliance, and training for employees. Prior to beginning his banking career, Reyes worked in the technology sector.

Reyes succeeds Cynthia Merkle as president. Merkle will maintain her CEO role until her retirement later this year.

“I’m excited about the opportunity to join Union Savings Bank, and I’m incredibly thankful to the bank’s leadership for placing their faith in me as their next president,” Reyes said. “Cindy [Merkle] and those who held this position before her have brought incredible success to USB; I hope that I’m able to do the same.”

Reyes graduated with a degree in management from De La Salle University in Metro Manila, Philippines, and holds a Master’s in Business Management from the Asian Institute of Management in Makati, Philippines.

BANKING NORTHEAST MAGAZINE | 15

Jeffrey J. Tengel

Lisa Florian

Ronald Celaschi

16 | BANKING NORTHEAST MAGAZINE

DATABANK BANKING NORTHEAST MAGAZINE | 17

Recognizing The Best In Financial Marketing

Financial institutions responded to challenges in creative ways in 2022

Financial marketing. It sounds like something we all know what it is, but do we? It’s so much more than ads on social media and cable television stations.

For example, where financial marketing best serves credit unions and banks might be the campaigns that affect a consumer's image of, emotional connection to, and message perception of the financial institution.

One great emotional connection was made between Passumpsic Bank, a community focused bank in Vermont and northern New Hampshire, and its customers who love the great outdoors with Bank of the Wild.

PeoplesBank knew it had a leg up on larger competitors as a community bank that balanced local, easily accessible resources, and convenient technology. Its mission was to create frictionless banking.

Berkshire Bank is pursuing its vision of being the leading socially responsible omni-channel community bank in the markets it serves. It is creating economic inclusion by leveraging a suite of interconnected, innovative strategies, products, and services.

Financial marketing can also be used for an internal look at a bank’s or credit union’s most valuable assets: its employees. North Brookfield Savings Bank’s mission was to have a happy workforce. So, to that end, the bank created the Recognition Wednesday Campaign, where employees nominate each other for the weekly honor.

Look on the following pages to see what these financial institutions have creatively achieved to make the most of their financial marketing efforts. >>

18 | BANKING NORTHEAST MAGAZINE

MARKETING

BANKING NORTHEAST MAGAZINE | 19

THE BEST IN FINANCIAL MARKETING

North Brookfield Savings Bank

North Brookfield Savings Bank’s mission was to have a happy workforce. So, to that end the bank created the Recognition Wednesday Campaign, where employees nominate each other for the weekly honor.

It’s about happiness

“Employees are genuinely happy when they nominate others and when they themselves are nominated,” said Andrea Healy, FSVP, chief administrative and HR officer for the bank.

The North Brookfield, Mass., bank with over $350 million in assets promotes the recognition campaign internally and on LinkedIn and Facebook.

“We have had other banks and employers comment on how they appreciate how much we recognize our teams,” Healy said. “They often say how refreshing it is to see that we promote them for others to see. This type of kindness has no budget and no cost but the ROI is astounding.”

The bank often sends reminders to staff about nominating others, and the campaign has spilled over into the community. Community members/customers have been nominated for recognition for emulating the bank’s core values.

“We have effectively used a budget of zero to create the best ROI for the bank, a happy employee,” Healy said. “After all, if customers see and feel happy employees, they want to do business with us."

THE BEST IN FINANCIAL MARKETING 20 | BANKING NORTHEAST MAGAZINE

Cornerstone Bank

Cornerstone Bank feels it is its duty to give back to the community. A large part of that giving back is promoting financial literacy through partnerships that educate in easyto-understand ways and provide real-world skills that will last a lifetime.

Promoting financial literacy

The Southbridge, Mass., bank with assets over $1.4 billion, first reached out to community organizations to offer its financial literacy programs. As word spread about the availability of the programs, the bank began to get requests for them. The 2022 budget of $75,000 is to be significantly increased this year to deal with the growth.

The bank’s presentations are based on the needs of the audience. Employees with specialized expertise help conduct the presentations.

The literacy initiative comprises three ongoing projects within central Massachusetts.

• A partnership with Financial Literacy at Gateway Academy in Shrewsbury to offer students in grades 1-12 a weekly class for 10 years;

• A monthly class to children at In the Hour of Need Family Shelter in Worcester;

• A monthly class to all students in the afterschool program at Our Bright Future on Southbridge.

Cornerstone worked with more than 44 organizations in 2022, dedicating more than 360 hours to its financial literacy initiative.

