EXPERT ARTICLE

75

MEASURABLE AND DEVASTATING IMPACT ON INDIA’S TEXTILE AND APPAREL INDUSTRY

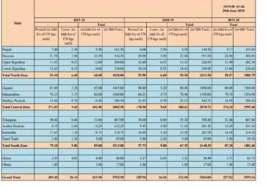

OVERVIEW The manufacturing and market conditions in India s Textile and apparel industry sectors continues to be at the bottom of `U `curve with no significant pick up in domestic demand or international export orders, with exports down by almost 60% in April 2020. Despite the much hyped economic Relief package of the govt. for the MSME industry; nearly 30-35% of smaller and medium size units are expected to go under despite only 3 months away from the traditionally high demand and market turnover period of Festivals season from mid October. The key downturn factors continue to be the drastically reduced retail and export demand, and big cut down in the `disposable/surplus` incomes due to millions of job losses amidst Covid crisis.In terms of numbers, the market size of India s overall T & C sector is approx. $110 to 120 Billion,and of which only $ 35 billion accrues from exports,which owing to Covid 19 impact took a hit of $10.36 billion for financial year ending April 2020 alone.In contrast, both Bangladesh and Vietnam too took a 30% down hit on their T&C exports which averaged to approx. $35 billion each .Even the market access they got due to GSP+ access to Europe and, incase of preferential access of Vietnam into the USA markets has not helped much to pep up their exports considering that the retail store and high street retail selling itself is down 30-35% in both Europe and the USA.While Vietnam is yet benefitting immensely with the preferential FTA pacts, India has lagged behind to the serious handicap to its textile and clothing industry exports. There is now urgent and dire need for India s FTA pacts esp. with EC, Japan, ASEAN and also with the

new large market blocks of Euroasia and Africa under the 49 country AcFTA common market. Sectorwise woes,and Issues GARMENT INDUSTRY As per trade body,CMAI, only 25% garment units have resume working despite easing of lockdown by end of June. However,the resumed factories are operating at an average 25% of their capacity. Considering that the ongoing Summer period is typically a low season for both domestic retail and exports, No substantial demand enhancement can be expected for atleast next 1 to 2 quarters by when the `traditional` Festival period from mid Oct.to mid November will be over without any significant Domestic market revival.Owing to the slow and limited domestic demand ,the Indian fabric and garment making sector is witnessing a drastic shift from traditional products to new ones, such as PPEs, N-95 masks and technical textiles incl. production of Meltblown fabrics. Incase of exports and, in the short-term, Indian apparel exporters are fearing missed deadlines – with key inputs like apparel trims etc from China either stuck at Indian customs or not shipped at all following military tensions between the two neighbours. Indian garment industry is presently also suffering due to import ban on Chinese goods,as per the case in point: 1) The garment industry could suffer severe repercussions if India’s unofficial slowdown on customs clearance and ban on Chinese imports continues. Items such as garment fabrics and trims,machines | J U LY 2 0 2 0