In addition to the three primary ongoing initiatives, the bank conducted financial literacy presentations in 12 schools at the elementary, middle school, high school, and college levels, as well as community organizations, including senior centers, libraries, after-school programs, Girls Scouts, and YMCAs.

Most of these interactions led to repeat and increased instruction at the primary location as well as increased word-of-mouth requests from other similar organizations.

BANKING NORTHEAST MAGAZINE | 21

THE BEST IN FINANCIAL MARKETING

Passumpsic Bank

Passumpsic Bank, a community-focused bank in Vermont and northern New Hampshire, wanted to increase its brand awareness in the region. So it enlisted Saltwater to produce a campaign designed to reach audiences ages 18 to 65.

‘Start Your Adventure’

Saltwater set out to build a creative campaign that would stand out in the market. The team knew it had a great tagline in “Start Your Adventure.” The team also knew that New Englanders love the outdoors, so it asked itself some questions. What if New Englanders didn't have to interrupt their outdoor adventures to do their banking? What if it could combine customers' love for the outdoors with Passumpsic Bank’s great services?

And with that, The Bank of the WIld was born. With a budget of $190,000, a multifaceted campaign was built. It would be a campaign that proved to be incredibly successful. Passumpsic Bank, with assets over $880 million, was thrilled with the results.

Saltwater introduced The Bank of the Wild to the public through two unique teaser videos, designed to build anticipation prior to the primary spot launch. Both teasers ran for two weeks and included a vanity URL that would lead viewers to the bank’s landing page. This was followed by the primary campaign launch on television, as well as placements on Instagram, Facebook, Twitter, LinkedIn, and YouTube.

To support the campaign after The Bank of the Wild aired, the bank boosted content showing

the perspective of its A-Tree-M machine and what it sees during a typical day in the forest, as well as two longform Mockumentary interviews with Bank of the Wild employees. Pieces of the set were shipped to Passumpsic branch locations, and Sasquatch footprints were added to outside locations to highlight the bank's working relationship with that famous creature of the forest.

With more than 1.5 million television impressions via WCAX and more than 5.3 million digital impressions, the Bank of the Wild was widely seen by the 18-65 target group. Plus, more than 25% of impressions came from viewers younger than 45, positive momentum toward the goal of expanding Passumpsic Bank's awareness with younger audiences.

A great deal of activity was seen on Facebook and Instagram, with considerable growth of 154% on Instagram Reels in particular. The creative saw 150 seconds of time earned, which is on average an additional two and a half minutes with engaged users as compared with standard video assets. The partnership with Hulu allowed the campaign to make use of its Interactive Living Room tool.

Smart television/OTT viewers saw the 30-second spot coupled with a prompt to "Learn More." Viewers were brought to a branded page with the option to screen other videos from the campaign. This branded page included a customized Bank of the Wild theme, simple messaging, and a QR code directing viewers to the landing page, bankofthewild. com. This creative had an engagement rate of .58%, exceeding Hulu's internal benchmark standard of .46%.

THE BEST IN FINANCIAL MARKETING 22 | BANKING NORTHEAST MAGAZINE

PeoplesBank

PeoplesBank embarked on a journey in 2019 to redefine itself in an effort to uncover a unique brand position that mirrored its mission and connected the dots between its products and services.

PeoplesBank knew it had a leg up on larger competitors as a community bank that balanced local, easily accessible resources, and convenient technology. Its mission was to create frictionless banking. From there, the idea of Simple was bornnot basic or generic - but fewer hassles and better options that fit the needs of customers within its footprint.

PeoplesBank, with assets of $3.56 billion, evaluated all of its products through a “simple” lens so it could deliver on this message. The campaign is still running strong as the idea of Simple continues to resonate with consumers.

The success of Simple is measured by lift in brand awareness and a year-over-year increase in account openings and balances.

Simple but effective

During the campaign’s first year, brand awareness was a key factor in influencing the most effective channel allocation for a $1 million media spend. PeoplesBank delivered more than 80 million impressions to consumers within its footprint through a mix of high-level brand awareness tactics and targeted programmatic digital tactics.

PeoplesBank continues to see the importance of brand advertising used as a “halo” over its product messaging for retail, business banking and consumer lending. The bank saw increased mortgage and personal loan applications during the sustained brand spend.

While top-funnel brand tactics were crucial in building equity in the Simple brand, it also focused funds on digital, as online banking boomed in a post-pandemic landscape. By dialing up digital, PeoplesBank saw a 10% increase in web traffic during the first year of the campaign. Growth continues in site visits and session duration.

PeoplesBank associates are committed to carrying out the Simple brand message in everything they do, from their interactions with customers to introducing new technology, such as VideoBankerITMs, which give customers access to a drive-up teller seven days a week.

As the bank increased its emphasis on messaging in the more expensive Connecticut market, spending was increased and allocated to deliver effective and efficient communications.

The numbers support the effectiveness of this campaign. A few more examples:

• Broadcast outperformed Northeast regional advertisers, as well as financial industry averages, by driving a 78% higher website visitation lift following the airing of the spot.

• When people were asked “how familiar are you with PeoplesBank,” the bank saw a brand lift of 10% (two times higher than the benchmark lift of 5%) after the launch of the 2020 campaign.

• In 2022, this momentum continued as video partner ViralGains, reported an 11.12% total brand lift when more audience members ranked their familiarity with PeoplesBank at 4 or 5 out of 5.

• Paid search performance in the Connecticut demographic remains strong and is up 120% compared to 2021 with a 13% click-through rate and 6.6% click to app start rate.

THE BEST IN FINANCIAL MARKETING BANKING NORTHEAST MAGAZINE | 23

Berkshire Bank

Berkshire Bank is pursuing its vision of being the leading socially responsible omni-channel community bank in the markets it serves.

Headquartered in Boston, Berkshire, which operates 100 offices primarily in New England and New York, is creating economic inclusion by leveraging a suite of interconnected, innovative strategies, products, and services. Collectively, this effort comprises the Be FIRST Commitment, which has helped impact more than 86,000 individuals and ensured the economic resiliency of people, small businesses, and nonprofits.

MyCheck is a socially responsible, low-cost alternative to traditional check cashing. MyFreedom is a nationally acclaimed and Bank On certified checking account recognized for its affordability, transparency, and accessibility.

Commitment to inclusion

Nearly 30% of the bank’s mortgages in 2020 went to first-time homebuyers. For those already in their homes and in lowmoderate income communities, the bank offers MyCommunity, a home equity product specifically designed to revitalize LMI neighborhoods.

To power the underrepresented business ecosystem, Berkshire Bank’s Reevx Labs provides opportunities for nonprofits, small businesses, and entrepreneurs to access technical assistance, professional development, financial education,, and pop-up retail space to test their concepts. Matched with the bank’s innovative Friends & Family Loan, a CD-backed community-underwritten loan, entrepreneurs can access financing.

Berkshire, which has assets of $12.1 billion, witnessed the outsized impact it was having on underrepresented groups who were having

difficulty accessing government programs. It deployed its capital through an innovative loan program called The Futures Fund in collaboration with the Black Economic Council and MA LGBTQ Chamber to provide more than $1 million in funding to businesses impacted by the COVID-19 pandemic.

A number of human and financial resources have gone into the development, implementation, and success of the bank’s economic inclusion programs. It includes nearly $1 million in direct philanthropic support to programs with nonprofit organizations that help power financial wellness along with nearly 2,000 hours of volunteer service in which employees provided financial coaching to individuals and businesses. The bank allocated more than $3 million to support loan programs aimed at helping underrepresented small businesses through The Futures Fund and raised $3 million in CDbacked investments to power the Friends & Family Fund loan program, which provides seed capital to small businesses run by marginalized and underrepresented populations.

The two Reevx Labs spaces have full-time community coordinators who manage programming in the spaces as well as two “Relationship Managers'' who help consumers with financial planning and access to a suite of socially responsible products and services. A fulltime community programs officer helps manage consumer programs. These full-time resources complement front-line bankers who all play a part in delivering programming, products, and services. Partners across business lines were involved in the development of the products and services offered through the economic inclusion program.

If businesses run into challenges as a result of uncertainties in the environment, the bank offers The Futures Fund, a very low-interest line of credit, accessible to people with lower credit scores and even prior criminal histories, to help get them through and build back stronger.

BEST IN FINANCIAL MARKETING 24 | BANKING NORTHEAST MAGAZINE

THE

Veterans, when you’re struggling, soon becomes later becomes someday becomes ...when?

Don’t wait. Reach out .

Whatever you’re going through, you don’t have to do it alone.

Find resources at VA.GOV / REACH

BANKING NORTHEAST MAGAZINE | 25

advantagediscover the NES Find your design partner to achieve your long-term goals. advantage discover the NES bank design project management branding equipment new england new york 508.339.6600 nes-group.com What makes us different? In-house capabilities to imagine, design, and deliver your project. Let us build off your goals and help you realize your environments' creative potential.